Almost everything you do in your business has a cost. You pay a price, whether it’s in terms of time, money, effort, or anything else. But what happens when you establish a production limit and then have to create more than you planned? You come across what is called marginal cost. Let’s learn about the marginal cost, the formula, and how to calculate it with examples.

What Is Marginal Cost?

The marginal cost is a depiction of the costs incurred as more units of a product is manufactured. When producing physical goods (such as a steel nail), the key cost considerations are:

- Workforce (the workers who make the nails).

- Physical items (the raw materials that are turned into nails, plus the machinery required).

- Property investment (expenses involving the factory where the nails are made).

- Modes of transportation (costs incurred for transporting both raw goods and finished products).

Some of these costs remain constant regardless of how many nails are manufactured. The cost of physical space, for example, is unlikely to vary whether the facility produces one nail or one million nails. Manufacturing equipment, once acquired, becomes a fixed cost, despite long-term wear and tear and the additional power required to keep the machines operating.

Other cost elements will vary depending on how many units of a product are manufactured. If you want to create additional nails, you’ll need more raw iron. And they will need to be transported to the plant. The finished nails must also be transported to hardware retailers. If additional worker hours are necessary to manufacture the extra nails, labor costs may rise as well.

How to Calculate Marginal Cost using the Formula?

Businesses, economists, and market analysts use the following formula to determine marginal cost:

Marginal Cost = (Change in Costs) / (Change in Quantity)

This yields a monetary value for each extra unit of a product produced.

The cost adjustment will be heavily influenced by the existing size of production. As an example:

- Because they may continue to use the same oven in the same room, a baker operating out of their kitchen may be able to manufacture anything from one to fifty baguettes without incurring substantial costs. (Their biggest cost increase in moving from a single loaf to a 50-loaf production run would be the additional flour, salt, water, and yeast—all of which are quite inexpensive basic ingredients.)

- However, if the baker intends to produce hundreds of baguettes, they will most likely need to start in a much bigger area than their home kitchen. In this example, boosting production will result in a considerably higher fixed cost since they would most likely have to lease space in a bigger facility and maybe acquire additional equipment.

- Increased production costs may not always imply lower total income. On the contrary, most firms reduce their per-unit cost of production by raising their output level. This is related to the “economies of scale” idea. The average cost per unit produced tends to decrease as the volume of production increases—provided, of course, that there is a sufficient market for people eager to acquire your product.

How to use the Marginal Cost Formula

Economists, especially those studying microeconomics, utilize the marginal cost formula to calculate the costs of physical production.

The marginal cost formula is also often used by firms that want to forecast the extra cost. Also, the marginal cost formula can forecast the increased profit that may result from growing their production scale. Production choices are made by business executives depending on whether an increase in overall production cost will increase total profit. Business leaders may use the marginal cost formula to make educated choices about their company’s future by keeping careful tabs on the cost of labor, real estate, raw materials, and transportation.

An Example of the Marginal Cost Formula

Johnson Tires, a publicly traded firm, routinely produces 10,000 truck tires every year for $5 million. However, after one year, the market demand for tires has increased dramatically, necessitating extra unit production. Thus, prompting management to acquire more raw materials and replacement parts, as well as engage more labor.

Because of this demand, the total production costs for 15,000 units in that year are $7.5 million. You conclude as a financial analyst that the marginal cost for each extra unit produced is $500 ($2,500,000 / 5,000).

The Importance of Marginal Cost

In economics, marginal costs are essential because they help firms maximize earnings. When marginal costs match marginal income, we have profit maximization. This is the case when the cost of producing an extra product is precisely equal to the revenue generated by selling it. In other words, the firm is no longer profitable at that moment.

