What is CCC?

The cash conversion cycle (CCC) – often known as the cash cycle – is a working capital indicator that measures how long it takes for a company to convert cash into inventory and then back into cash through the sales process. The lower the CCC, the less time a company’s cash is locked up in accounts receivable and inventories.

Basically, the CCC is a crucial indicator for companies that buy and manage inventory. This is because it indicates both operational and financial efficiency. It should, however, not be seen in isolation, but rather in conjunction with other financial indicators such as return on equity. It’s also worth noting that CCC isn’t a major consideration for all businesses, as not every company will have physical inventory.

Understanding the Cash Conversion Cycle (CCC)

The CCC is made up of multiple activity ratios that include accounts receivable, payable, and inventory turnover. AP is a liability, while AR and inventory are short-term assets. The balance sheet contains all of these ratios. In reality, the ratios show how well management is generating cash from short-term assets and liabilities. An investor can use this information to assess the company’s overall health.

But then, you may ask, “What are the business implications of these ratios?”

Cash flows fast through a firm if it sells what customers desire to buy. The CCC slows down if management fails to realize potential sales. For example, if too much inventory accumulates, cash is locked up in things that cannot be sold, which is bad for business. To move inventory rapidly, management must lower prices, perhaps losing money on the sale of its items.

If AR isn’t well-managed, the organization may have trouble collecting payments from customers. And because AR is essentially a loan to the consumer, the company loses money when they don’t pay on time. The longer a corporation has to wait for payment, the less money is available for further investments. Slowing down AP payment to suppliers, on the other hand, benefits the company because of the extra time it allows to put the money to better use.

The Cash Conversion Cycle’s Elements

Calculating the CCC may be daunting at first, but once you grasp the elements involved, it becomes much easier.

To make the calculations, you’ll need to consult your financial statements, such as the balance sheet and income statement. Meanwhile, the three major elements of the cash conversion cycle include, Days Inventory Outstanding, Days Sales Outstanding, and Days Payable Outstanding.

Days Inventory Outstanding

Days Inventory Outstanding is the first part of the equation (DIO). This is the average time for inventory to be converted into final products and sold.

DIO = (Average Inventory ÷ Cost of Goods Sold) x 365

But then the average inventory (in value) for the period will be an addition of the beginning inventory value and ending inventory value; then dividing the sum by 2

Mathematically;

(Beginning Inventory + Ending Inventory) ÷ 2

The cost of products sold is calculated as follows:

Ending Inventory = Beginning Inventory + Purchases.

Days Sales Outstanding

Days Sales Outstanding (DSO) is the average number of days it takes for you to retrieve your accounts receivable (money owing to you).

DSO = (Net Credit Sales + Accounts Receivable) x 365

The average of your beginning and ending receivables is your accounts receivable for this section.

(Beginning Receivables + Ending Receivables) ÷ 2

Days Payable Outstanding

Days Payable Outstanding (DPO) is the average time it takes a firm to purchase goods and services from its suppliers on accounts payable (your company owes money) and pay for them.

DPO = Ending Accounts Payable ÷ (Cost of Goods Sold ÷ 365)

In this section, the accounts payable are:

(Beginning Payable + Ending Payable) ÷ 2.

What Constitutes a Satisfactory Cash Conversion Cycle?

A short cash conversion period is ideal.

If your CCC is low or (better still) negative, your working capital is not locked up for long periods of time, and your company has more liquidity. Many online businesses have low or negative CCCs because they drop-ship instead of retaining inventory. They receive immediate payment when customers buy things, and do not have to pay for inventory until customers have already paid them.

On the other hand, you don’t want your CCC to be too high if it’s a positive number. A positive CCC indicates how many days your company’s working capital is stranded as it waits for accounts receivable to be paid. If you sell things on credit and your customers need 30, 60, or even 90 days to pay you, you may have a high CCC.

Read Also: SHORT TERM DEBT: Definition, Examples, and Debt financing

However, you can shorten your company’s cash conversion cycle in a number of ways.

This is by making your accounts receivable procedure as efficient as possible, for starters. Remove any needless jargon from your bills and be explicit about what you’re billing for and the terms you’re requesting.

