Bankruptcy has assisted millions of Americans in reducing their debt burden and obtaining a fresh start. There are various types of bankruptcies, so it is critical to understand the distinctions and similarities. We have the 3 types of bankruptcy for businesses and two types of bankruptcy for individuals. First, let’s understand the concept of bankruptcy.

What Is the Definition of Bankruptcy?

More than just a way to lose a game of Monopoly, bankruptcy in real life is a lot more serious: it’s when you go before a judge and tell them you can’t pay your debts. Then, depending on the circumstances, they either erase your debts or devise a repayment plan for you. Different individuals file for a type of bankruptcy for a variety of reasons, including job loss, divorce, a medical emergency, or family death. In fact, over 730,000 types of non-business bankruptcies were filed in 2018.1 That’s insane!

It’s also important to understand that bankruptcy does not discharge student loans, government debts (taxes, fines, or penalties), reaffirmed debt (where you recommit to the terms of an existing loan), child support, or alimony. So, if those are your only debts, bankruptcy is not the way to go.

What are the Different types of Bankruptcies?

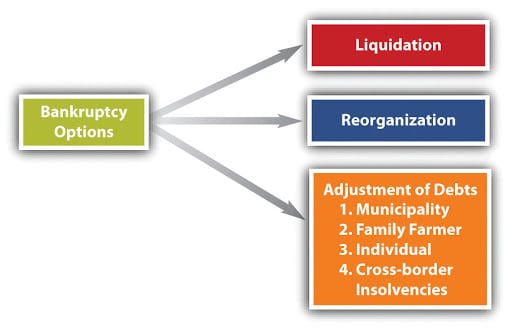

Even though the general goal of bankruptcy is to discharge debt, all bankruptcies are not equal. In reality, there are six different types of bankruptcies:

- Chapter 7: Liquidation

- Chapter 13: Repayment Plan

- Chapter 11: Major Reorganization

- Chapter 12: Family Farmers

- Chapter 15: Applied in Foreign Cases

- Chapter 9: Municipalities

You might have taken one look at this list and then zoned out for the rest of the time. That’s all right. A chapter simply refers to the specific section of the United States Bankruptcy Code where the law is found. But we’ll go over each type so you’re familiar with your options.

Two Types of Individual Bankruptcy

There are two most common types of bankruptcies for individuals: Chapter 7 and Chapter 13.

