Once upon a time checks were the most common form of transacting businesses in the history of financial institutions. Now? Not so much. Either way, it doesn’t totally rule out the fact that individuals still use them every now and then. It makes endorsing them a big deal.

Simply put, you should know how to endorse a check if or when someone gives it to you. This will give you the luxury of either being able to cash it, deposit it or hand it out to someone else. When done correctly, endorsements make it simple to use checks. Conversely, the wrong move could get you into a deep mess. So it’s important that you do this rightly. But before we move any further, let’s go through some vital information about checks you should know.

What is a Check?

A check is a piece of paper in form of a slip that instructs a bank or credit institution to pay a specific amount of money to a particular set of individuals. This could include businesses, organizations, government bodies, or other entities.

For starters, a check must have a date, the payee’s name, the amount, and an authorized signature for the checking account from which the funds will be withdrawn in order to be valid. The payee is the person who receives the money.

On the other hand, the payee must sign or endorse the back of the check in order to receive the funds. Basically, an endorsement tells the bank or credit institution that the person who signed the check is the payee and wants to accept the funds.

Why Is It Necessary to Endorse Checks?

When you receive a check, it is made payable to you. In other words, you’re the only one that has the legal authority to withdraw funds from the checkwriter’s account. However, handing over that check to your bank and letting them handle it is the simplest way to cash it.

You allow the bank to receive payment by endorsing a check. The bank then has the authority to negotiate the check on your behalf.

But there are also scenarios where you can deposit a check without endorsing it. This may be an option if the check is small. There are other conditions though, you must deposit it into an account with the same name as the payee, and it should not be from an insurance company or other organization that requires endorsement. These unendorsed checks are routinely accepted by banks, with the assumption that no problems will arise.

However, if getting paid quickly is critical, it’s best to endorse checks properly and thoroughly. Even if your bank allows you to deposit a check, the check may bounce after several weeks, causing the bank to deduct funds from your account until the matter is resolved.

How to Endorse a Check

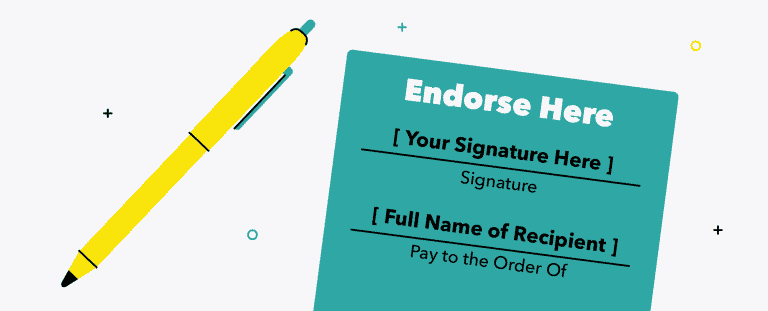

Simply turn the check over and sign your name on the back to endorse/approve it. The back of most checks has a slot for your endorsement. There are a couple of blank lines and a “x” where you can sign your name. The back of the check can also say “Endorse here” and “Do not endorse / sign/stamp below this section and so on.” The notice is there because the bank stores check-processing data on the back of the check, below the endorsement. If you’re unsure how to endorse a check, contact your bank or credit institution for assistance.

In any case, endorsements can be done in three different ways:

Blank Endorsement

The phrase “blank endorsement” can be misleading because it does not necessarily imply that an endorsement is empty. Rather, it denotes that the endorsement contains only the payee’s signature and no further guidance.

Restrictive Endorsement

This form of endorsement requires the signature as well as the words “for deposit only,” indicating that the check can be deposited but not cashed. Writing “for deposit only,” also means that you will have to include a bank account number where it can be deposited. To deposit a check remotely with a mobile banking app, some banks ask payees to accept a check with the phrase “for mobile deposit only.”

Full Endorsement

This form of endorsement results in a “third-party check” that you can send to someone else to approve, cash, or deposit it. It requires that you write “Pay to the order of” and the name of the individual who will receive the funds, and then sign your name under that instruction in the endorsement area.

A check written in pencil should never be endorsed because it can be erased. The best ink to use is blue or black, which will show up well and clearly on the back of most tests.

Mobile Endorsement on a Check

When depositing a check with your phone, certain banks will need you to add “Mobile Deposit” to the endorsement. However, for mobile deposits, several banks will allow different endorsement styles. Check with your bank to see if a specific mobile endorsement is required.

Business Endorsement on a Check

If a check is made payable to a business, the check must be signed on behalf of the business by an authorized person using the procedures below;

- Sign the business’s name exactly as it appears on the pay-to line.

- Sign your name.

- Include the company’s name in your title (Owner, Accountant, etc.)