For the most part, you’ll receive payments faster if the buyer understands the invoice quickly. You can also reduce the CCC by requesting advance payments or offering a discount for paying early. Finally, staying on top of late payments by following up as soon as a payment is due is a good idea.

What Role Does Cash Flow Play?

The cash conversion cycle is a cash flow formula that determines how long it takes for your company to convert inventories and other assets into cash. To put it another way, the cash-to-cash cycle time is the interval between when you pay for inventory and when customers pay to replenish your company’s cash flow. Keeping cash flow positive in industries with high inventory and material demands, such as construction, can be the difference between taking on new clients and turning them away.

The conversion cycle calculation determines how long a company’s cash is held until it is recovered from clients and customers. Keeping a careful eye on the company’s CCC might help you keep track of its total finances as money comes in and goes out. If you’re confused about the differences between cash flow and profit, keep in mind that they’re not the same thing. While profit is the amount of money left over after a company’s expenses are paid at a fixed point in time, cash flow is flexible. It shows how much money is coming in and going out of a company.

What’s the Difference Between a Cash Conversion Cycle and an Operating Cycle?

Obviously, there’s a big difference between a cash conversion cycle and an operating cycle.

Simply put, an operating cycle is the number of days between when you buy goods and when clients pay for them. The cash conversion cycle is the number of days it takes for you to pay for inventory and receive payment from your clients.

Why is the Cash Conversion Cycle so important?

There are various reasons why keeping track of your cash conversion cycle is critical.

For starters, investors, lenders, and other sources of capital frequently examine a company’s cash conversion cycle to gauge its financial health and, in particular, its liquidity. A company’s liquidity determines how readily it can repay a corporate loan, satisfy other financial obligations, and invest in growth. Furthermore, the cash conversion cycle is particularly useful for evaluating inventory-based enterprises like shops. However, it is not the only financial criterion used by lenders; they often mix it with other factors before determining whether or not to give out the loan.

Suppliers may consider your CCC while considering whether or not to grant credit to your business. They are often concerned that you may not be able to pay them on time if your company lacks appropriate liquidity.

Read Also: Debt To Equity Ratio: Explained!!!, Formula, Calculations, Examples

On the other hand, you should be concerned about the cash conversion cycle as well.

Like we earlier mentioned; a low CCC suggests that you’re doing a good job of converting inventory to cash and that your firm is running well. If your CCC is too high, however, it could indicate operational concerns, a lack of demand for your goods, or a shrinking market niche. So if your CCC isn’t to your liking, determine what’s wrong and take steps to fix it, such as increasing your invoice collection efforts.

Finally, when determining how much money you need to borrow, your cash conversion cycle is a crucial factor to consider. Understanding your CCC and, as a result, your company’s liquidity, can assist you in determining how much cash you can request from a lender.

The Formula for CCC

Since CCC includes calculating the net aggregate time involved over the three stages of the cash conversion lifecycle mentioned above, the mathematical formula for CCC is:

CCC=DIO+DSO−DPO

where: DIO=Days of inventory outstanding(also known as days sales of inventory)

DSO=Days sales outstanding

DPO=Days payables outstanding

DIO and DSO represent cash inflows, whereas DPO represents cash outflows.

As a result, DPO is the sole negative number in the equation. Another way to look at the formula is that DIO and DSO are tied to inventory and accounts receivable, which are both considered short-term assets and are assumed to be positive. DPO is associated with accounts payable, which is a liability and consequently a negative number.

CCC Calculation

The cash conversion cycle of a business is divided into three parts. Several items from the financial accounts are required to compute CCC:

- The income statement showing revenue and cost of goods sold (COGS).

- The record of inventory at the start and end of the time period.

- Accounts receivable (AR) at the start and end of the time period

- Accounts payable at the start and end of the time period

- The number of days in the period (for example, a year is 365 days and a quarter is 90 days).

First Stage

The first stage is deals with the current inventory level and shows the time it will take for the company to sell its stock.

This value is comes from the Days Inventory Outstanding figure (DIO). Meanwhile, a lower DIO number is desirable because it implies that the company is making sales quickly, signifying a higher business turnover.

The cost of goods sold (COGS), which indicates the cost of obtaining or manufacturing the products that a company sells during a period, is is vital to calculating the DIO or DSI.

