Accounting balance sheet, what is it used for, how to make a balance sheet. And also, balance sheet format, simple balance sheet example, balance sheet template, balance sheet formula, and balance sheet PDF.

DEFINITION OF ACCOUNTING BALANCE SHEET

An accounting balance sheet of a business or organization or company is that part of the financial statement that contains details of the assets, liabilities, equity capital, and also total debt of the business.

It’s safe to say that balance sheets are like snapshots of the financial position of a company at a particular period of time. Most times it is calculated after every quarter, six months to a year of the beginning of the financial year.

The main contents of the balance sheet are the assets and liabilities. What are the assets? “Assets” are those resources that are owned by the business. They can appear in two forms: fixed assets and non-fixed assets.

While liabilities are debts or obligations a company owes or is indebted to They are in form of current and non-current liabilities.

Read also: Financial statement of company+detailed examples

However, these two are not the only content of the balance sheet as another important content includes the owners’ equity or shareholder. In writing a balance sheet you should know that assets and liabilities are always equal to the owners’ equity. It is called the book value of a company. For a balance sheet to be able to show its true results and meaning both the assets and liabilities should tally (assets=liabilities + equity).

The balance sheet is a financial statement that contains the basis of the company’s return. And, as well, evaluates its capital structure as well.

USES OF ACCOUNTING BALANCE SHEET

They are several uses of an accounting balance sheet and they include:

- The balance sheet reveals the financial status of a business for a particular period of time.

- The balance sheet shows the assets, liabilities, and equity of a company.

- When the fixed assets subtotal is compared to the current liabilities subtotal, you can know if a firm or business has enough funds in the short term to pay off its short-term obligations.

- One of the uses of accounting is to compare total debts to total equity to determine if its equity ratio indicates high borrowing level.

- The total of fixed assets, when compared with sales, will result in a fixed assets turnover. When these turnovers are compared to best-in-class businesses, you will determine if your fixed assets investments have been too high or low as the case may be.

- The major and most important or relevant use of the accounting balance sheet is that it shows the financial state of a business. And, all other uses would be important depending on their own needs.

HOW TO MAKE AN ACCOUNTING BALANCE SHEET

REPORTING PERIOD AND DATE

Making your balance sheet count means you should determine the date and period the balance is representing. However, reporting day is always the final day in an accounting year when the assets and liabilities are. And, also the equity of a company are been reported. Although some publicly traded companies report on a quarterly basis. When that is the case the reporting date will be the final date of the quarter such as March 31, June 30, September 30, and December 31.

Companies that make their financial statement reports annually. Will always report on the 31 of December.

ASSET IDENTIFICATION

Analysts prefer splitting assets into two forms for their better understanding as well as easy identification of their various sources. After the identification of your reporting date, you will need to ensure your assets are also tallied to that same date; it will also be required for their final analysis.

Assets are of two forms, namely. Fixed and non-fixed assets are classified in terms of individual line items and total assets.

FIXED ASSETS

- Cash and cash equivalent

- Short-term marketable securities

- Accounts receivable

- Inventory

- Various other fixed accounts

NON-FIXED ASSETS

- Long-term marketable securities

- Property and goodwill

- Intangible assets

- Various non-fixed assets.

KNOW YOUR LIABILITIES

Knowledge of your liabilities is one thing arranging them into both line items and totals is another thing. Either way for liability to count in a balance sheet, it should be properly stated as well as applied in the correct manner.

CURRENT LIABILITIES

- Accounts payable

- Accrued expenses

- Deferred revenue

- Commercial paper

- Current portion of long-term debt

- Various current liabilities

non-current liabilities

- Deferred revenue

- Long-term lease duties

- Long-term debts

- Various non-current liabilities

These liabilities should be sub-totaled and then totaled together to get an accurate result.

The stock of these would be pretty much straightforward if the business involves a single owner. Lines for this section of the balance sheet include:

- Common stock

- Preferred stock

- Treasury stock

- Retained earnings.

Comparison of total assets against total liabilities plus equity is a must-do. For the balance sheet to be balanced. In a case where the balance sheet is not as balanced as expected. You should double-check your data input. Check for miscalculation, wrong inputs, omission, duplication, and accurate data.

Read Also; PRICE ELASTICITY OF DEMAND: What You Should Know

FORMAT OF AN ACCOUNTING BALANCE SHEET

Majorly we have two ways to express the format of an accounting balance sheet. However, these two formats are the account format and the report format. Whichever format is your choice between the two, just ensure you apply the format approximately to get the best and most accurate results.

The account format of the balance sheet divides its balance sheet into left and right sides like a T account. The assets are listed on the left while both owners’ equity and liabilities are listed on the right side of the balance sheet. When this particular format of the balance is entered correctly the elements of the left side should be equal to the total of the elements of the right side.

A report format of a balance sheet is quite different from the account format. In the report format of a balance sheet elements are vertical in the assets sections at the top while the liabilities and owners’ equity are below the assets section.

