A lot of things have changed in recent times. However, there are also a few changes in how to report the sale of inherited property and how to report the sale of the inherited property on a tax return that you should know about, especially the rules around it in your state. Get to understand them in detail below

How to Report the Sale of Inherited Property

Firstly, we need to understand what inheritance means before diving into the main concern of how to report the sale of inherited property. Inheritance simply means assets that an individual bequeaths to a loved one after they pass away. An inheritance may be in the form of cash, investments such as stocks or bonds, or other assets such as jewelry, automobiles, art, antiques, real estate, and other tangible assets. However, those who receive an inheritance may, in one way or another, be subject to inheritance taxes. In a case where a beneficiary is more distantly related to the decedent, the inheritance tax is likely to be higher.

A decedent’s assets are shared according to their will through the probate process. In a situation where there is no will, the court will appoint an administrator to divide assets according to the laws of the state. There are currently six states that have inheritance taxes, and they include Iowa, Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania. In most of these states, any assets that are bequeathed to a spouse are exempt from inheritance taxes. In some cases, children are also exempt, or rather, they may face lower rates of taxation.

The rates of an inheritance tax (“death duty” or “the last twist of the taxman’s knife”) depend on some factors, including a beneficiary’s state of residence, the value of the inheritance, and the beneficiary’s relationship to the decedent. Consequently, beneficiaries with no family ties to the decedent are subject to higher inheritance taxes than beneficiaries who are closely related to the decedent.

Understanding How to Report the Sale of Inherited Property

Now, moving on to how to report the sale of inherited property. Note that the basis of property inherited is generally the fair market value (FMV) of the property on the date of the decedent’s death. Furthermore, there are situations where that may not be the case:

- The personal representative for the estate chooses to use an alternate valuation.

- Value under the special-use valuation method for real property in farming or a close business.

- The decedent’s basis in land to the extent of the value not in existence from the decedent’s taxable estate qualifies for a conservation easement.

- Property that the taxpayer or spouse originally gave to the decedent within one year before the decedent’s death.

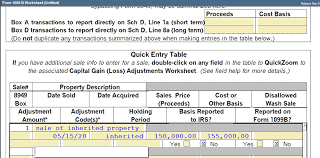

How to report a sale of inherited property is mostly the same, although there are a lot of programs offering these services online. The steps you will take on how to report a sale of inherited property will look like these:

- Income

- Capital Gain/Loss (Sch D)

- New

- Description of Property: Enter a description of the property being sold.

- Form 1099-B Type: Select “Form 1099-B Not Received”.

- Date Acquired: Select “Inherited-Long-Term” from the drop-down menu.

- Date Sold—Enter the date the property was sold.

- Sales Price: Enter the sales price.

- Cost-Enter the fair market value

How to Report the Sale of Inherited Property on a Tax Return

There is a difference between a “beneficiary” and an “heir”. Intestates refer to individuals in a will, while heirs refer to people, such as a child or a surviving spouse, who are to receive a decedent’s property, by “intestate succession,” which is a set of rules to sort out inheritance matters, in the absence of a will. As you navigate the process of reporting the sale of inherited property, be sure to consult this guide on inheriting a home from your parents for helpful insights and guidance.

To determine if the sale of inherited property is taxable, you must first determine the taxpayer’s basis in the property.

Reporting the sale of the inherited property on a tax return is not difficult. Currently, President Biden is proposing the removal of something called the step-up in basis for inherited property. However, the importance of the step-up in the basis is essential. If you file out tax forms for the sale of inherited property, the step-up in basis is a key component, although, for tax filing purposes, it is the fair market value.

Understanding How to Report the Sale of Inherited Property on Tax Return

Your share of the sales proceeds (generally reported on the report on Form 1099-S) from the sale of a property you had inherited should be reported on Schedule D in the Investment Income section of TaxAct. You would enter “Inherited” as the date the property was purchased, then enter the cost basis, date of sale, and the sales proceeds.

However, I want you to know some ways to avoid paying taxes on your property. They include: selling it immediately after inheritance, making it your primary home, and selling it after two years. Inheriting property can trigger a capital gains tax if you choose to sell it. And there are other taxes you need to consider, such as state inheritance taxes. If the inherited property is a residence consider living in it for a few years before selling it.

Alternatively, consider renting it. Talking to an estate planning attorney or a tax professional may be helpful if you stand to inherit assets from your parents or anyone else.