DSI= Avg. Inventory/ COGS ×365 Days

where: Avg. Inventory=21×(BI+EI)

BI=Beginning inventory

EI=Ending inventory

Second Stage

The second stage focuses on current sales and shows how long it takes to collect the sales proceeds.

Days Sales Outstanding (DSO) is a metric that divides average accounts receivable by revenue each day to arrive at this value. DSO with a lower value shows that the company is able to collect funds in a timely manner, so improving its cash position.

DSO= Revenue Per Day / Avg. Accounts Receivable

where: Avg. Accounts Receivable=21×(BAR+EAR)

BAR=Beginning AR

EAR=Ending AR

Third Stage

The third step focuses on the company’s current overdue payables. It indicates the amount of money a company owes its current suppliers for inventory and items purchased, as well as the time frame in which those commitments must be met.

Days Payables Outstanding (DPO), which considers accounts payable, is helps to determine this number. It is preferable to have a greater DPO value. By increasing this amount, the corporation may keep its capital for longer, allowing it to invest more.

DPO= COGS Per Day / Avg. Accounts Payable

where: Avg. Accounts Payable=21×(BAP+EAP)

BAP=Beginning AP

EAP=Ending AP

COGS=Cost of Goods Sold

All of the data above are accessible in a publicly-traded company’s financial statements. They are filed as part of its annual and quarterly reporting. For a year, the number of days in the corresponding period is 365, and for a quarter, it is 90.

What You Can Learn From the Cash Conversion Cycle?

The primary strategy for a company to increase profits is to increase inventory sales. But how can one increase sales? If cash is readily available at regular intervals, one can churn out more sales for profit, as more products to create and sell result from the frequent availability of money. Inventory can be purchased on credit, resulting in accounts payable (AP).

A business can also sell things on credit, resulting in receivables (AR). As a result, cash isn’t a consideration until the company pays its bills and collects its receivables. This means that cash management relies heavily on timing.

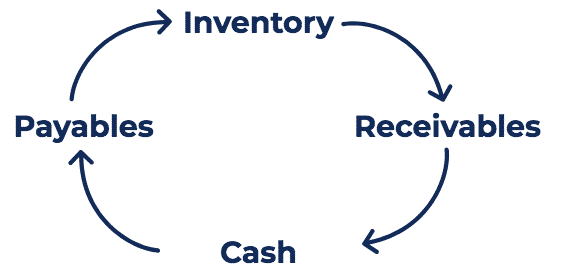

In other words, the lifespan of cash utilized for corporate activities is tracked by CCC. It tracks cash as it moves from cash in hand to inventory and accounts payable, then to product or service development expenses, sales and accounts receivable, and finally back to cash in hand.

Read Also: CHECK FORMAT: EXAMPLES, PROPER FORMAT, ROUTING NUMBERS & ALL YOU NEED

CCC is a measure of how quickly a corporation can convert invested cash from start (investment) to finish (exit) (returns). Again, the CCC should be as low as possible.

The three key ingredients of business are inventory management, sales realization, and payables. The business will suffer if any of these go out the window—for example, inventory mismanagement, sales restrictions, or payables increasing in number, value, or frequency. CCC accounts for the time spent in various procedures in addition to the monetary value, providing a different perspective on the company’s operational efficiency.

In general, the CCC value, in addition to other financial measurements, reveals how well a company’s management is using short-term assets and liabilities to generate and redeploy cash. It provides insight into the company’s financial health in terms of cash management. The graph also aids in determining the liquidity risk associated with a company’s operations.

Example

Let’s work through this using a hypothetical example. The information below comes from the financial accounts of Company X, a fictional retailer. All figures are expressed in millions of dollars.

| Item | Fiscal Year 2021 | Fiscal Year 2022 |

| Revenue | 9,000 | Not needed |

| COGS | 3,000 | Not needed |

| Inventory | 1,000 | 2,000 |

| A/R | 100 | 90 |

| A/P | 800 | 900 |

| Average Inventory | (1,000 + 2,000) / 2 = 1,500 |

| Average AR | (100 + 90) / 2 = 95 |

| Average AP | (800 + 900) / 2 = 850 |

The CCC is now calculated using the formulas above:

DIO = US$1,500 / ($3,000/ 365 days) = 182.5 days

DSO = US$95 / ($9,000 / 365 days) = 3.9 days

DPO = US$850 / ($3,000/ 365 days) = 103.4 days

Therefore, CCC = 182.5 + 3.9 – 103.4 = 83 days

So, What’s Next?