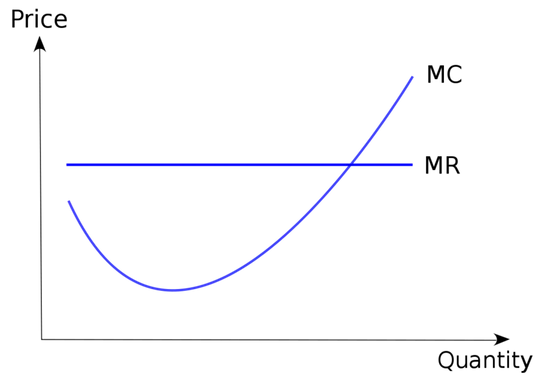

As the marginal cost curve below shows, marginal costs begin to fall as the organization benefits from economies of scale. However, when businesses grow less productive and suffer from diseconomies of scale, marginal costs might begin to rise. This is the moment at which costs begin to rise and finally meet marginal income.

This might be due to the business growing too large and inefficient. It could also be a management problem in which employees become demotivated and less productive. Whatever the cause, enterprises may confront escalating costs and be forced to halt production when their income equals their marginal cost.

Marginal Cost Curve

The MC is an important factor in the manufacturing industry since it determines whether to discontinue further production. At a certain level of production, MR Equals MC, and hence the enterprise is no longer profitable. Increasing production anymore would therefore be counter-productive.

What Is the Distinction Between Marginal Product and Marginal Cost?

The marginal product of a business is the extra output produced as a consequence of increased input made into the organization. In practice, this may represent the extra doughnuts manufactured by a donut shop after hiring an extra employee or the increased quantity of strawberries gathered by a farmer after planting more seeds.

What Is the Marginal Cost of Production?

The marginal cost of production in economics is the change in total production cost that results from creating or producing one extra unit. Divide the change in production costs by the change in quantity to determine marginal cost. The goal of marginal cost analysis is to discover when an organization may reach economies of scale to improve productivity and overall operations. If the MC of manufacturing one more unit is less than the per-unit price, the manufacturer may be able to profit.

Understanding Marginal Cost of Production

The marginal cost of production is a concept in economics and management accounting that is often utilized by businesses to determine an ideal production level. Manufacturers often consider how much it would cost to add one additional unit to their production schedules.

At a given level of production, the advantage of creating one more unit and receiving money from that item reduces the entire cost of producing the product line. The key to reducing production costs is to locate that point or level as soon as feasible.

All costs that fluctuate with the degree of production are included in the MC of production. For example, if a corporation wants to construct a whole new facility to manufacture more items, the cost of construction is marginal. The MC changes with the quantity of the item produced.

Marginal cost is an essential concept in economic theory because a corporation seeking to maximize profits would produce until the marginal cost (MC) equals marginal revenue (MR) (MR). After then, the cost of creating an additional item will outweigh the money produced.

Information asymmetries, positive and negative externalities, transaction costs, and pricing discrimination are all economic characteristics that might affect the marginal cost of production.

Examples of Marginal Cost of Production

The marginal cost of production includes the following costs:

#1. Variable costs

Variable costs change with the amount of production, and they climb progressively with the number of units produced. A shoemaker, for example, needs sixty cents for leather and plastic for each shoe created. Leather and plastic are variable costs, meaning that their costs rise as the number of shoes produced rises.

#2. Fixed costs

Fixed costs stay fixed and do not fluctuate whether production output decreases or increases. The rent paid for the shoe manufacturer site is one example. The costs are dispersed across all production units and will reduce on a per-unit basis as output levels grow.

#3. Production’s short-run marginal cost

When more production is created exclusively on a short-term basis, the short-run marginal cost is incurred. During short-run production, the corporation may hold a fixed number of assets and, as a result, may opt to reduce or raise production levels based on the available number of assets.

#4. Production’s long-run marginal cost

When every input is variable, the long-run marginal cost of production is the increasing cost incurred throughout production. It is the increased cost incurred when a firm expands its operations by hiring more people, expanding a plant, or entering a new market.

The Importance of Marginal Cost of Production

It is simpler for a corporation to set production levels and implement per unit pricing strategies after knowing the link between the marginal cost of production and the marginal revenue. Knowing the marginal cost allows the firm to calculate and develop an ideal revenue margin for maintaining sales and boosting profits.

The marginal cost of production is used to calculate the change in a product’s cost caused by the production of an additional unit of output. When the firm has reached its optimal level of production, creating more units will raise the cost of production per unit. Overproduction above a certain level, for example, may need extra compensation for employees as well as additional equipment maintenance costs.