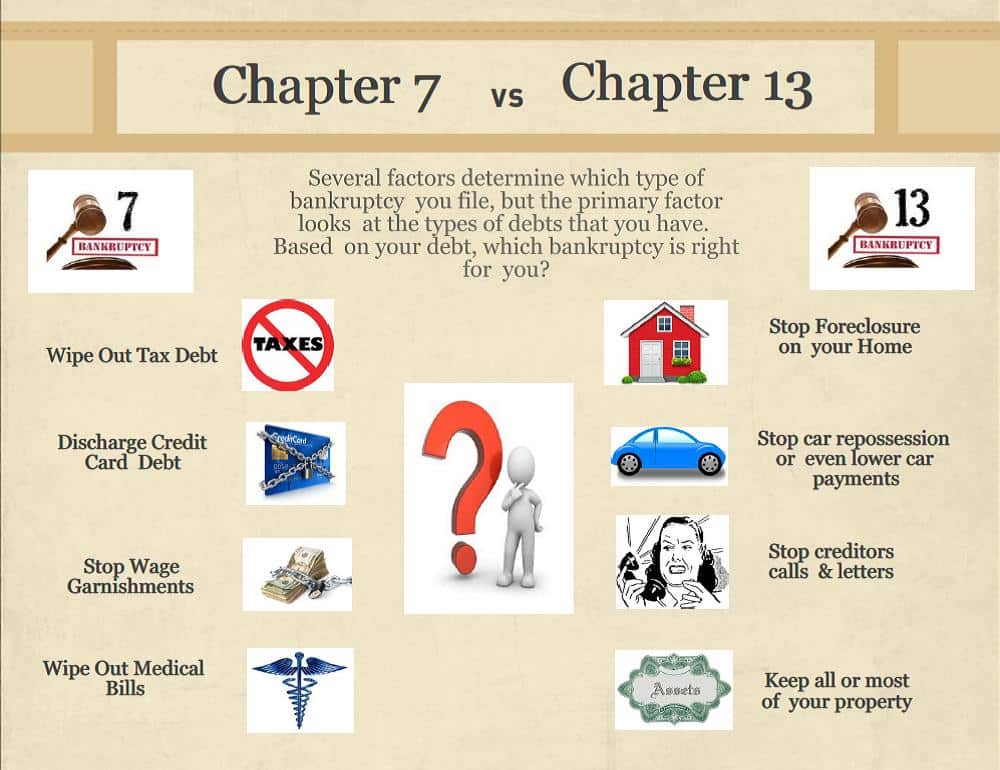

#1. Chapter 7 Bankruptcy

Chapter 7 bankruptcy, also known as the liquidation or straight bankruptcy, is the most common type of individual bankruptcy. A court-appointed trustee supervises the liquidation (sale) of your assets (anything of value you own) to pay off your creditors (the people you owe money to). Any remaining unsecured debt (such as credit cards or medical bills) is typically discharged. However, as previously stated, this does not include debts that are not dischargeable through bankruptcy, such as student loans and taxes.

Depending on which state you live in, the court may not order you to sell certain items. During Chapter 7 bankruptcy, for example, most people are able to keep basic necessities such as their home, car, and retirement accounts, but there is no guarantee. Chapter 7 cannot stop a foreclosure; it can only postpone it. The only way to keep the items you still owe money on is to reaffirm the debt, which means recommitting to the loan agreement and continuing to make payments. However, the vast majority of Chapter 7 bankruptcies are no-asset cases, which means there is no property of sufficient value to sell.

You can only file for Chapter 7 bankruptcy if the court determines that you do not earn enough money to pay off your debts. This decision is based on the means test, which compares your income to the state average and examines your finances to determine whether you have enough disposable income. If your income is insufficient, you may be eligible for Chapter 7.

A Chapter 7 bankruptcy also stays on your credit report for ten years, and you won’t be able to file again for eight years.

#2. Chapter 13 Bankruptcy

While Chapter 7 bankruptcy often results in debt forgiveness, Chapter 13 type of individual bankruptcy essentially reorganizes it. The court approves a monthly payment plan that allows you to repay a portion of your unsecured debt and all of your secured debt over three to five years. The monthly payment amounts are determined by your income and the amount of debt you have. However, the court has the authority to place you on a strict budget and monitor all of your spending (ouch!).

Unlike Chapter 7, this type of individual bankruptcy allows you to keep your assets while catching up on any non-bankruptcy debt. Chapter 13 individual types of bankruptcy can also help you avoid foreclosure by giving you more time to pay off your mortgage.

Anyone can file for Chapter 13 bankruptcy if their unsecured debt is less than $419,275 and their secured debt is less than $1,257,850. You must also keep up with any tax filings. You should also be aware that a Chapter 13 bankruptcy remains on your credit report for seven years and that you cannot file for it again for two years.

Three Types of Business Bankruptcy

Depending on its structure, a business can file for one of three types of bankruptcy. Sole proprietorships are legal extensions of the owner. The owner is personally liable for the company’s assets and liabilities. A sole proprietorship is most likely to declare bankruptcy by filing for Chapter 13, which is a reorganization bankruptcy.

Corporations and partnerships are legal business entities distinct from their owners. They can file for Chapter 7 or Chapter 11, which are types of reorganization bankruptcy for businesses.

#1. Chapter 13: Debt Adjustment for Individuals with Regular Income

Chapter 13 bankruptcy is a type of reorganization bankruptcy that is usually for businesses. It can be used for sole proprietorships because sole proprietorships are indistinguishable from their owners. When reorganization, rather than liquidation, is the goal of a small business, they use Chapter 13. You file a repayment plan with the bankruptcy court outlining how you intend to repay your debts. For businesses, Chapter 13 and Chapter 7 bankruptcies are vastly different.

Chapter 13 permits the proprietorship to continue operating and repaying its debts, whereas Chapter 7 does not.

The amount you must repay is determined by how much you earn, how much you owe, and how much property you own. If your personal assets are part of your business assets, as they are if you own a sole proprietorship, filing Chapter 13 instead of Chapter 7 can help you avoid problems like losing your home.

#2. Chapter 7: Liquidation

When a business has no viable future, Chapter 7 business type of bankruptcy may be the best option. They commonly refer to it as a liquidation. Chapter 7 is typically used when a company’s debts have become so overwhelming that restructuring them is not an option. Sole proprietorships, partnerships, or corporations can use Chapter 7 bankruptcy.

When the company does not have any significant assets, Chapter 7 is also an option. If a business is a sole proprietorship and an extension of the owner’s skills, it usually does not make sense to reorganize it. and Chapter 7 becomes appropriate. Before a Chapter 7 bankruptcy is granted, the applicant must pass a “means” test. If their income exceeds a certain threshold, their application will be denied. If a Chapter 7 bankruptcy is granted, the business is dissolved.