- Any limits, such as “For Deposit Only,” should be added.

FBO—For the Benefit of—Endorsement on a Check

Checks are sometimes made payable to a person or company for the benefit of someone else. Someone might, for example, write a check to an assisted living home for the benefit of a family member who is elderly or has special needs. This is what the “Pay to the Order Of” line might look like:

1. Assisted Living Facility FBO Jane Smith

2. Assisted Living Facility for the Benefit Of Jane Smith

Writing an FBO check ensures that funds are used for a certain purpose, but in this situation, the money is held by the assisted care home as the custodian. The check is signed by the custodian.

Some banks demand that both parties sign the check. To learn how to write an FBO check for them, consult your bank and the organization receiving the check. But then, it can be complicated if the bank demands both signatures and the person who will benefit from the check is unable to endorse it.

Common Issues With Endorsing a Check

Though endorsing a check appears to be a simple process, it can be fraught with complications. These can cause your bank to take longer to process checks or possibly stop them from being processed at all.

#1. Match Name on Check

The name on the endorsement must match the name on the front of the cheque (“Pay to the Order Of…”).

#2. Name has a misspelling

If someone offers you a check and misspells your name, endorse the back of the check with the incorrect spelling, then sign your name on the back of the check with the proper spelling.

#3. Multiple Payees

Look for “and” or “or” in the pay-to line if the check is made out to numerous recipients. If the cheque is made payable to “John and Jane Smith,” both John and Jane must sign it. If the cheque is made payable to “John or Jane Smith,” either John or Jane can sign it. When people offer a check inside a wedding card, this is a typical occurrence. Make sure you’re endorsing the check correctly by looking at the pay-to line.

When Is It Appropriate to Endorse a Check?

Until you’re ready to cash or deposit a check, don’t endorse it with just your signature. When a check is endorsed in this way, it becomes negotiable, meaning it can be cashed or deposited by anyone who presents it to the bank, even if they aren’t the payee.

Your home or office may appear to be a secure location to hold a ready-to-cash check, but there may be people present who take your check and cash it. Family members, contractors, caregivers, babysitters, and delivery people are just a few examples.

In other words, take as much time as you can before signing a check, regardless of the method you use to endorse checks.

It’s best if you sign while you’re at the bank or in the middle of a mobile deposit.

If you endorse checks and they go missing, it’s much easier for someone else to cash the check or attempt to deposit it into their account.

Is Depositing Someone Else’s Check Into Your Account Allowed?

A friend or family member may ask you to deposit their cheque into your account at some point in your life. This could be due to their inability to deposit the check or their desire to transfer the funds from the check to you directly.

Many banks and credit unions, in general, accept this. However, before you begin the process, you should consult with your financial institution. It is possible that the check will be canceled if you do not follow their regulations.

Call your bank and let them know you’re going to deposit a cheque made out to someone else. Inquire about what you need them to write on the back of the check, and whether you both have to be there to deposit it. Some banks need a form of identification from the opposite party in order to verify the identity of the person signing the cheque.

What Is the Procedure for Endorsing a Check to Someone Else?

You’re the only one who can do anything with a check that’s been made payable to you. But to a large extent, you can sign the check over to someone else (so they can cash or deposit it). This procedure, however, comes with a number of risks. In the end, if everything goes well, someone else should be able to use a check made out to you.

Will the Bank Give You Permission?

like we earlier mentioned, there is a possibility that checks that have been signed over to a third party may not be accepted by banks. I mean somebody besides the check writer and the original payee. It’s perfectly legal to try, but banks aren’t obligated to follow your instructions. Some banks have policies prohibiting this practice. So they perceive a third-party check as a red flag, in which case they may refuse to deposit or cash the check.

If you plan on signing a check over to someone else, make sure they check with their bank before you accept the check.

You don’t want to clutter the back of the check with extra signatures and names (which can create confusion and delays the next time you try to cash the check). Secondly, find out if it’s legal and what the conditions are.

When you use this method, banks are actually giving your money to someone else. Regrettably, the danger is often too high for them to bear. When a bank is unable to check your identity or signature, they must depend on the word of a third party.

How Do You Endorse a Check to Someone Else

Verify that a bank will approve a check before signing it over to another individual or a company. If you get approval, sign at the back of the check as an endorsement. Some banks require you to write “Pay to the order of [Person’s First and Last Name]” under your signature, while others only require the person depositing the check to sign their name under yours. Once that person has signed the check, give it to them to deposit or cash.

See this in a clearer perspective below;

Step 1: Work Out a Strategy With Your Recipient

Although it isn’t always possible to endorse a check to someone else, you may be able to use this method to pay rent or other monthly costs. But first, check with your recipient to see if they’re okay with this payment method.

