There are individuals who find it frustrating in creating a financial plan. Some may have strived hard in accumulating the wealth but are also feel terrified to pass this wealth to their heirs because of the size of the estate and gift taxes. Favorably, there are several ruses you can make that can considerably reduce the amount you owe in taxes. Thus, one of these ruses is creating a grantor-retained annuity trust (GRAT). Thus this article is the bolt and nut to Grat trust, stocks, examples, benefits, and a brief biography of Amy grat.

GRAT Trust

Grat is an acronym for grantor retained annuity trust. It is an irrevocable financial instrument for estate planning which minimizes taxes on large financial gifts to family members. The irrevocable trust is built for a certain term or span of time. This demands that the individual establishing the trust pays a tax upon trust establishment.

I know you might be wondering why the word Annuity. As an important and large component of GRATs, They are a financial mechanism where you contribute funds or assets such as shares of stock into an account, and later that account gives a disbursement in equal installments regularly. This may be either immediately or in the future.

However, the aim of a GRAT is to change later appreciation on the assets in the GRAT to others at a minimal gift tax cost. Therefore, for a successful GRAT strategy, the assets contributed to the GRAT must generate a return at a higher rate than the IRS assumed rate of return.

The grantor holds the right to receive annuity payments for a set span of time after contributing assets to the GRAT. Typically. Thus in its easiest terms, in a grantor retained annuity trust (GRAT), the person setting up the trust is the grantor, therefore when you retain the annuities from the trust, those payments will definitely return back to you.

4 key considerations in setting up a GRAT

- The length of the trust’s term

- The assets you want to place invest in it,

- Consider the prevailing rate of return the IRS uses to calculate the trust’s annuity payments

- The beneficiary of the remainder

How GRAT Work

Apart from paying out yearly annuities which work as part of your retirement income strategy, GRATs are tools for minimizing tax liability. It is a type of gifting trust that allows individuals to transfer a high yielding property or assets to a beneficiary with a minimal estate tax.

Grantors set up an irrevocable trust, with a term ranging from 2 years and above (depending on the grantor’s wish). He contributes funds or assets into the account as a lump sum. Every year, the grantor is given out a fixed annuity. Thus, its usually a set percentage of the original amount in the trust. For instance, if you set up a GRAT with $200,000 and a fixed annuity of 12%, you would receive $12,000 yearly, despite how much is left in the trust after years.

Meanwhile, if the value of the trust sinks below the annuity payment amount, the annuity payment will be what is left of the trust assets. Thus, no further payment will be made from the trust. Lastly, at the end of the trust’s term all remaining funds in the trust, are given to the beneficiaries.

How GRATs AreTaxed

Basically, GRATs are taxed in two ways:

- Through income, you earn from the appreciation of your assets in the trust. These are subject to regular income tax

- Through the remaining funds/assets that transferred to a beneficiary. They are subject to gift taxes.

To learn more about how a grantor-retained annuity trust is taxed and its benefits to your estate plan, Read Also: Grantors Trust: A Simple definitive guide (Updated!)

Benefits of Establishing a GRAT

- The main benefit of establishing a GRAT is the potential to shift large amounts of money to a beneficiary while paying less gift tax.

- Another benefit especially for affluent individuals with large estates is utilizing a GRAT as part of their estate planning strategy. This makes it possible to transfer much more than $18,000 to a beneficiary and still don’t have to pay gift taxes.

- It allows the transfer of relevant assets in a short period of time.

- It reduces the gift and estate tax debt that such a sizable transfer would typically acquire.

Grat Stocks

Stocks are securities that represent an ownership share in a company. However, if your customers want a stock, a Grantor-Retained Annuity Trust might be right for them. This is because GRAT is an irrevocable trust that transfers wealth without paying gift or estate taxes. For example, your customer trades in stock that pays them an annuity for a set number of years, the remainder goes to their beneficiaries form of a gift.

GRAT stock can help your clients transfer the appreciation of an asset, above a small

interest rate, to a beneficiary tax-free. Here is an example you can learn from: The Famous Facebook founders Mark Zuckerberg and Dustin Moskovitz put pre-IPO stock into GRATs for children they were yet to have.

Another example is placing stocks in a GRAT just before the downturn of a market. If in the long run, it looks like they would not recover by the end of the term, then you could exchange those stocks for a equal value. Relatively, you could also start a new GRAT with the same stocks at their reduced price rate

Furthermore, you can freeze the upside on a GRAT. This occurs only if its assets have done well. Ponder on this- Assuming you were only hoping to transfer $2 million to your kids, but the stocks in the GRAT have grown past that target mid-way through the GRAT’s term. At this point you can remove the appreciated stocks and interchange them in slow-growing assets with an equal current value.

Amy Grat

Amy Grat is Chief Executive Officer of The opportunity engine, formerly International Trade Education Programs (ITEP).

Beforehand, Amy grat served as Vice President of Investor Relations for the Los Angeles County Economic Development Corporation (LAEDC). Here, she was responsible for driving revenue and cultivating the organization’s relationships with Southern California’s business community. Amy also held offices in higher education such as Associate Director of International Executive Programs at USC’s International Business Education and Research (IBEAR) Program.

This was where she designed executive education programs whose focus was on Asia and Latin America for the U.S. and international companies. She also conducted USC’s annual Asia/Pacific Business Outlook Conference. Amy grat has also served in program management roles at the University of Pennsylvania’s Office of International Programs and the International Visitors Council of Philadelphia.

Amy grat is active in industry and civic organizations, she has served on the Boards of the Wilmington Chamber of Commerce. She is also a Member of the Los Angeles Area Chamber of Commerce World Trade Week Committee and chairs the WTW Education Subcommittee. Amy is a graduate of Leadership LA (Class of 2006) and Leadership Carson (Class of 2013).

