When combined with other indicators, stockholder equity can be a fantastic tool to gauge a company’s financial health. In general, understanding the stockholder equity allows you to calculate your company’s net worth from your balance sheet. For example, if your stockholder equity is positive, it suggests your company will be able to pay off its creditors. Furthermore, it shows you are in good financial standing.

A negative number may suggest that your company’s assets are smaller than its liabilities. In other situations, this may imply that your company is on the verge of going bankrupt. Once you’ve determined the stockholder equity, you’ll be able to assess whether or not you need to make adjustments to improve your corporation. In this post, we will define stockholder equity, explain how to calculate it, and provide practical examples as well as recommendations for increasing it.

What is Stockholder Equity?

Stockholder’s equity is the total worth of an investor’s assets after deducting and settling liabilities. It’s also known as shareholder equity or a company’s book value. Stockholder’s equity is the difference between assets and liabilities in a business, similar to owner’s equity. Therefore, calculating stockholders’ equity is a wonderful approach to get a sense of a company’s health.

What is Included In Stockholders’ Equity?

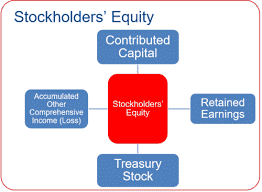

Stockholder equity is reported on the balance sheet as paid-in capital, retained earnings, accumulated other comprehensive income, treasury stock, preferred stock, as well as common stock. They are defined as follows:

- Paid-in capital: This is the capital a corporation receives from investors when it issues shares of common and preferred stock.

- Retained earnings: They are a company’s entire profits after paying out dividends to shareholders.

- Accumulated other comprehensive income: This consists of revenues, expenses, profits, and losses that are not shown in net income on an income statement.

- Treasury stock: This refers to the outstanding shares of stock that a corporation has repurchased from stockholders.

- Preferred stock: Preferred stock is stock in which dividends take precedence. In other words, shareholders will receive dividends before common stockholders.

- Common stock: These are shares that are representative of corporate ownership.

How to Determine Stockholders’ Equity

Calculating stockholders’ equity can help you gain a better understanding of your company’s financial status. Though it may forecast a future bankruptcy, knowing your stockholders’ equity will tell you whether or not you’ll need to take steps to help your business stay afloat. You calculate the stockholder equity by deducting a corporation’s liabilities from its assets. To calculate stockholder equity, use the following formula:

Total assets – Total liabilities = Stockholder’s equity.

Alternatively, you can calculate stockholder equity by adding share capital and retained earnings and subtracting treasury stock. The equation for this would be:

Share capital + Retained earnings – Treasury stock = Total shareholder equity

Though determining stockholder’s equity isn’t an all-encompassing look into your company’s financial soundness, it can provide a rough indicator of its current and future position.

Examples of Stockholder Equity

Here are a few examples of stockholder equity in action:

Example 1

Your bank had $3 million in assets as of December 2018. It also has total liabilities of $2 million. This suggests that the bank’s entire stockholder’s equity was $1 million at the time. This is because: $3 million (assets) – $2 million (liabilities) = $1 million (stockholder’s equity). This is the amount of money that stockholders will have when your bank has paid off all of its liabilities. This stockholder’s equity will be on the balance sheet by indicating each component that makes up the stockholder equity, such as common stock, preferred stock, retained earnings, accumulated other comprehensive income, and more.

Example 2

If your child’s lemonade stand has $50 in assets but only $20 in liabilities for the week, the stockholder’s equity would be $30. This is due to the fact that $50 (assets) – $20 (liabilities) = $30 (stockholder’s equity). This positive figure could indicate that the lemonade stand is doing well financially.

Example 3

Your small business has a total asset value of $10,000 by November 2019. Your company also has $7,000 in total liabilities. This means that by November 2019, your company’s entire stockholder’s equity was $3,000. In other terms, $10,000 (assets) minus $7,000 (liabilities) equals $3,000 (stockholder’s equity). The $3,000 is what stockholders have after your small firm has paid off all of its liabilities.

What does an increase or drop indicate?

If you calculate stockholders’ equity regularly, you’ve probably observed growth or reduction. Here are some of the possible explanations for both:

Increasing stockholder equity

There are various reasons why stockholders’ equity may increase over time, including:

- Profit

- Inventory liquidation (s)

- Changes in the process of assets valuation

- Increased earnings kept

- Shareholders provide more capital

Decrease in Stockholders’ Equity.