Recipients may be concerned that their banks will refuse to accept this payment, even if this is not a regular occurrence. Make sure you communicate before endorsing a check to someone who might not take it.

Step 2: Check With Your Bank Again

When it comes to endorsing a check to someone else, it’s normal for banks to have varying procedures and requirements. Some banks may refuse to provide these services due to the risk of stolen checks or checks being paid to the wrong person. To make this process go as smoothly as possible, contact or visit your bank first.

Also, keep in mind that you may need to contact the bank from whence the cheque was originally issued. The bank’s contact information is usually found on the front of the cheque. When you contact your beneficiary, don’t forget to inquire about any further identification they may need to cash it out.

Step 3: Sign the Check Over to the Recipient Correctly

How do you sign a check over to someone else now? Begin by looking for the endorsement line on the cheque. “Endorse check here” is usually situated on the right or left along with the height of the check.

Once you’ve located it, sign your name on the top line and put “Pay to the order of [recipient name]” beneath it. This indicates to the teller that you have given permission for this check to be paid to a third party. Be careful to write the recipient’s name exactly as it appears on their identity card, as the teller will double-check it before paying it out.

Step 4: Present Your Check

It’s time to give your receiver their payment! If you haven’t previously, share contact information when you meet with your receiver. They’ll be able to notify you if there are any problems, such as the bank not accepting the payment.

If you’re concerned, verify with your recipient to see if the check was received. If you or anyone else in the trade is nervous, choose a more secure option. Certified checks, for example, are approved by banks as a more secure payment method and may be a preferred payment option, particularly for large purchases.

Having Someone Endorse a Check So You Can Deposit It In Your Account

The procedure for having someone endorse a check so you can deposit it into your own account varies from bank to bank or credit union to credit union. In most cases, this entails the person putting your name on the back of the cheque and signing it. Every check includes a designated spot for the payee to write their name or other information.

Typically, this entails writing “Pay to the order of: Your Name” on your cheque and signing their name beneath it. Always double-check with your banking institution to ensure that you’re following the steps correctly.

Having Someone Endorse a Check So You Can Deposit It In Their Account

Because there are no payees to transfer, depositing a cheque for someone into their own account is a little easier.

It’s a good idea to receive a deposit slip from the individual who wants you to deposit the check if at all possible. They can use it to write down their account details and sign the backs of their checks, and everything should go smoothly at the bank. This also ensures that you have a clear record of the funds you placed for the payee.

If you don’t have a deposit slip, have the payee write “For Deposit Only” on the back of their check and sign it.

Alternatives to Deposit a Check

If you or someone you know needs to deposit a check but is unable to do so at a branch, there are alternative less-inconvenient options.

Many banks and credit unions now allow mobile check deposits, which you can encourage a friend or family member to use and then transfer the funds to you once they’ve been processed.

In addition, many credit unions participate in shared branching, which allows members to transact business at locations other than their own.

Keep Your Checking Account Safe

When depositing checks into your account that is not intended for you or that you are unsure of the origin of, you should always be cautious. Even if you deposit a bad check unintentionally, you may find yourself in a difficult situation.

You may face fines if a banking institution decides that you deposited a bad check. For one thing, you can be liable for returning the check to the bank. The bank has the authority to freeze and, in some situations, shut your account. If a check bounces and you use the funds to pay a bill or make a car payment, the payments may be canceled, which will have an impact on your credit score.

In general, you should refrain from depositing checks into your own account unless you are certain they are legitimate. You can verify that the check is for a valid amount by calling the bank that issued it.

Conclusion

When it comes to transferring, cashing, or receiving funds, we can’t be totally safe from fraud. But following the guidelines in this post is a starter. At this point, you should be able to deal with check frauds to a reasonable extent. However, if you have any concerns you would like to air, please reach out in the comment section.

What Does Endorsing a Check Mean?

When someone pays you with a check, you often must sign the back of the check before depositing it into your account. Endorsing the cheque means signing the back of it. What you write on the check when you sign it—how you endorse the check—is determined by what you want to accomplish with it and how it is written.

Do I Need to Endorse the Back of a Check?

For a check to be valid for a deposit, it must be endorsed on the back. So, just before you present it to the bank, write your name in the vacant place next to the X.

How Do You Countersign a Check?

To do so, the payee must sign the check and write “pay to the order of” and the name of the second person on the back. The second individual can then endorse or countersign the check and deposit it. However, most financial institutions hardly accept third-party checks.

What Are the 3 Possible Types oF Endorsing Check?

3 Types of Endorsements

Blank Endorsement. A blank endorsement is made when the back of a check is signed without any further constraints.

Restrictive Endorsement. A restriction endorsement guarantees that a check will be deposited into a certain account. …

Special Endorsement