Just as you should know how to read the front of a check, you should also know how to read the back of a check. That’s where you sign off on it, which is a critical step toward converting it to cash. After all, even in an age of electronic payments, we still commonly use paper checks for crucial transactions such as paying rent, receiving pay, or changing bank accounts.

After you’ve learned the critical details on the front, here’s how to sign the back of the check. You’ll also learn what to write on the back of a check and the consequences of the wrong endorsement for mobile deposits.

What you’ll see on the Back of a Check

The back of a check typically has three distinct parts. However, they may differ depending on who issues or prints them.

#1. Endorsement Area

This is where you sign or endorse the check before depositing or cashing it. This may be as easy as signing the form. However, it’s best to use an endorsement that limits how it can be used. If you lose it or someone steals it after you endorse it, the limitation (such as adding “for deposit only”) makes stealing the money difficult, if not impossible.

#2. Security Screen

This region is only for financial institutions and you cannot use it as a customer. Banks use this room to record the sequence of events that occur when they process the check. You’ll notice that this section is normally written in very light ink (possibly with a line pattern). Thus, it makes it difficult to photocopy and replicate. When the genuine one is used, the words “Original Document” are often written in this space. However, you have to look closely to see it.

#3. Security Box

A security feature that includes an alert that discourages thieves from modifying or copying the check. It also includes advice to help customers decide whether or not a search is valid. It, for example, advises you to look for microprint or watermarks on it.

Who Signs the Back of Check?

There’s a lot of misunderstanding on where signatures go. Is it your responsibility to sign the back of a check when you write it, or is it the responsibility of the recipient?

When you write a check, you just need to sign on the front—right on the signature line. It is possible, however, to provide instructions on the back of a check when writing it. “Hold for deposit until December 30, 2020,” for example. The caveat is that you can never be absolutely assured that your orders will be followed.

If you collect a check, you must sign the back before depositing or cashing it. You could provide guidelines that restrict how it can be used along with your signature. For example, if you’re mailing the check to deposit it into another account, you might write “For deposit only” and then your account number. That way, no one else can cash it if you lose it in the mail.

Is it necessary to Sign the Back of a Check?

If you are receiving rather than writing the check, you may be able to deposit it without a signature in certain cases if it is payable to you. However, it is best to sign the check with a signature. It may be returned to the issuer, resulting in fees and delays in receiving your money.

You’ll have a great chance of missing the signature on personal checks. It shouldn’t be a surprise if the bank hounds you for a signature on company or big checks.

If you’re making a mobile check deposit, some checks have a checkbox to indicate that you’re using a remote deposit service. Some banks instruct you to write something about mobile deposits on your check. You may be able to get away with ignoring those instructions, but it’s best to ask your bank for guidance.

Numbers on the Back of Check

The routing and account numbers on the front of a check are probably familiar to you, but what about the numbers on the back?

Pre-printed numbers in the endorsement area are frequently used as reference numbers to track checks. This is particularly for businesses that print them on blank checks. Numbers outside the endorsement area are inserted by banks that manage it when it is cashed or deposited. Those banks print their details on the check before sending it to the bank that will eventually release the funds.

To endorse, sign your name on the back and provide any additional information needed to process it efficiently. A signature is normally sufficient, but additional measures will help you monitor how banks treat your payment and protect you from fraud.

What to Write on the Back of a Check

#1. Matching names

To be properly endorsed, the name signed on the back of the check must match the payee’s name on the front of the check. If the name was misspelled or written incorrectly, sign it with the incorrect version, then sign again with your correct name.

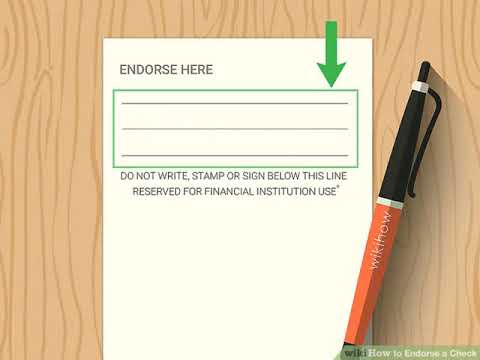

#2. Where to Endorse

Most checks have a 1.5-inch section on the back for you to write in. This is marked with lines and directions that say “Do not write, stamp, or sign below this line”. Try to keep your entire signature and any other instructions for the bank in that region.

Blank Endorsement

The simplest (but also riskiest) way to endorse is to simply sign the check without adding any restrictions. To use that method, known as a blank endorsement, sign your name in the endorsement area. However, only do this if you want to deposit or cash the check immediately after signing.

Mailing, ATM Deposits, and Other Services

If you intend to mail the check to your bank, deposit it at an ATM, or carry it around for a while. You may take a different approach: either keep the check unsigned until you’re ready to deposit, or apply a limit to the endorsement. Blank endorsements are dangerous because someone else could steal the endorsed check and cash it or deposit it to a different account.