Capital Gains Tax Rules for Inherited Property

When inheriting a property, such as a home or other real estate, the capital gains tax kicks in if you sell that asset at a higher price point than the person you inherited it from paid for it. Likewise, it’s possible to claim a capital loss deduction if you end up selling the property at a loss. It’s important you note this too while knowing how to report inherited property on a tax return.

The difference with inherited property, however, is that the IRS allows you to use what we call a step-up basis for calculating capital gains tax liability. The step-up cost basis represents the value of the home when you inherit it versus its original purchase price.

To determine if the sale of inherited property is taxable, you must first determine your basis in the property. The basis of property inherited from a decedent is generally one of the following:

- The fair market value (FMV) of the property on the date of the decedent’s death (whether or not the executor of the estate files an estate tax return (Form 706, United States Estate (and Generation-Skipping Transfer) Tax Return)).

- The FMV of the property on the alternate valuation date is only if the executor of the estate files an estate tax return (Form 706) and elects to use the alternate valuation on that return.

Understanding Capital Gains

Now regarding capital gains on an inherited property (and losses), you can claim a capital loss on inherited property if you sell it and all of these are true:

- You sell the house in an arm’s length transaction.

- Selling the house to an unrelated person.

- You and your siblings didn’t use the property for personal purposes.

- When you and your siblings didn’t intend to convert the property to personal use before the sale.

An arm’s length transaction is a transaction where the buyers and sellers have no relationship with each other. Except when handling an inheritance. When a property is received on inheritance or as a gift, it is not taxable for the receiver. When the inheritor or the receiver of this gift of property sells it, capital gains on the sale are taxable for the inheritor.

The Procedure to Calculate the Capital Gains of Inherited Property

The steps you need to take in order to achieve this goal are given below:

- You must know the cost of acquisition and indexation in order to calculate the capital gains.

- Cost of the property: The property did not cost anything to the inheritor, but for the calculation of capital gain, the cost to the previous owner is considered as the cost of acquisition of the property.

- Indexation of cost – The year of acquisition of the previous owner is considered for the purpose of indexation of the cost of acquisition along with the year of sale of the property.

- The base year for such calculations has been updated from 1981 to 2001.

Calculate the cost of capital gains using the formula: Cost of acquisition x ( Cost inflation index of the year of sale/Cost inflation index of the year of acquisition). So where the Cost Inflation Index (CII) varies every financial year, a few are tabulated below:

| Year | CII | Year | CII |

| 2001-02 | 100 | 2011-12 | 184 |

| 2002-03 | 105 | 2012-13 | 200 |

| 2003-04 | 109 | 2013-14 | 220 |

| 2004-05 | 113 | 2014-15 | 240 |

| 2005-06 | 117 | 2015-16 | 254 |

| 2006-07 | 122 | 2016-17 | 264 |

| 2007-08 | 129 | 2017-18 | 272 |

| 2008-09 | 137 | 2018-19 | 280 |

| 2009-10 | 148 | 2019-20 | 289 |

| 2010-11 | 167 | 2020-21 | 301 |

Finally, subtract the cost of capital gain from the selling price of the property to know the net gain of the transaction.

Conclusion

How to report the sale of the inherited property on a tax return is basically simple when you know the necessary details and your way around them. In every way, whether you have inherited property or not, it’s important you know beforehand the pros and cons of inherited property, as well as how to report the property even on a tax return.

FAQs

How do you report the sell of an inherited property?

Report this sale on Schedule D and Form 8949. The gain or loss of inherited property is reported in the year that it is sold.

How do i account for the sale of an inheirted property to the IRS?

State a description of the inherited property on Line 8, column (a) of Schedule D; 2. Record the date of death in column (b) of Line 8. ; 3. Place the date and follow the following instructions.

Where should i enter capital gains and loss of an inheirted property?

Report the sale on Form 8949, which will transfer to Schedule D. Enter your basis in the property as your share of the fair market value

Where do i report the sale of gifts and inheirtances?

Report the sale on Schedule D (Form 1040), Capital Gains and Losses and on Form 8949, Sales and Other Dispositions of Capital Assets. If you sell the property for more than your basis, you have a taxable gain

Related Articles

- INHERITANCE TAX: Overview & Threshold Explained

- Primary Residence: Tips to Avoid Taxes on The Sale of Primary Residence

- Home in Trust: Placing Your Home in Trust

- FINANCIAL REPORTING: All you need to know with Examples (+ quick easy tools)

- 1031 EXCHANGE FLORIDA: Tax Exchange Rules, Timeline, and Processes (Updated!)