The only major difference between these formats of a balance sheet is the horizontal and vertical placement of the elements. However, any format is acceptable so long as you apply it correctly.

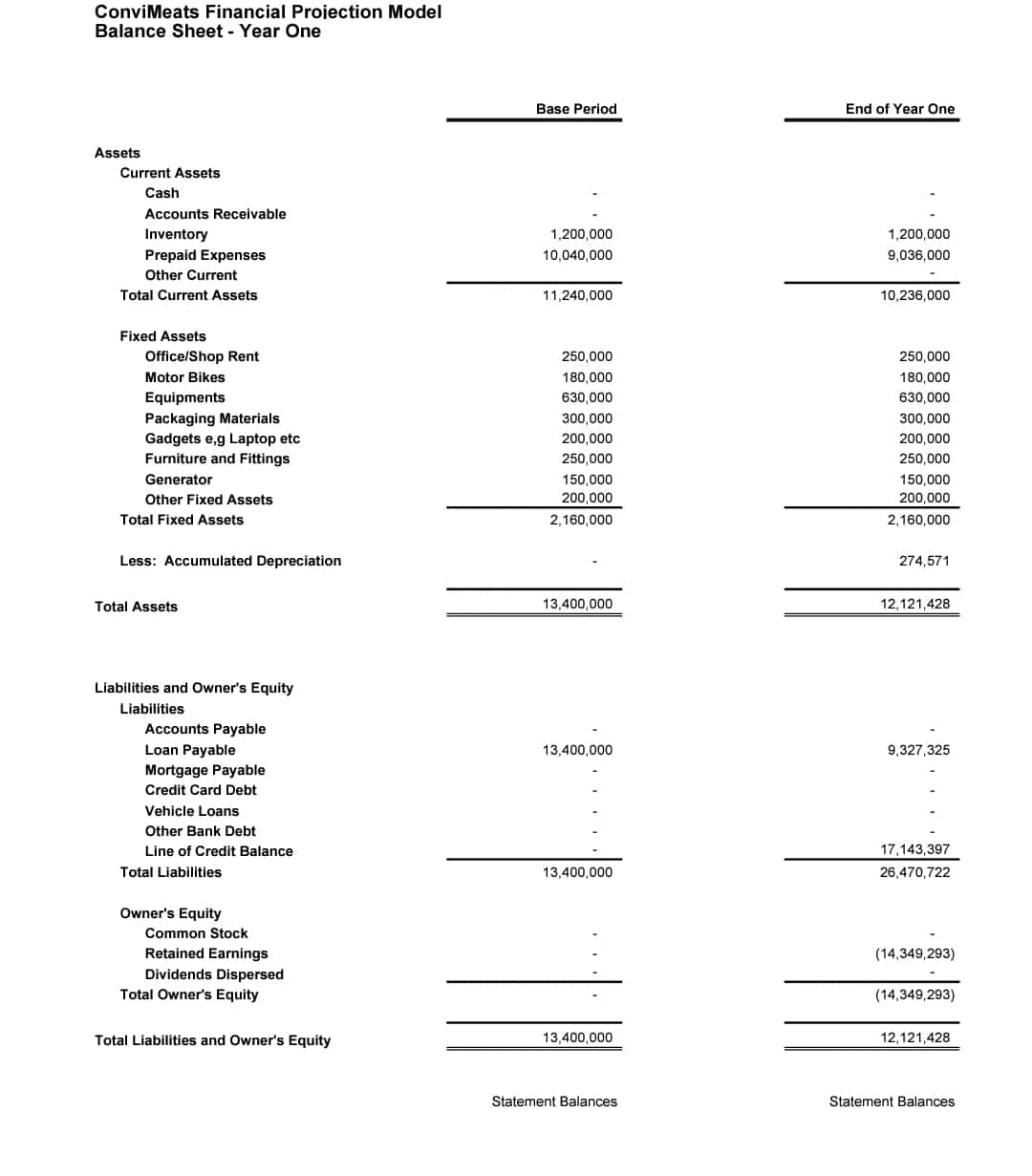

SIMPLE BALANCE SHEET EXAMPLE

A balance sheet is the easiest to recognize in the three financial statements of accounting because of its feature of assets, liabilities, and owners’ equity. And an example of a balance sheet should definitely contain these lists.

Here is a simple example of what a balance sheet looks like and what you require to see or prepare while dealing with a balance sheet.

This balance sheet example contains mainly the assets, liabilities, and shareholder’s equity. Because they are the main contains the accounting balance sheet.