Increased production capacity will be costly if the marginal cost per unit is high. A low marginal cost of production, on the other hand, may indicate that a corporation may obtain economies of scale by working with reduced fixed costs in specific production lines.

Which is the Formula for Calculating the Marginal Cost of Production?

The marginal cost of production is computed by dividing the cost change by the quantity change. Assume a plant is presently producing 5,000 units and desires to raise production to 10,000 units. If the factory’s present cost of production is $100,000 and expanding production will boost costs to $150,000, the marginal cost of production is $10, or ($150,000 – $100,000) / (10,000 – 5,000).

What role does the Marginal Cost of Production have in the Success of Businesses?

The marginal cost of production might assist firms in optimizing their production levels. Creating too much too rapidly may have a detrimental influence on profitability, while producing too little may result in unsatisfactory outcomes. In general, a corporation will attain optimum production levels when its marginal cost of production equals its marginal income.

Which Jobs Make Use of the Marginal Cost Formula?

As part of normal financial analysis, professionals in a variety of corporate finance responsibilities assess the additional cost of production. Accountants in the valuations division may calculate the marginal cost for a customer, while analysts in investment banking may incorporate it as part of their financial model output.

Economies of Scale (or Not)

Businesses that have economies of scale may have cheaper costs of manufacturing more items. Producing each extra unit becomes cheaper for a business with economies of scale, and the company is encouraged to achieve the point where marginal revenue equals marginal cost.

A production plant, for example, with a large amount of space capacity gets more efficient as more volume is produced. Furthermore, the business can negotiate cheaper material costs with suppliers in bigger quantities, lowering variable costs over time.

For certain firms, when more products or services are produced, per unit costs climb. Diseconomies of scale are thought to exist in these firms. Consider a corporation that has achieved its maximum production volume. If it wanted to manufacture additional units, the marginal cost would be quite high since substantial expenditures would be necessary to increase the factory’s capacity or lease space at a high cost from another firm.

Marginal Cost Pricing

Marginal cost pricing is when the selling corporation cuts the price of its items to match the marginal cost. In other words, it cuts the price to the point where it no longer earns a profit. Typically, a company would do this if they are experiencing low demand and need to decrease prices to the marginal cost to get consumers back.

Alternatively, the business may be financially-strapped and has to sell its items rapidly to earn some cash. It might be to cover an anticipated debt payment, or it could simply be due to a lack of funds. At the same time, it may use a marginal cost pricing approach to minimize stock, which is very popular in the fashion industry.

Such a tactic is often used by supermarkets. This might be done to get rid of out-of-date inventory or to entice buyers to buy inexpensive items. The idea is that while customers are at the shop, they will also buy other things that will benefit the company.

Obtaining Optimal Production

The firm eventually achieves its optimal production level, at which time creating any more units would raise the per-unit production cost. In other words, increased production raises both fixed and variable costs. Increased production over a given level, for example, may necessitate paying employees exorbitant sums of overtime compensation. Alternatively, the costs of mechanical maintenance may skyrocket.

The marginal cost of production is the difference in the overall cost of an item that results from producing one more unit of that thing. The marginal cost (MC) is determined by dividing the change in total cost (C) by the change in quantity (Q). So, the marginal cost is computed using calculus by calculating the first derivative of the total cost function concerning the quantity:

MC = ΔQ/ΔC

Marginal Cost Formula

MC=Marginal cost

Δ=Dividing the change

C=Total cost

Q=Change in quantity

As production capacity varies, so may the marginal costs of production. If, for example, expanding production from 200 to 201 units per day necessitates the acquisition of extra equipment by a small business, the marginal cost of production may be quite high. This expenditure, on the other hand, might be much cheaper if the business considers increasing from 150 to 151 units utilizing current equipment.

A lower marginal cost of production indicates that the business has lower fixed costs for a given production volume. If the marginal cost of production is high, the cost of expanding production volume will be high as well, therefore increasing production may not be in the best interests of the business.