As you know by now, CCC isn’t really significant on its own. It should instead be used to track a company’s performance over time and to compare it to its competitors.

When measured over multiple years, the CCC can reflect an improving or deteriorating value.

For example, if Company X’s CCC was 90 days in fiscal year 2023, the company has improved between the end of fiscal year 2023 and the end of fiscal year 2024

While the difference between these two years is positive, a considerable change in DIO, DSO, or DPO may warrant more study, such as a look back in time. So To get the best picture of how things are changing, look at CCC changes over multiple years.

For the same time periods, CCC should be determined for the company’s competitors.

For example, Company X’s competitor, Company Y’s CCC for fiscal year 2023 was 100.9 days (190 + 5 – 94.1).

Read Also: Accounts Payable vs Accounts Receivable Detailed Comparison

Company X outperforms Company Y in terms of moving goods (lower DIO), collecting what it owes (lower DSO), and keeping its own money for longer (higher DPO). However, keep in mind that CCC should not be the only statistic used to assess the company or management; ROE and ROA are also useful tools for measuring management effectiveness.

Assume that Company X has an online retailing competition, Company Z. This will make things more interesting. Company Z’s CCC over the same time period is -31.2 days, which is negative.

This means that Company Z does not pay its suppliers for the commodities it purchases until it is paid for the goods it sells. As a result, Company Z doesn’t need to keep as much inventory and can keep its money for longer. In terms of CCC, online retailers typically have an edge, which is another reason why CCC should never be utilized in isolation from other metrics.

Cash Conversion Cycle Specific Considerations (CCC)

The CCC is one of various tools that can be used to assess management, especially if it is measured over multiple eras and competitors. CCCs that are decreasing or constant are a good sign, whereas rising CCCs demand a little more investigation.

CCC is most effective when used by retail businesses with inventories that are sold to customers. Meanwhile, consulting firms, software firms, and insurance firms are all examples of enterprises for which this statistic is useless.

Negative Cash Conversion Cycle (CCC)

At the end of the day, a positive cash conversion cycle, even if low in comparison to comparable organizations, is still a “use” of capital. Certain companies might have negative CCCs, which indicates the net impact is a cash “source.” This is a rare occurrence. Turning over inventory frequently and getting cash payments for products sold before paying suppliers would result in a negative CCC.

Amazon is one of the most frequently mentioned examples of a company with a negative CCC. Due to the time lag, Amazon was able to effectively finance its operations by having a negative CCC, which allowed it to take advantage of attractive delayed payment terms with suppliers; but, unlike typical debt financing, this came with no interest.

This freely accessible capital helped support Amazon’s growth plans and had a significant part in developing the company into what it is today, despite the fact that it was an unsuccessful corporation with steep losses. Amazon had a substantially lower CCC that went below zero, even when compared to other market leaders such as Walmart, which are known for their efficiency.

What Is CCC?

The cash conversion cycle (CCC) – often known as the cash cycle – is a working capital indicator that measures how long it takes for a company to convert cash into inventory and then back into cash through the sales process.

What Are Examples of Negative CCC

Amazon is one of the most frequently mentioned examples of a company with a negative CCC. Due to the time lag, Amazon was able to effectively finance its operations by having a negative CCC, which allowed it to take advantage of attractive delayed payment terms with suppliers; but, unlike typical debt financing, this came with no interest.

How Does Cash Conversion Cycle Affect Profitability?

A low or (better still) negative CCC depicts a good conversion cycle. In this case, your working capital is not locked up for long periods of time, and your company has more liquidity. Many online businesses have low or negative CCCs because they drop-ship instead of retaining inventory.

What Are the 3 Components of the Cash Conversion Cycle?

There are 3 components to the cash conversion cycle:

- Days Inventory Outstanding (DIO).

- Days Sales Outstanding (DSO)

- .Days Payable Outstanding (DPO).

How Does CCC Affect Profitability?

As a measure of how liquid a company is, the cash conversion cycle (CCC) is the number of days that capital is tied up in business processes. Having a short cash conversion cycle instead of a lengthy one is seen as good for the profitability of a business.