She won a prestigious Connie Award by the Containerization and Intermodal Institute in 2007. Then in 2014, She was entitled Educator of the Year by the Women’s Transportation Seminar – Los Angeles.

Finally, Amy grat holds an MBA from the University of Southern California’s Marshall School of Business. She also has an MA in International Affairs from The George Washington University and a BA in English from San Diego State University.

GRAT Example

Below are typical examples of GRAT.

Facebook founder Mark Zuckerberg put his company’s pre-IPO stock into a GRAT before it went public. While the exact numbers are not known, Forbes magazine ran estimated numbers and came up with an impressive number of about $36,216,503 as the value of Zuckerberg’s stock.

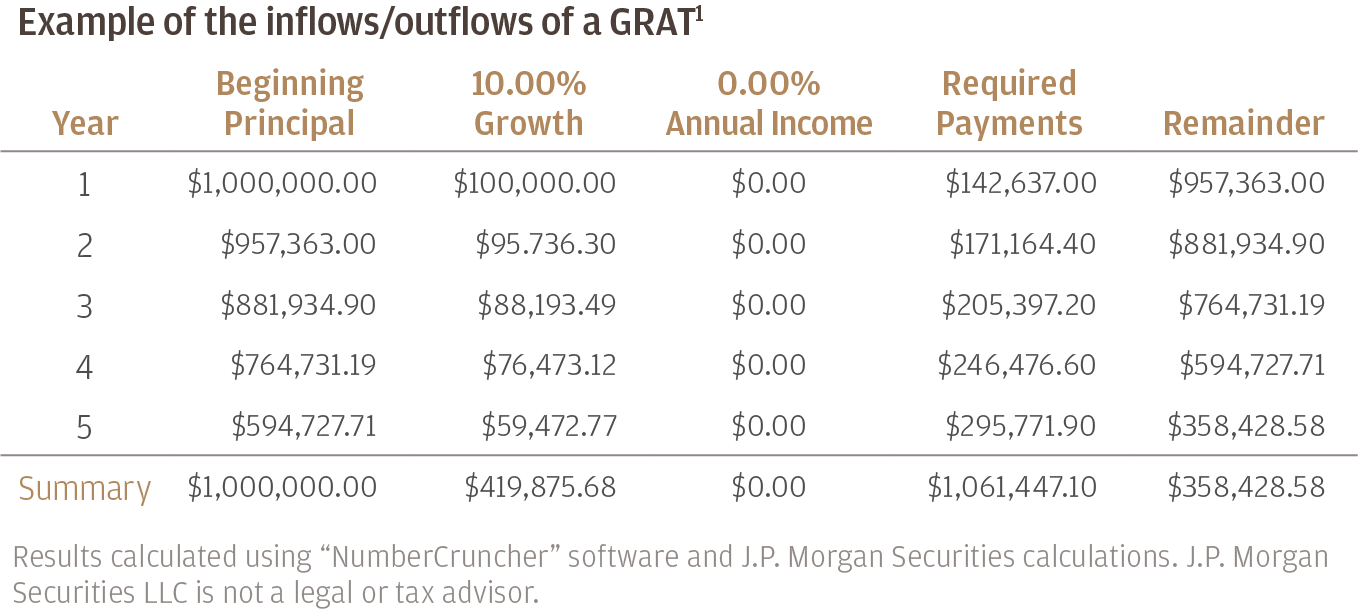

Table 1: GRAT Example

Assumptions: GRAT term: 5 years, IRS hurdle rate: 1.8%, Valuation of contributed assets: $1 Million, Principal growth: 10% annually, Annual annuity increase: 20%. (JP Morgan)

Table 2: GRAT Example

| Term | 5 Years |

| Principal | $10,000,000 |

| Annuity Interest Rate (§7520 Rate) | 0.80% |

| Rate of Return | 12.00% |

| Annual GRAT Payment | $1,512,023 |

| Total of Payments Received Over Term | $10,060,115 |

| Amount Owed in Gift Taxes | $0 |

| Remainder Passing to Beneficiaries | $995,848 |

| Estate Tax Savings at 40% | $403,139 |

In Figure 2 above, the grantor was able to bypass paying gift taxes while leaving about $1 million for their beneficiaries. Meanwhile, if the amount had moved down to their inheritors at their time of death, the gift would be subject to the current 80% federal estate tax. Thus, their beneficiaries would receive only $597,308. Therefore, by utilizing a GRAT, the grantor was able to save nearly $403,000 in taxes.

Hence, this calculator is only for illustrative purposes. Therefore, it should not be relied upon as an accurate indication of your financial retirement or investment needs. We do not guarantee that this calculator is reliable, and accurate. Please consult your tax advisor for clarification

Conclusion

GRATs are an effective strategy for passing appreciation on investments to children or beneficiaries at a minimal transfer tax cost. Although, the current economic environment, including a pessimistic stock market and relatively low-interest rates. It intensifies the ability of GRATs financed with commercial securities to exceed the IRS assumed rate of return.

Furthermore, the GRAT can prove to be an extremely viable tool to reduce the size of a taxable estate by allowing for an ample reduction of the assets for valuation views under federal gift tax laws.

Related Articles:

- LIVING TRUST: Overview, Cost, Templates, Pros & Cons (+Writing Guide)

- REVOCABLE TRUST: What is Living Revocable Trust?

- Visa Check Card Gift: Check Card vs Debit Card (+Quick Guide)

- REVOCABLE TRUST: A Comprehensive Guide (+ How it Works)

Disclaimer

This article is solely for informational purposes only. They only should not be seen as investment, tax, legal, or piece of accounting advice. Hence, we suggest that you consult your tax issues with a competent tax advisor. Have it that all investing involves risk thus past achievement is not an assurance for later returns.