If you’ve ever made an online or phone purchase using a credit card, you’ve probably been asked for your card’s security code. This is a short number sequence found on your physical card that is distinct from your credit card number. Providing this code provides additional assurance that the card is in your possession and that your payment information is not being misused. This blog post will define and investigate what a debit and credit card security code is and its importance.

What is a Credit Card Security Code?

A credit card security code is a three- or four-digit code that is unique to your card. The security code is known as the Card Verification Value (CVV), Card Verification Code (CVC), or Card Identification Number (CID), so you may hear it referred to as the CVV code, CVV number, or CVC number.

This number is printed on your card and is not accessible via your online credit card account or any credit card documents. Because this code is only found on your physical card, merchants will ask for it if your card isn’t present to ensure that you have the card in hand.

Merchants are not permitted to save credit card security codes after completing transactions. While thieves may be able to steal credit card numbers by hacking into a retailer’s electronic records, they should not be able to access security codes.

How to Find Your Security Code

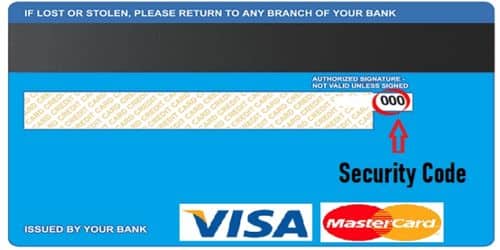

Depending on which network your card is in, you can usually find your credit card’s security code here. However, the layout varies slightly depending on the issuer and card, so if you don’t find the code where you expect it to be, keep looking for an unembossed three- or four-digit number.

- American Express: four digits on the front of the card, just above the card number.

- Mastercard and Visa: three digits at the right end of the signature field on the back of the card

- Discover: Three digits on the card’s back, in a box to the right of the signature field.

When Will You Need Your Credit Card’s Security Code?

When you buy something online or over the phone, you frequently need your credit card security code. In these cases, not every merchant requests the code, but many do for added security.

You’ll also need the security code the first time you give your credit card information to a mobile payment app like Apple Pay or Google Pay, but you don’t have to give it every time you use the app to pay for something.

When you pay at a card terminal in person, you do not need to enter your security code. You don’t have to provide the security code for each subsequent transaction if you allow a retailer to keep your card information on file and charge future purchases to your card.

Why Are Credit Card Security Codes Necessary?

When it comes to keeping your credit card information secure and private, security codes add an extra layer of protection. As previously stated, merchants are not permitted to store personal CVV data. So, if you are asked to verify your security code, the merchant is simply ensuring that you have the card in your possession. Because this information is never stored, becoming a victim of fraud is more difficult, but not impossible.

What’s the Difference Between a CVV, a CVC, and a CSC?

All of these terms refer to the same three or four-digit security code found on the back of your credit or debit card (the front of American Express cards). CVV is an abbreviation for “card verification value,” and CVC is an abbreviation for “card verification code.” CSC is an abbreviation for “card security code.”

This security number may even be referred to as a CVV2, or “card verification value 2” by some financial institutions. But don’t confuse the CVV with the obvious missing CVV1, which is different and is encoded into the magnetic stripe of the card. Typically, the CVV2 is associated with Visa and MasterCard.

The security code on some Discover and American Express cards may even be referred to as a CID, “card identification” or “cardID.”

Alternatives to Credit Card Security Code

We have now entered the age of digital wallets, which do not use the security codes we’ve been discussing, as technology advances at an exponential rate. Instead, these virtual wallets, such as Apple Pay, generate a unique identification code each time you make an online or in-store purchase.

This dynamic security code, also known as a CVV3 or token cryptogram, replaces but serves the same function as a credit card security code, ensuring that the payment account belongs to you. Tokenization refers to the use of these proxy security codes. EMV chip and contactless card transactions use these types of codes. Tokenized transactions are more resistant to fraud than magnetic stripe transactions. However, traditional security codes can still be used with contactless cards.

Debit Card Security Code

It’s easy to see why people like debit cards. A debit card can help you avoid carrying cash or writing checks, help you avoid paying interest on purchases, and possibly help reduce the risk of overspending.

But, because debit cards are directly linked to a bank account—and the money in that account—keeping them secure is especially important. Let’s take a look at a common security measure used by card companies to help protect debit cards: the debit card security code.

What is a Debit Card Security Code

Your debit card, like a credit card, has multiple sets of numbers printed on it. There’s the card number, which is usually a 15- or 16-digit number on the front of your card. Additionally, your card may have issued and expiration dates on the front.

A debit card security code is a three- or four-digit number found in the signature box on the back of the card, below the magnetic stripe. This number is also known as a card verification code, or CVC, or a card verification value, or CVV.

A card security code can be added to both debit and credit cards. Some card companies, such as American Express, display this code on the front of the card. However, there are significant differences in terms of security when you swipe that magnetic strip with a debit card versus a credit card.