Here are some of the possible causes of a reduction in stockholder equity:

- Depreciation of assets

- More liabilities

- Repurchase of outstanding shares

- More treasury shares

- Expenses rise

- Reduced retained earnings

- Dividends paid to shareholders

How to Increase Stockholder Equity

If your company is in poor financial health and has a negative stockholder’s equity, you may want to explore applying several strategies to raise stockholder’s equity. Here are some ideas for increasing your company’s net value, or stockholder equity:

#1. Reduce liabilities

By reducing the number of liabilities, you enhance the amount of overall stockholder equity. Consider reducing your financial commitments or your business expenses to reduce liabilities.

#2. Increase your retained earnings.

If your company becomes more profitable, you will observe a rise in retained earnings. Consider laying off personnel, eliminating any benefits or bonuses in place, and adopting more cost-effective equipment and machinery to enhance retained earnings. If you improve your company’s sales revenue, you will see an increase in your retained earnings.

#3. Sell depreciated assets

Another strategy to boost stockholder equity is to identify any assets your company possesses that has depreciated over time. These assets can also be liquidated (converted into cash) to make a profit.

#4. Increase your paid-in capital.

If a shareholder makes a monetary or other donation to a firm, the value of their investment in the business, as well as the value of each outstanding share, will increase. This will reflect on the balance sheet as an increase in stockholder equity.

It’s crucial to remember that while measuring stockholder’s equity can be useful, it must be used in conjunction with other tools to provide you with an accurate picture of your company’s net value.

The Role of Retained Earnings in Increasing Stockholders’ Equity

Retained earnings (RE) are a company’s net income from operations as well as other business activities that it keeps as additional equity capital. Retained earnings are thus a component of stockholders’ equity. They reflect returns on total stockholder equity reinvested back into the company.

Furthermore, retained earnings build and grow in size over time. Moreover, accumulated retained earnings may exceed the amount of donated equity capital and eventually develop to be the primary source of stockholder equity at times.

Companies may return a portion of stockholders’ equity to stockholders if they are unable to allocate equity capital in ways that yield the required profitability. Share buybacks are the reverse capital exchange between a corporation and its stockholders. When the firm acquires back its shares, it becomes treasury shares, and their dollar value is recorded in the treasury stock contra account.

Treasury shares continue to be counted as issued shares, but they are not considered outstanding and hence are not included in dividends or earnings per share calculations (EPS). When a company needs to acquire extra capital, treasury shares can always be reissued to stockholders for purchase. If a firm does not want to keep the shares for future financing, it can choose to retire them.

Applications in Personal Investing

With diverse debt as well as equity products in mind, we can apply this information to our personal investment decisions. Although many investment decisions are influenced by the level of risk we are willing to take, we cannot overlook all of the crucial components discussed above. Bonds are contractual liabilities in which annual payments are guaranteed unless the issuer defaults, but dividend payments from owning shares are discretionary and not fixed.

Bondholders come before preferred shareholders, who come before regular shareholders in terms of payment and liquidation sequence. As a result, from an investor’s standpoint, debt is the least risky investment, and for businesses, it is the cheapest method of funding because interest payments are tax-deductible, and debt generally provides a lesser return to investors.

However, debt is the riskiest form of funding for businesses since the corporation must fulfill the commitment with bondholders to make monthly interest payments regardless of economic conditions.

Stockholders’ Equity FAQs

How Do You Calculate Equity?

Stockholders’ equity is calculated by subtracting a company’s total assets from its total liabilities. All of these numbers can be found on a company’s balance sheet.

Is Stockholders’ Equity Equal to Cash on Hand?

No, because equity accounts for total assets and total liabilities, cash and cash equivalents are only a small part of a company’s financial picture.

What will increase stockholders equity?

There are essentially two ways for stockholders’ equity to grow. One is for existing or new shareholders to put more money into the firm, increasing stockholders’ interest in a business, and the other is for the company to make and keep a profit.

Is Stockholders’ Equity Equal to Cash on Hand?

No equity is not same as cash on hand.

- Equity Capital Market (ECM): Detailed Guide with Example

- What Are SHORT-TERM INVESTMENTS: Definition, Examples, and Banks

- Stakeholder Mapping: Guide to the Mapping Tool for Effective Stakeholder Management

- Cash Ratio: Formula, Calculations & Examples

- Balance Sheet vs. Profit and Loss Statement: Relationships & Differences