Do you want to know if you can afford a mortgage? Or are you already looking for the ideal house? In any case, knowing the average monthly mortgage payment will help you put your own house purchase into perspective.

What is the average monthly mortgage payment in the United States? Let’s break it down and see how much your beloved home actually costs.

What is the Average Mortgage Payment?

According to the U.S. Census Bureau, the median monthly mortgage payment is slightly more than $1,600. Census Bureau. Of course, this varies depending on the size of the house and where you reside, but it’s a good starting point.

If you’re the type of person who doesn’t care how we came up with the figure of $1,600, you may skip ahead to the next part.

What Does the Average Mortgage Payment Indicate?

The United States Census Bureau publishes both the mean and median payment. The mean and average are the same thing. The median is the value in the middle of a group of numbers. It splits the lower and upper halves of the set’s values.

Finding the median value rather than the average value can be more informative when calculating a typical monthly mortgage payment. Extremely high or low values might affect averages. The median indicates where the middle is for a wide variety of homeowners.

National averages:

Looking at national statistics, the 2020 National Association of REALTORS Profile of Home Buyers and Sellers indicates a national median home price of $272,500. With a down payment of 10% of the purchase price, we may compute a loan size of $245,250. Using current mortgage loan rates, you can calculate the average monthly mortgage payments as follows:

- $1,700 per month on a 30-year fixed-rate loan with a 3.29 percent interest rate

- A 15-year fixed-rate credit at 2.79 percent costs $2,296 each month.

First-time homebuyers:

The national averages include all homeowners, including those who have accumulated equity, advanced in their careers, and established good credit ratings. Those people are more likely to apply for and be authorized for higher loans.

Because first-time homebuyers sometimes have fewer funds and purchase less expensive homes, let’s estimate a purchase price of $200,000. According to the National Association of REALTORS, first-time buyers typically put down 7%. Based on this information, the average payments would be:

- $1,307 per month on a 30-year fixed-rate loan with a 3.29 percent interest rate.

- A 15-year fixed-rate credit at 2.79 percent costs $1,760 each month.

However, putting down less than 20% means you’ll likely have to pay mortgage insurance and pay extra interest (among other things). Now, suppose a first-time homebuyer purchases that less-expensive home and make a 20% down payment. That bigger down payment significantly reduces monthly mortgage payments. The figures might change if a 20% down payment was used:

- $1,077 per month on a 30-year fixed-rate loan with a 3.29 percent interest rate

- A 15-year fixed-rate credit at 2.79 percent costs $1,466 each month.

Housing markets:

The figures above are based on national median statistics. The peculiarities of the market in which you buy will determine your monthly mortgage payment. Homes on the coast and in cities are often more expensive. Houses are less expensive in the middle of America. Compared to the national average mortgage payment may not be beneficial.

According to Zillow, the median home price in San Diego is $808,608, which is significantly higher than the national median. Even with a 20% down payment, the monthly payment on a 30-year loan at 3.29 percent would be $4,018.

Meanwhile, the median home price in Omaha, Nebraska, is $234,639.6. With a 20% down payment, Omaha residents pay only $1,245 on a 30-year loan.

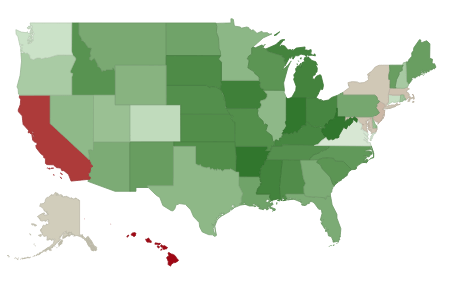

Average Mortgage Payments by State

Another important thing to consider when comparing average and median mortgage payments is location because housing prices and mortgage interest rates vary greatly between states.

We’ll examine median monthly house payments as well as average individual mortgage debt balances across all 50 states in the graphic below.