Marginal Revenue Calculation

The difference in revenue caused by the sale of one more unit of a product is measured as marginal revenue. Assume a corporation sells widgets for $10 per unit, sells 10 widgets each month on average, and makes $100 throughout that period. Widgets have grown in popularity, and the same firm can now sell 11 widgets at $10 each, resulting in a monthly income of $110. As a result, the marginal revenue for the eleventh widget is $10.

By dividing the change in total revenue by the change in quantity, the marginal revenue is computed. The marginal revenue (MR) function is the first derivative of the total revenue (TR) function regarding the quantity:

MR = ΔTR/ ΔQ

Marginal Revenue Formula

where:

MR = Marginal Revenue

Δ = Dividing the change

TR = Total Revenue

Q = Change in quantity

Assume the price of a product is $10 and the firm produces 20 units each day. By multiplying the price by the amount produced, the total income is computed. The total income in this scenario is $200, or $10 x 20. The total income generated by the production of 21 units is $205. The marginal revenue is determined to be $5, or ($205 – $200). (21-20).

How Can Marginal Revenue Grow?

Marginal revenue rises whenever the revenue generated by manufacturing one more unit of a thing grows faster (or declines slower) than its marginal cost of production. Increasing marginal revenue indicates that the corporation is producing too little in comparison to customer demand and that there are profit prospects if production is increased.

Assume a corporation produces toy troops. It costs the corporation $5 in materials and labor to manufacture its 100th toy soldier after some production. Because the 100th toy soldier sells for $15, the profit on this product is $10. Assume the 101st toy soldier costs $5 as well but maybe sold for $17 this time. The profit for the 101st toy soldier is $12, which is more than the profit for the 100th toy soldier. This is an illustration of growing marginal revenue.

Balancing the Marginal Revenue Scales

Marginal revenue tends to drop as production grows for any given level of customer demand. There is no economic profit in equilibrium since marginal revenue matches marginal costs. In the actual world, markets never attain equilibrium; instead, they gravitate toward a constantly shifting equilibrium. As in the preceding example, marginal revenue may rise as a result of shifting customer demand, which raises the price of an item or service.

It’s also possible that marginal costs are lower than they were before. When the marginal revenue product of labor rises—when employees become more trained, new production methods are adopted, or advancements in technology and capital goods raise output—marginal costs fall.

Profit is maximized at that level of output and price where marginal revenue and the marginal cost of production are equal:

Example

A toy firm, for example, may offer 15 toys for $10 apiece. If the corporation sells 16 units, the selling price drops to $9.50 per unit. The marginal revenue is $2, which is calculated as ((16 x 9.50) – (15 x10)) (16-15). Assume the marginal cost is $2.00; at this moment, the corporation maximizes its profit since the marginal revenue equals the marginal cost.

When a company’s marginal revenue is less than its marginal cost of production, it is producing too much and should reduce its amount provided until the marginal revenue matches the marginal cost of production. As the marginal revenue exceeds the marginal cost, the corporation is not producing enough things and should expand production until profit is maximized.

When Marginal Revenue Begin to Decline

When predicted marginal revenue starts to diminish, a corporation should investigate the reason. Market saturation or pricing battles with rivals might be the trigger.

If this is the case, the corporation should prepare by committing funds to research and development (R&D) to keep its product range fresh. So, if a company believes it will be unable to increase its marginal revenue once it is expected to decline, management must consider both its marginal revenue and the marginal cost of producing an additional unit of its good or service and plan on maintaining sales volume at the intersection of the two.

If the firm intends to increase its volume beyond that point, each extra unit of its item or service will be a loss and should not be produced.

Marginal Benefit vs. Marginal Revenue

Although they may seem similar, marginal revenue and marginal benefit are not the same things. In reality, it’s the opposite. While marginal revenue measures the extra money a firm makes from selling one more unit of an item or service, marginal benefit measures the consumer’s gain from consuming one more unit of a good or service.

The incremental increase in a consumer’s benefit caused by consuming one extra unit of an item or service is referred to as marginal benefit. It usually falls when more of a good or service is consumed.

Consider a buyer looking to purchase a new dining room table. They go to a local furniture shop and spend $100 on a table. They wouldn’t need or desire a second table for $100 since they only had one dining area. So, they could, however, be attracted to buy a second table for $50 since the value is amazing at that price. As a result, the extra unit of the dining room table reduces the consumer’s marginal gain from $100 to $50.

