In this article, we will learn the relationship between the minimum variance portfolio and global, provide formulas to determine the minimum variance portfolio weights, calculator, and provide an Excel sheet that implements the approach.

The minimum variance portfolio or minimum risk portfolio is a risk-based approach to portfolio construction. This means the portfolio is constructed using only measures of risk. It is also an investing method that helps you maximize returns and minimize risk. This involves diversifying your investments.

One reason why you as an investor might want to go for a risk-based approach is the fact that you can’t easily estimate expected or future returns. But your risk might be easier to estimate. This leads to a more robust portfolio that is less subject to estimation risk.

Let’s help you learn how to choose the right securities to build your portfolio.

What is a Minimum Variance Portfolio?

A minimum variance portfolio is one that maximizes performance while minimizing risk. It can hold volatile investment types on their own, but when combined, create a diversified portfolio with lower volatility than any of the individual parts. But the strategy is simple to implement.

In other words, A mini variance portfolio holds individual, volatile securities that don’t correspond with one another. One security may rise in value while another drops straight down at high speed, it isn’t important so don’t panic. Consequently, because of their low correspondence, the portfolio as a whole is seen as less risky. But how? You will find out if you keep reading…

Any two investments with a low correlation to each other can form a mini variance portfolio. An example of a mini variance portfolio is a stock mutual fund and a bond mutual fund. Variance is a measurement of risk.

Variance

This measures the daily movements of an investment. The more significant the price change, the higher its variance, and the more volatile it. For example, bonds have lower volatility than stocks and low variance. The standard deviation of an investment is the square root of the variance – both measure portfolio risk.

So when people talk about what a wild ride the stock market is, that’s what they mean. One day your stock is up 24%, the next it’s down -5%.

However, if you observe the Dow from 1900 through the present, you will notice that the market always goes up.

Moreover, each investment in a mini variance portfolio is risky if traded individually, but the risk is guarded when traded in the portfolio. The term originates from the Markowitz Portfolio Theory, which suggests that volatility can be used to replace risk and, therefore, less volatility variance correlates with less investment risk.

How Does Minimum Variance Portfolio Work?

As earlier mentioned, there are two ways to create a portfolio with a low volatility. Basically you can either pick a few volatile investments that have little link with one another, or stick with low-volatility investments. For instance, investing in the tech and fashion industries is a typical scenario for creating this kind of portfolio.

Low correlation investments are ones that perform differently from the market.

Utilizing mutual fund categories that have comparatively low correlations among one another is a popular strategy for creating a portfolio with a minimum volatility. This adheres to a core and satellite portfolio structure, with a possible allocation like this:

- S&P 500 index fund at 40%

- Emerging markets stock fund at 20%

- 10% fund for small-cap stocks

- Index fund for bonds worth 30%

Although the first three fund categories can be somewhat volatile, there is little link between the four. The volatility of the four of them combined is lower than that of any one of them individually, with the probable exception of the bond index fund.

Correlation Measurement

When creating this kind of portfolio, understanding correlation measurement is helpful. You can achieve this by keeping an eye on a statistic called “R-squared” or “R2.”

The R-squared is mostly predicated on the correlation between an investment and a significant benchmark index, such the S&P 500.

If your investment’s R2 in relation to the S&P 500 is 0.97, then changes in the S&P 500 can account for 97 percent of your investment’s price movement (ups and downs in performance).

On the other hand, suppose you own an S&P 500 index mutual fund and wish to lower the volatility of your portfolio. In that situation, holding additional investments with a low R2 would also be a good idea. This means that if the S&P 500 were to begin to decline, the impact could be lessened by your low-R2 holdings. They won’t fluctuate in response to the performance of the S&P 500.

Bond prices may be flat or even slightly negative while stock prices are growing, but they often increase when stock prices are decreasing.

Although stocks and bonds rarely move in the same direction, their performance is largely uncorrelated.

Using This Approach with Stocks

If funds are not your thing, you might want to think about investing in US large-cap stocks, US small-cap companies, and US emerging countries stocks.

Each of them has a history of erratic price volatility, a high relative risk, and little linkage to the others. In the long run, compared to a portfolio made up only of one of those three stock categories, their low R2 results in decreased volatility.