The bankruptcy court appoints a trustee to take possession of the business’s assets and distribute them among the creditors in Chapter 7 bankruptcy. At the end of the case, a sole proprietor receives a “discharge” after the assets are distributed and the trustee is paid. A discharge means that the owner of the business is no longer obligated to pay the debts. Partnerships and corporations do not receive a discharge.

#3. Chapter 11: Business Reorganization

Chapter 11 bankruptcy may be a better type for businesses that have a realistic chance of turning things around. Sole proprietorships whose income levels are too high to qualify for Chapter 13 bankruptcy also use it.

A Chapter 11 plan is one in which a company reorganizes and continues operations under the supervision of a court-appointed trustee. The company files a detailed plan of reorganization outlining how it will deal with its creditors. To return to profitability, the company can terminate contracts and leases, recover assets, and repay a portion of its debts while discharging others.4 It will present the plan to its creditors, who will vote on it. If the court finds the plan to be fair and equitable, it will approve it.

Reorganization plans call for creditors to be paid overtime. Bankruptcies under Chapter 11 are extremely complex, and not all of them are successful. It usually takes more than a year to finalize a plan.

Other Types of Bankruptcy

Chapter 12 Bankruptcy

This is a repayment plan that allows family farmers and fishermen to avoid having to sell all of their belongings or foreclose on their property. While Chapter 12 bankruptcy is similar to Chapter 13, it is a little more flexible and has higher debt limits.

Chapter 15 Bankruptcy

This Chapter international bankruptcy issues and grants foreign debtors access to U.S. bankruptcy courts.

Chapter 9 Bankruptcy

Chapter 9 bankruptcy is yet another repayment plan that allows towns, cities, school districts, and other entities to reorganize and repay their debts.

Visit the United States Courts website for more specific information about bankruptcy laws in your area.

Which Type of Bankruptcy Is Best for My Case?

Since the other forms of bankruptcies are tailored to particular individuals or companies, most people are only eligible for Chapter 7 or Chapter 13.

Differences between Chapter 7 Bankruptcy and Chapter 13 Bankruptcy

The main distinction between Chapter 7 and Chapter 13 bankruptcy is based on the individual’s assets and income level. For example, if a person has recently lost a job or has an inconsistent income, they can be forced to file for Chapter 7 bankruptcy. However, if the means test shows that they make enough money to pay off their loans, they will be placed in a Chapter 13 bankruptcy instead. If preventing home foreclosure is a top priority, someone may file for Chapter 13. They may also file for Chapter 7 if time is of the essence, as it is quicker than Chapter 13.

However, bankruptcy is a frightening experience. Deciding between Chapter 7 and Chapter 13 is like attempting to choose the lesser of two evils. In both cases, anonymity is sacrificed. All of the evidence is basically set out on a table for the court to review. Then there’s the fact that they get to dismiss about half of all Chapter 13 bankruptcy proceedings in the United States. This is because the debtor is unable to make the monthly payments.

Bankruptcy may appear to be a magic wand that can solve all of your problems. However, it is far from a magical experience, and it has a significant emotional cost. Dave Ramsey declared bankruptcy before completely changing his financial habits, and he never encourages anyone to do the same. In reality, he considers bankruptcy to be on par with divorce in that it should be used only as a last resort after exhausting all other options.

So, let’s take a look at some alternatives to declaring bankruptcy.

What are some alternatives to Bankruptcy Filing?

It is possible to escape any type of bankruptcy, no matter how deeply in debt you are. You just need to be aware of your choices. Here are a few steps you can take to get out of debt without declaring bankruptcy:

#1. Take care of the basics.

Before you do something, ensure that the Four Walls are covered: food, utilities, shelter, and transportation. If you don’t have a place to sleep or food to eat, you won’t have the stamina to battle your way out of debt. So prioritize taking care of yourself and your family. The collectors would have to wait.

#2. Make a budget.

We previously explained that in Chapter 13 bankruptcy, the court places you on a budget and keeps track of your expenses. But the fact is that you can do all of those things without declaring bankruptcy. Having a budget can be a game-changer if you’re nearing the end of your rope. Instead of worrying about where your money went, track it. You’ll find the money you didn’t even know you had. And, indeed, budgeting entails eliminating all unnecessary costs in order to pay off debt. You should cancel cable and subscriptions. There will be no more eating out. There will be no more holidays. You’re in a state of survival. Instead of the government telling you how to manage your money for five years in a bankruptcy case, you get to make the decisions.