When you use a debit card to buy something or pay a bill, you’re using your own money, which is drawn directly from the bank account to which the card is linked. Using a credit card is essentially borrowing money from the card issuer to make a purchase or pay a bill.

What Is the Function of a Debit Card Security Code?

Because your debit card is directly linked to your bank account (or a specific amount of cash if you use a prepaid debit card), you must protect it as carefully as you would cash.

A debit card security code is generally only one layer of security for card transactions; you may be asked for it if you make a purchase online or over the phone. The merchant is attempting to verify that you are the cardholder or authorized user by asking for this code, along with your account number and other information. This is because you’ll usually need to have the card on hand to share this code.

A debit card security code differs from the personal identification number, or PIN, that you chose when you received your card and enter when you withdraw money from an ATM or make an in-person debit purchase.

It also differs from the unique code generated by EMV chip cards to help prevent fraud. When you insert your card into the card reader, the chip on the front is read. The reader scans the chip, you enter your PIN or sign, and the chip generates a unique code for that specific purchase. You never see this unique code, unlike the security code on the back of your card.

Along with your card number and expiration date, it’s critical to safeguard your debit card security code because someone can use it to make a fraudulent purchase with your card — even if they don’t have the card in their possession.

Importance of Security Code of a Debit Card

The Security Code adds an extra layer of protection to your cards account and is just as important as password security, which is required to access and secure your account. The CSC assists in validating your account and protecting you while placing an online order.

It is recommended that you secure your card security number because if someone obtains this number, they may use your money fraudulently. So, don’t give out your CSC number to anyone, and if your debit card is stolen or lost, contact your card issuer right away to recover your security code as well as your debit card.

Is the security code the same as CVV?

A card verification value (CVV) is a security code that helps protect you from credit card fraud. A CVV number can also be referred to as a card security code (CSC), a card verification code (CVC or CVC2), or a card identification number (CID).

How do I find the security code on my card?

The security code is a four-digit number that appears on the credit card’s surface in the upper right corner of the card number.

What is 3 digit card security code?

The CVV2 (Card Verification Value 2) is a three-digit security code located at the bottom of the signature panel on the back of your card. CVV2 is typically used in transactions in which the card is not physically presented, such as online purchases.

Is it possible to crack CVV?

After obtaining a valid 16-digit number, the hacker employs web bots to brute force a three-digit card verification value (or CVV) and expiration date to hundreds of retailers at once. The CVV requires a maximum of 1,000 guesses, and the expiry date requires no more than 60 attempts.

How do hackers get CVV?

Hackers can obtain your CVV number in one of two ways. The first is through phishing, and the second is through the use of a web-based keylogger. Phishing. This is a type of online security theft in which sensitive information, such as credit card information, is stolen.

Can you bypass CVV code?

If a merchant requires a CVV code, there is usually no way around it. If you don’t have the physical card, you’ll need to find it or use a different card or payment method to complete your purchase.

Can a CVV code be 000?

The 000 code could be an acceptable CVV number, or it could be a credit or debit card with the CVV number in the format 000.

Can I get my CVV number online?

The only way to determine your credit card’s security code is to possess the physical card and check the code. If you’ve misplaced your credit cards or the security code is no longer legible, contact the issuer immediately. They’ll most likely issue you a new card with a new code.

Do you need CVV to pay online?

A unique 3-digit CVV code is required to complete every transaction made with your credit or debit card.

Conclusion

A credit card security code is a three to a four-digit number that can be found on the back of your card. It is used to confirm and complete transactions, so knowing it is essential when shopping online. With this guide, you should have a better understanding of what it is, where you can find it, and why it is used.

If you are having trouble accessing your credit card’s security code, please contact your provider. This should allow you to solve your problem quickly, securely, and conveniently.

Card Security Code FAQs

Is CVV 3 or 4 digits?

The CVV code is the last three digits after the credit card number on the back of the card in the signature area. Please contact your credit card issuer if your card does not have a CVV code or if you are unable to read the CVV code.

What if someone knows my CVV number?

Each of these cards has a card verification value (CVV) printed on the back or front of the card, and with access to the CVV, full card number, customer name, and expiry date, fraudsters can easily wipe out money from customers’ bank accounts by engaging in online transactions with other people.

Can I change my CVV number?

CVVs are generated automatically by the credit card company and printed on the card. While your debit or credit card may be issued with a PIN at first, it is only temporary. In most cases, you will be required to change it to a specific number. You have no such authority over a CVV.

Related Articles

- ONLINE PAYMENT SYSTEMS: Top 13 Online Payment System & Software in UK

- Available Credit: What Does It Mean on a Credit Card

- Company Credit Card: Company Credit Card and Policies

- IDENTITY MANAGEMENT SYSTEM

- WHAT IS EMPLOYMENT VERIFICATION: All You Need To Know