Get money into your account via Restrictive Endorsement

A restrictive endorsement ensures that a check is deposited into a specific bank account. To use this form, include your account number with your endorsement. Also, give directions stating that the money can only be deposited into your account.

To do so, write “For deposit only to account #####” (using your account number) as part of your endorsement. If you lose it, thieves would have to change the endorsement. This makes it more difficult for them to get your money. Another option is to write “For deposit only to account of the payee”. This will require thieves to have access to an account under your name.

What Happens if you make a Wrong Endorsement on a Check?

Check endorsement can go wrong in a variety of ways, such as writing your maiden name instead of your married name. Also, you can make a wrong endorsement by signing with a nickname instead of the full name on your bank account.

However, for most financial institutions, the signature on the check is the most important aspect. Without a signature, a check is not valid; thus, if the signature is incorrect, it can indicate to the bank that someone is attempting to commit fraud.

Are you an SEO Expert? Manage your invoice with this SEO Invoice Template and Receipt Maker

How do you Correct the Wrong Check Endorsement?

Endorsing a check means signing the back of it. Consumers can endorse checks because this is the step required to legally transfer funds to the bank. However, another reason to endorse is to improve the security of your funds. You should write “for deposit only” and also include your account number (plus signature) to ensure no one else can use it if you happen to lose it.

If your bank has strict deposit rules, wrong information on the endorsement area of the check can cause problems. For example, since your name must fit the “Pay to the Order Of” line, if anyone incorrectly fills out your name, you must endorse it with the incorrect spelling, and you may also write the correct signature in the endorsement field.

Unfortunately, crossing it out would not work if you wish to change a wrong endorsement, such as switching from “for deposit only” to another endorsement type; technically, there is no way to reverse an endorsement; however, your bank may be laxer about adhering to their own laws, so you may be able to get away with making a change.

Numbers on a Check’s Back

The routing and account numbers displayed on the front of a check are certainly recognizable to you, but what about the numbers printed on the back?

Checks are frequently tracked using reference numbers that are pre-printed in the endorsing area. For firms that print checks on blank check stock, they are extremely useful.

Banks that handle the cheque when it is cashed or deposited add numbers outside of the endorsing area. The checks are printed with the details of those banks, who then forward them to the bank that will actually release the funds.

New guidelines for writing on a Check for Mobile Deposit

With your iPhone® or AndroidTM device, you can make deposits in a flash.

Due to new banking regulations, for all checks that you deposit through a mobile service, you must write the phrase “For Mobile Deposit Only” handwritten below your signature in the endorsement area on the back of the deposit will be rejected.

Although some checks include a preprinted box for mobile deposits, ticking this box does not fulfill the endorsement requirement. Unfortunately, if you deposit a check using a mobile app without writing a signature or this endorsement, it may be denied and the deposit will be deducted from your account.

Does a Cheque Have a Blank Back?

The reverse of the check often has a line for signing and is blank. The check’s back would appear like the image below if the endorsement were left blank. The payee would merely sign their complete name on the check’s reverse. There are no additional restrictions, including those that apply exclusively to deposits or to a certain person.

Does It Matter if a Check Has a Back?

For a check to be accepted for deposit, it must include an endorsement on the back. Therefore, always add your signature to the document right before bringing it to the bank in the spot adjacent to the X.

Is a Check’s Back Required to Be Signed?

Additionally, it may be moved from the initial payee to another payee. The cheque must have the issuer’s signature on both the front and back.

What Is the Name of the Sheet Found beneath a Check?

Duplicate checks are a special kind of check that have a little piece of paper acting as a carbon copy behind each one. Every time a check is written, duplicates are automatically made, making it simpler to maintain records.

Summary

It’s just as necessary to get the back of your check right as it is to get the front right. If you don’t do it correctly, it will be refused or returned to the issuer, just as if you messed up the front. Regardless of if you can get away with not signing the back, it’s always a good idea to endorse the check to ensure that everything goes smoothly.

Back Of Check FAQs

What do i write on the back of a check?

You endorse a check on the back of the check. There may be a simple line or a box that reads: “Endorse Here.” There’s usually another line that says, “Do not write, stamp, or sign below this line.” The endorsement area is typically about 1.5” long and covers the breadth of the check.

Can I cash a check if I wrote on the back?

According to the National Check Fraud Center: Section 3-206: If the back of the check says it is For deposit only, then has the signature of the payee, that is a restrictive endorsement and it should be observed, but the person who affixed that indorsement can waive it.

Where can I cash a check I already signed?

7 Places Where You Can Cash a Personal Check

- The Bank listed on the check. …

- Walmart. …

- Ace Check Cashing. …

- Gas station. …

- Your employer. …

- Grocery store. …

- Endorse your check to a friend or family member

Where can I cash a check I already signed?

To receive the funds, the payee must sign, or endorse, the back of the check. This signature, called an endorsement, informs the bank or credit union that whoever signed the check is the payee and wants to accept the money.