Read Also: HOW TO PREPARE AN INCOME STATEMENT: Definition, Format, & Step by Step Guide

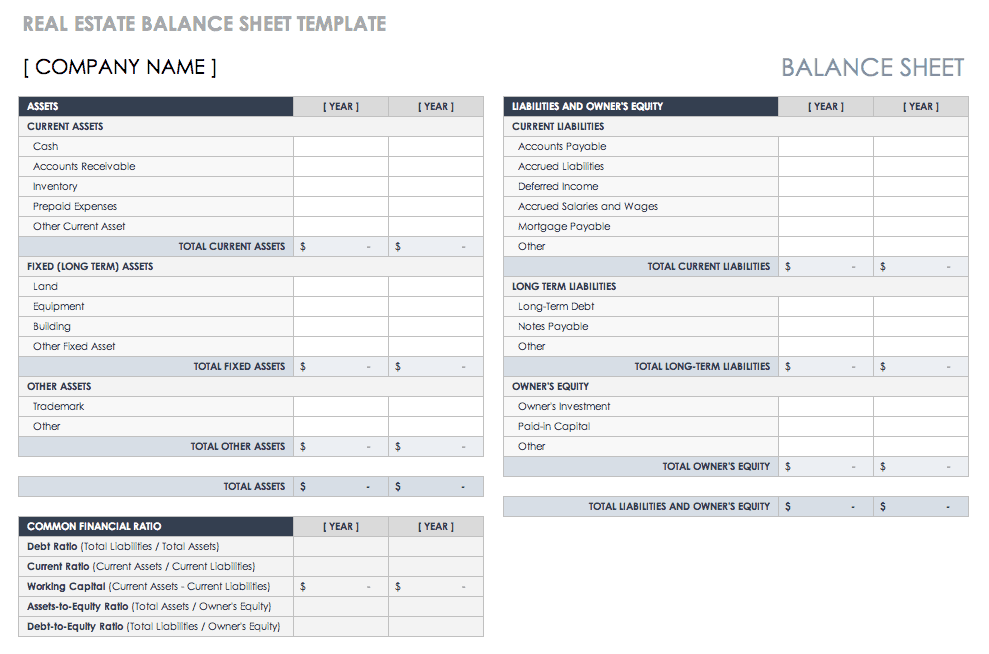

TEMPLATE OF A BALANCE SHEET

A template of a balance is a balance sheet with the absence of the figures. Meanwhile, the simple purpose of these templates is to guide you through your preparation of the balance as well as make work easier for the person preparing the balance sheet.

Knowing what you should expect in a balance sheet is one step ahead while the actual preparation of the balance sheet is another. However, here is a guide to preparing that balance sheet today.

BALANCE SHEET FORMULA

If knowledge of the balance sheet is important then its formula should be fundamental since knowing the balance sheet is waste without the result. Hence I am going to state a clear formula for the balance sheet in this post.

The formula is based on an entire double-entry accounting process. And equation states that the total number of assets is equal to liabilities plus owners’ equity. Thus total assets= liabilities + owners equity

BALANCE SHEET ANALYSIS FORMULAS

Basically, there are some formulas that help in the analysis of the balance sheet and they are as follows

- Working capital: its formula states that current asset- current liabilities while working capital per dollar of sales = working capital/total sales

- Current ratio: formula is current assets/ current liabilities while acid test =current assets –inventory/ current liabilities

- Debt to equity ratio: formula states debt to equity ratio= total debt/shareholders equity.

What are assets vs liabilities?

In its most basic form, your balance sheet can be broken down into two categories, assets and liabilities. A company’s assets are any possessions that have the potential to provide future financial gain. Your debts to other people are called liabilities. In other words, assets increase your wealth, while obligations decrease it.

What are the 3 main components of a balance sheet?

Three items make up a balance sheet: assets, liabilities, and shareholder equity.

What is the purpose of a balance sheet?

A balance sheet provides you with a quick overview of your company’s financial situation at any given time. A balance sheet, along with an income statement and a cash flow statement, can aid business leaders in assessing the financial health of their organization.

Is a car a liability or asset?

Your car is a depreciating asset according to accounting standards. This implies that your car might be worth something right now, and you could sell it. While you own the car, though, that value often decreases with time.

Is cash an asset or liability?

In a nutshell, yes—cash is the top item on a company’s balance sheet and a current asset. The easiest way to acquire other assets is by using cash, which is the most liquid sort of asset.

What is asset vs liability vs equity?

All the things your company possesses are its assets. What your company owes to owners and third parties are its liabilities. The guiding principle of accounting is that assets must equal liabilities plus equity in order for your books to balance.

BALANCE SHEET PDF

Balance sheet and financial statement topics will always need more information such as PDFS and books or eBooks for a better understanding and clarification. PDFS on a balance sheet will always be advisable for learners seeking to advance in their knowledge of balance sheets.

The balance sheet and financial disclosures

The PDFS made available is for the knowledge of the balance sheet. Balance sheet PDFS are all the extra readings you need.

CONCLUSION

This post should be a major if you seeking knowledge of balance. Already, we know a financial statement can’t be possible without a balance sheet present. You wouldn’t need to be an accountant or a financial person to prepare a balance sheet, going through this post, you will be able to easily prepare and understand a balance sheet. Running a business or a company balance sheet will definitely be of need at the end of each accounting year.