| State | Median Monthly Payment | Average Mortgage Balance |

| Alabama | $1,147 | $144,272 |

| Alaska | $1,907 | $227,960 |

| Arizona | $1,394 | $210,872 |

| Arkansas | $1,071 | $132,973 |

| California | $2,282 | $371,981 |

| Colorado | $1,681 | $273,718 |

| Connecticut | $2,096 | $224,336 |

| Delaware | $1,563 | $190,846 |

| Florida | $1,466 | $195,549 |

| Georgia | $1,383 | $180,378 |

| Hawaii | $2,350 | $348,637 |

| Idaho | $1,228 | $185,322 |

| Illinois | $1,668 | $177,055 |

| Indiana | $1,130 | $124,454 |

| Iowa | $1,234 | $135,111 |

| Kansas | $1,349 | $141,610 |

| Kentucky | $1,158 | $129,469 |

| Louisiana | $1,267 | $154,713 |

| Maine | $1,381 | $140,904 |

| Maryland | $1,987 | $253,598 |

| Massachusetts | $2,165 | $261,345 |

| Michigan | $1,279 | $135,845 |

| Minnesota | $1,547 | $180,766 |

| Mississippi | $1,134 | $123,062 |

| Missouri | $1,254 | $143,545 |

| Montana | $1,386 | $189,021 |

| Nebraska | $1,352 | $144,299 |

| Nevada | $1,469 | $239,477 |

| New Hampshire | $1,917 | $184,468 |

| New Jersey | $2,439 | $241,772 |

| New Mexico | $1,262 | $163,384 |

| New York | $2,114 | $240,795 |

| North Carolina | $1,290 | $165,636 |

| North Dakota | $1,389 | $167,883 |

| Ohio | $1,269 | $125,250 |

| Oklahoma | $1,214 | $138,752 |

| Oregon | $1,647 | $236,604 |

| Pennsylvania | $1,474 | $147,148 |

| Rhode Island | $1,838 | $189,946 |

| South Carolina | $1,227 | $165,649 |

| South Dakota | $1,298 | $158,728 |

| Tennessee | $1,224 | $165,260 |

| Texas | $1,549 | $186,696 |

| Utah | $1,497 | $230,545 |

| Vermont | $1,594 | $151,884 |

| Virginia | $1,767 | $245,054 |

| Washington | $1,826 | $278,851 |

| West Virginia | $1,023 | $112,912 |

| Wisconsin | $1,418 | $143,979 |

| Wyoming | $1,428 | $191,545 |

Average Mortgage Payment By City

A monthly property payment might be substantially more than the national average or median payment, especially in coastal cities where space is limited. According to US Census Bureau data from the 2019 American Community Survey, the median monthly house payment (including utilities, insurance, and HOA fees) in Los Angeles was more than $2,600 per month and more than $2,800 per month in the New York City region.

However, not all metro regions are as expensive; in Phoenix, Arizona, the median property payment is around $1,500 per month, while in Dallas, it is over $1,800 per month. According to Census Bureau data, here’s how the most populous metro regions measure up in terms of monthly living expenditures. The cities are organized by size.

| City | Median monthly home payment |

| Los Angeles, California | $2,659 |

| Chicago, Illinois | $1,882 |

| Houston, Texas | $1,815 |

| Phoenix, Arizona | $1,540 |

| Miami, Florida | $1,874 |

| New York City, New York | $2,807 |

| Dallas, TX | $1,870 |

| Riverside County, California | $1,969 |

Average Monthly Mortgage Payment According To Loan Size

Based on the National Association of Realtors‘ April 2022 median regional existing-home prices, borrowers with 20% down and a 30-year mortgage with a 5.46 percent fixed rate can expect to pay the following in principle and interest each month.

| YEAR | MEDIAN MONTHLY MORTGAGE PAYMENT | MEDIAN HOME SALE PRICE* |

| *New-home sales only sources: U.S. Census Bureau and U.S. Department of Housing and Urban Development | ||

| 2019 | $1,200 | $320,250 |

| 2017 | $1,100 | $322,425 |

| 2015 | $1,030 | $294,150 |

| 2013 | $997 | $266,225 |

| 2011 | $1,019 | $224,900 |

Average Mortgage Payment Costs

New homeowners may be unaware of all of the costs associated with their mortgage payments. Monthly payments include the following:

- Principal: The principal is the amount of money borrowed when you take out your first mortgage. This is computed by deducting your down payment from the selling price of the home.

- Interest: This is the second-largest component of your monthly mortgage payment and is the money you pay your mortgage lender in exchange for them granting you the loan. An annual percentage rate is commonly used to calculate interest rates (APR).

- Property taxes: The property taxes you pay go to your local government to fund road repairs, public schools, fire departments, and other services. Property taxes, which can be one of the most expensive components of mortgage payments, may surprise new homeowners.

- Homeowners insurance: Although it is not legally needed to have homeowners insurance, most mortgage lenders will not make a loan unless you have it. This includes damage from home fires, break-ins, and other incidents.

- Homeowners Association (HOA): If you live in an HOA neighborhood, you will be subject to certain rules, regulations, and fees. Townhouses, multi-unit apartment buildings, and condominiums are the most typical examples. The fees you pay for belonging to an HOA may help with trash pickup, landscaping, security, and maintenance, as well as access to on-site services.

How We Arrived at Our Average Mortgage Payment Figure

We utilized the average house sales price from the Census Bureau and the Department of Housing and Urban Development to establish how much the average borrower pays for their mortgage each month. The average price in the first quarter of 2022 was $507,800. We then used the typical down payment of 13% (as published by the National Association of Realtors) to calculate an average loan amount. Data from Freddie Mac was also utilized to calculate the average mortgage rates for 30-year and 15-year fixed-rate mortgages in the first quarter of 2022: 3.82 percent and 3.04 percent, respectively.

Can I Obtain a Mortgage for Three Times My Current Income?

An income multiple of three is often at the lower end of the scale, therefore, many lenders are ready to grant more to a suitable applicant. It is possible to obtain a mortgage for three times your pay.

Are Interest-Only Loans More Affordable?

You only pay the loan’s interest when you have an interest-only mortgage. You will still owe the full amount borrowed at the conclusion of the repayment period. The biggest benefit of making interest-only mortgage payments is that your monthly payments will be significantly less expensive.

Can I Live in a Home with an Interest-Only Mortgage?

Although interest-only mortgages are still a popular choice among buy-to-let investors, they are also available for homes. Despite this, not many lenders provide them because the homeowner has minimal security.

What Will Happen if I Am Unable to Pay Off My Mortgage at the End of the Term?

Your home can be taken back if you don’t pay the remaining sum by the conclusion of the mortgage term, and your credit report might also suffer.

Is a Tiny Mortgage Preferable than None at All?

Going part-time or downsizing your job are just a few ways that being mortgage-free might make it easier to downsize. It also typically makes buying and selling a property less expensive and simpler. A lesser mortgage typically affords you more freedom and security.

Conclusion

The monthly expense of a mortgage goes much beyond principal repayment. The loan interest, property taxes, homeowners’ insurance, and mortgage insurance are all included and vary depending on where you live. These criteria must be considered when evaluating how much housing you can afford.

Related Articles

- MORTGAGE FRAUD: Types, Signs, and How To Avoid It

- GIFT LETTER FOR MORTGAGE: How To Write One

- PAY OFF MORTGAGE EARLY: When & How To Pay Off Mortgage Early

- ADJUSTABLE-RATE MORTGAGE (ARM) Loan: Definition and 2022 Rates

- What Is Mortgage Insurance and When Do You Need It?

(xanax)