Returning to our widget-maker example, let’s connect the two. Assume a consumer is thinking about purchasing ten widgets. If the marginal advantage of buying the eleventh widget is $3, and the widget firm is willing to sell the eleventh widget to maximize its customer benefit, the marginal income to the company is $3, and the marginal benefit to the consumer is $3.

Marginal Analysis

All of these computations are part of a process known as marginal analysis, which divides inputs into quantifiable pieces. It was first created by economists in the 1870s and progressively became an element of business management, particularly in the application of the cost-benefit method—the determination of when marginal revenue exceeds marginal cost, as we’ve been describing above.

A corporation should continue to grow production until marginal revenue equals marginal cost, according to the cost-benefit analysis. Any other cost is unimportant if the optimum output is where the marginal benefit equals the marginal cost. As a result, marginal analysis informs managers on what they should not consider when making judgments regarding future resource allocation: They should disregard average costs, fixed costs, and sunk costs.

A toy producer, for example, may attempt to assess and compare the costs of creating one more toy with the predicted income from its sale. Assume that the corporation spends $10 on average to create a toy. During the same period, the average sales price was $15.

This does not necessarily imply that more toys should be produced. If 1,000 toys have already been created, the manufacturer should only assess the cost and benefit of the 1,000th item. If the first 1,000 toys cost $12.50 to produce but only $12.49 to sell, the manufacturer should cease production at 1,000.

Can the marginal cost be affected by changes in technology or other factors?

Yes, changes in technology and other factors such as input prices and production processes can greatly impact the marginal cost of producing a good or service.

Can a firm maximize its profit by setting the price equal to marginal cost?

Not necessarily. While setting the price equal to marginal cost can result in a break-even situation, it may not result in the maximum profit for the firm as it ignores the revenue generated from the market demand.

Is it possible for marginal cost to be greater than average cost?

Yes, it is possible for marginal cost to be greater than average cost, particularly in the short run when some inputs are fixed and cannot be adjusted.

How does the shape of the marginal cost curve relate to the shape of the average cost curve?

Marginal cost and average cost are related but not identical functions. While the average cost curve tends to take the shape of a U, the marginal cost curve can take either a positive or negative sloping form.

How does marginal cost impact decision-making for firms?

If a company wants to know how much it will cost to make an extra unit of a product, it needs to know the marginal cost. The company can use this data to figure out its most profitable production level and set prices accordingly.

How does the concept of marginal cost apply to the service industry?

The service sector is also subject to marginal cost analysis, just like the manufacturing sector. A service provider can use the marginal cost to determine the optimal price, output level, and distribution of scarce resources.

Conclusion

To calculate optimal production levels, manufacturers track marginal production costs and marginal profits. When productivity levels fluctuate, the marginal cost of production is computed. This enables firms to establish a profit margin and develop strategies to become more competitive to increase profitability.

The most successful entrepreneurs and business executives recognize, predict, and respond rapidly to changes in marginal revenues and costs. This is a critical aspect of corporate governance and revenue cycle management.

Marginal Cost FAQs

How do I calculate marginal cost?

You calculate the marginal cost by dividing the change in total cost by the change in quantity.

What is the difference between marginal cost and marginal production?

While the marginal product is concerned with changes in production, marginal cost is a representation of the costs spent while producing extra units of a product.

Is marginal cost the same as variable cost?

Variable costs are those that fluctuate when the overall level of production varies. The extra cost spent for manufacturing each additional unit of the product is referred to as the marginal cost.

Related Articles

- Marginal Cost: Meaning, Formulas & How to Calculate, Simplified!!!

- BUSINESS PORTFOLIO ANALYSIS: Overview, Templates & How to Make One

- How to Calculate Home Equity with Practical Examples & All You Need

- FIXED COST: Meaning, Examples, Formula, & How to Calculate

- How to Calculate Break-Even Point (Synonym: Calculate Break-Even Point)

- EQUITY IN BUSINESS: Meaning, Examples & Market Value