#3. Increase your earnings.

Your income is your most potent wealth-creation (and debt-reduction) tool. The more money you earn, the more money you have to throw at your debt. As a result, you might need to take on a second job or work extra hours at your current job to help you get by while you catch up on your monthly payments. Yes, it can be frustrating, but the short-term sacrifice will be well worth it in the end.

#4. Sell your belongings.

Remember how we said that in Chapter 7 bankruptcy, the court liquidates your assets? What if you sold your possessions instead? If you have something valuable, such as a yacht, a fancy lawnmower, or anything with a motor that you don’t use to get to work, sell it! Furniture, collectibles, jewelry, the guitar you told yourself you’d learn to play someday—everything you don’t need has to go. Doesn’t that sound outlandish? This is essentially what would happen if you declared bankruptcy, except you would have no say over how your belongings were sold. So go to Craigslist, eBay, and Facebook Marketplace and sell your items for fast cash.

Advantages And Disadvantages Of Bankruptcy

One of the major advantages of bankruptcy is its ability to lift the burden of debt. Furthermore, it prevents the possible lost of ones house or business

However, this is at a disadvantage. It may cancel your debt but, it damages your credit score. Some bankruptcy stays on your credit rating for a number of years. Some for 10 years, more or less depending on the types of bankruptcy.

What are the eligibility requirements for Chapter 13 bankruptcy?

To be eligible for Chapter 13 bankruptcy, an individual must have a regular source of income and unsecured debts of less than $394,725 and secured debts of less than $1,184,200.

What happens to debts in Chapter 12 bankruptcy?

In Chapter 12 bankruptcy, the debtor proposes a repayment plan to repay all or a portion of their debts over a 3-5 year period. After the repayment plan is confirmed by the court, the debtor makes payments to the Chapter 12 trustee, who then pays the creditors. Any remaining eligible debt is discharged at the end of the repayment period.

What is Chapter 13 bankruptcy for individuals with regular income?

Chapter 13 bankruptcy is a type of bankruptcy available to individuals with a regular source of income. It allows individuals to repay some or all of their debts over a 3-5 year period under the supervision of a bankruptcy court.

What is the process of filing for Chapter 12 bankruptcy?

To file for Chapter 12 bankruptcy, an individual must:

- Complete and file a petition with the bankruptcy court

- Provide a list of creditors, assets, and liabilities

- Provide proof of income and expenses

- File a proposed repayment plan with the court

- Attend a meeting of creditors

- Obtain court approval of the repayment plan.

What are the eligibility requirements for Chapter 12 bankruptcy?

To be eligible for Chapter 12 bankruptcy, an individual must be a family farmer or fisherman with regular income from farming or fishing operations. The individual’s debts must also meet certain limits.

What is the role of a plan of reorganization in Chapter 11 bankruptcy?

In Chapter 11 bankruptcy, a plan of reorganization is a proposal made by the debtor to repay creditors over a specified period of time. The plan must be approved by the bankruptcy court and the creditors. The plan outlines the terms of the reorganization, including the treatment of creditors, the payment of debts, and the restructuring of the debtor’s business operations.

Make a plan!

Did you know that before your debt can be forgiven, most bankruptcy courts require you to complete a financial literacy course? This is because debt has become a way of life for so many people. But this does not have to be the case! Financial Peace University (FPU) will show you how to break bad money habits, invest and pay off debt like a boss, and create a bright future for yourself and your family. Furthermore, it is less expensive than the bankruptcy court bill. This tried-and-true strategy has assisted nearly 6 million people in making positive changes in their lives.

Types Of Bankruptcy FAQs

What are the four types of bankruptcies?

There are six chapters of bankruptcy in the United States, Chapter 7, Chapter 9, Chapter 11, Chapter 12, Chapter 13, and Chapter 15, with Chapter 7 and Chapter 13 bankruptcy being the most common forms filed.

What is the difference between Chapter 7 and 13 bankruptcy

With Chapter 7, those types of debts are wiped out with your filing’s court approval, which can take a few months. Under Chapter 13, you need to continue making payments on those balances throughout your court-instructed repayment plan; afterward, the unsecured debts may be discharged

Does Chapter 11 wipe out debt?

An individual filing for Chapter 11 won’t get the discharge until you have made all payments under the plan. Also, an individual cannot wipe out some types of debt, such as domestic support obligations, some taxes, and liabilities incurred through fraud. Learn more about how Chapter 11 bankruptcy works.