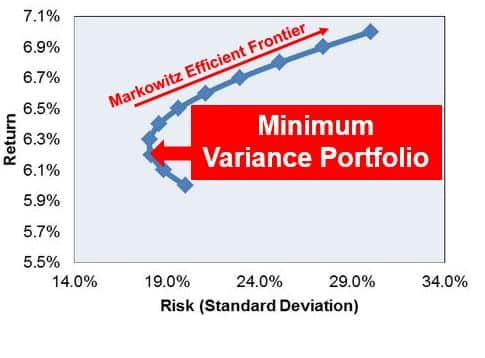

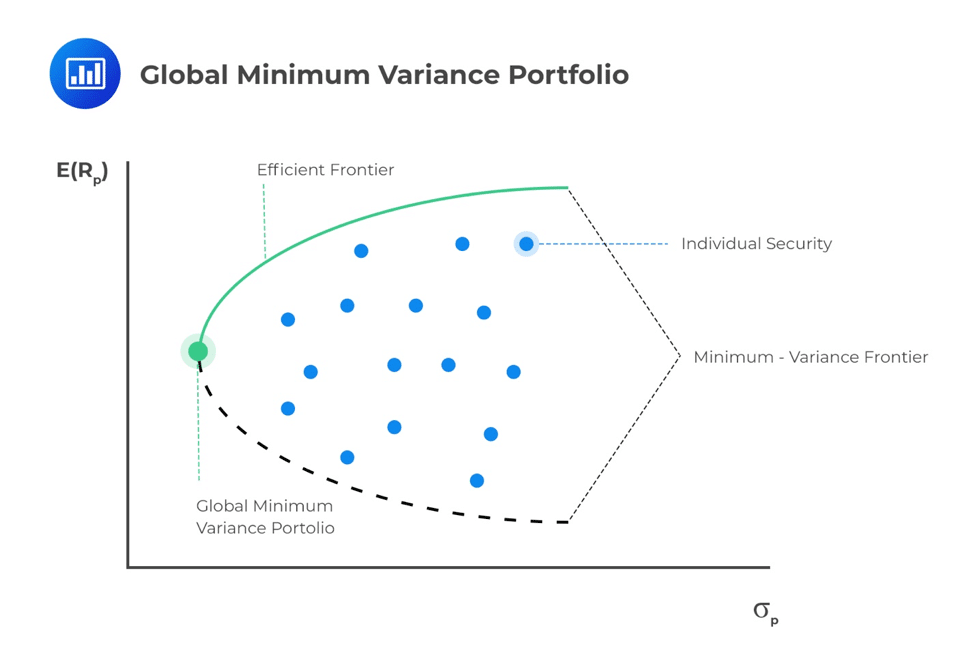

GLOBAL MINIMUM VARIANCE PORTFOLIO

The global minimum variance portfolio is related to modern portfolio theory and the efficient frontier. In particular, it is a unique portfolio that is on the efficient frontier. It is also clear from the figure that the portfolio with the lowest standard deviation constructs from the set of securities that the investor can invest in.

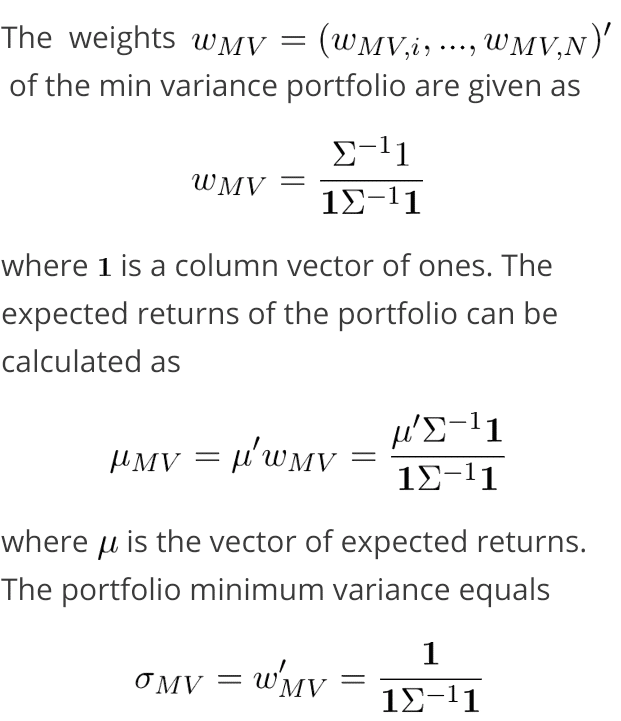

FORMULA MINIMUM VARIANCE PORTFOLIO

To calculate the MVP weights, we can make use of the following MVP formula. To do this, all we need is the covariance matrix. It is important to note that we do not need the expected returns to determine the weights.

MINIMUM VARIANCE PORTFOLIO CALCULATOR

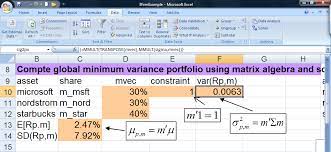

The above formulas provide a closed-form solution to calculate the global MVP. It can easily be calculated using software that allows for matrix algebra. In Excel, we can also calculate the min var portfolio using Excel’s Solver.

MINIMUM VARIANCE PORTFOLIO EXCEL

Minimum variance portfolio excel can be calculated on an excel spreadsheet. Here is a good example below.

How Does it Work?

Generally, there are one or two things to do inorder to hold a good minimum varince portfolio. The first is to settle for a low volatility investment or settle for some volatile investments with low or negative correlation to each other.

Can Minimum Variance Portfolio Be Optimal?

Can a minimum variance portfolio be optimal? Minimum variance weighted portfolios are optimal if all investments have the same expected return, while Maximum Diversification weighted portfolios are optimal if investments have the same Sharpe ratios.

What Is Minimum Variance Portfolio Standard Deviation?

The minimum variance portfolio (MVP) is the portfolio that provides the lowest variance (standard deviation) among all possible portfolios of risky assets.

What Is Global Minimum Variance Portfolio?

The global minimum variance portfolio is the portfolio that provides you with the lowest possible portfolio volatility, for a number of underlying assets. … The er argument: the expected returns of the underlying assets ( mu_hat_annual thus in this case).

How Much Should You Spend on Stock a to Achieve the Minimum Variance Portfolio?

This means, to achieve a minimum variance portfolio that is invested in Stocks A and B, you should invest 74.42% in Stock A and 25.58% in Stock

Conclusion

It is often said that slow and steady wins the race. Rather than risk your fund in hope of a huge return, consider spreading your investment across bond, stock and cash. Keep it at minimum risk level using MVP. It is much safer and also yield great returns on your investment with minimum risk.