The accounting system is pretty vast with several methods of performing the same task. Just like trying to deduce or solve a problem in science, some methods get the job done faster, some give you more accurate results while others are important fragments of the bigger picture. This article will focus on one of such fragments; Double-Entry Accounting. In other words, it will cover the important aspects of the double-entry accounting system including its definition, a practical example, its importance, and so on.

Let’s set the ball rolling…

What is the Definition of a Double-Entry Accounting?

For starters, double-entry refers to a bookkeeping system that ranks as one of the most fundamental foundational concepts in accounting, despite its simplicity. Double-entry accounting basically means that for every input into one account, there must be an equal and opposite entry into another account. It will result in a debit entry in one or more accounts and a credit entry in the same or different accounts. If a company takes out an $8000 loan, for example, double-entry accounting credits assets with $8000 and debits liabilities $8000. In other words, the $8000 represents a boost in cash as well as a debt.

How Does Double-Entry Accounting System Work?

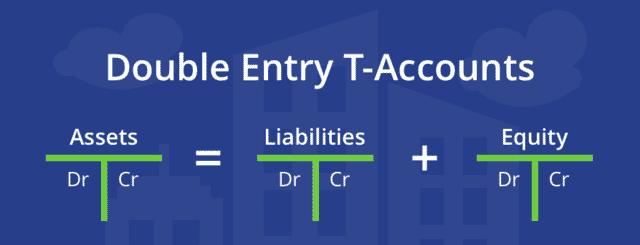

Judging from the definition, a double-entry accounting system’s major goal is to keep a company’s accounts balanced so that management and external stakeholders can see an accurate picture of the company’s current financial situation. As a result, the foundational accounting equation, Assets = Liabilities + Shareholders’ Equity, is frequently used in double-entry bookkeeping.

Accountants utilize the idea of debits and credits to record transactions for each account on the balance sheet in order to obtain the previously indicated balance. A debit entry in one account must equal a credit entry in another account to keep the equation balanced in double-entry bookkeeping.

Basically, debits are usually found on the left side of a ledger, whereas credits are found on the right.

To further demonstrate these, T-accounts come in handy, especially when teaching the idea in foundational accounting schools. And since they provide a visual representation of the flow of figures from one account to the next; professionals also find them very useful.

Double-Entry Accounting History

For hundreds, if not thousands, of years, the double-entry accounting system has been in use. And due to the necessity of recording transactions between parties, accounting has played a critical role in business, and consequently in society, for generations.

Accounting’s origins and evolution can be traced back to Mesopotamian civilizations, and it is strongly linked to the creation of writing, counting, and money. The idea of double-entry accounting, on the other hand, is traced back to the Romans and early Middle Eastern cultures, where rudimentary variants of the approach can be discovered.

In other words, this method dates back to the 13th and 14th centuries when Italian merchants began to adopt it extensively. The double-entry accounting system was initially documented in 1494 by Luca Pacioli, who is now known as the “Father of Accounting.”

This was largely because of his book launch that year, detailing the fundamentals of the double-entry accounting method.

What is the Importance of Double Entry Accounting?

Single-entry bookkeeping may be sufficient for very small, startup firms. You can’t say the same for large corporations. There are several advantages when it comes to double-entry accounting. Let’s go through some of them…

#1. Provides a Full Financial Picture

Double-entry accounting allows small businesses to better track their financial health and growth rate.

Or basically, any company with more than one employee, inventory, debts, or multiple accounts.

Companies that meet any of these requirements require the comprehensive financial picture that double-entry bookkeeping provides. According to Bench Bookkeeping, double-entry accounting can provide a variety of important financial reports such as a balance sheet and income statement.

#2. Aids Businesses in Making Better Financial Decisions

Financial statements generated by double-entry bookkeeping show small businesses how successful they are. It also shows how financially sound different portions of their organization are. Basically, you can see how much money you’ve spent and how well your business is going. This enables a business to make more knowledgeable financial decisions in the future.

#3. Eliminates Errors in Bookkeeping

In double-entry accounting, liabilities and equity (net worth or “capital”) must match assets on a balance sheet. If they don’t, you can be sure your books are incorrect. And if a company’s journal entries are incorrect, this failsafe alerts them.

The double-entry technique is also a more transparent manner of keeping your records in general, which helps firms be more accountable.

#4. Investors, Banks, and Buyers Prefer it

Anyone who is considering donating money to your firm will be far more willing to do so if you use the double-entry approach. This is because it is more complete and transparent.

Investors, banks, and potential buyers may get an accurate and complete view of your company’s financial health using double-entry accounting.

The Equation of Accounting

When we look at the accounting equation, one of the fundamental principles of accounting, the above becomes clearer. This equation must have the same answer on both sides. If they aren’t, there’s a discrepancy in the records.

Here’s how it works:

Liabilities + Equity = Assets

If a result, as assets grow, liabilities must grow as well in order for both sides of the equation to balance.

An e-commerce company, for example, purchases $1000 worth of inventory on credit. Liabilities (accounts payable) increase by $1000, but assets (inventory) also increases by $1000. As a result, the accounting equation is the same on both sides.

Double-Entry Accounting System Example

Let’s have a look at a basic example to help us grasp how double-entry accounting works. Assume ABC Company purchases $6,000 in office furnishings and pays in cash right away. In this situation, one of ABC’s asset accounts – most likely Furniture or Equipment – would need to be increased by $5,000, while Cash would need to be cut by $6,000.

It’s worth noting that the debit amount is exactly equal to the credit amount, $6,000, after the transaction.

Double Entry in the Real World

A bakery uses credit to purchase a fleet of refrigerated delivery trucks; the total credit purchase cost was $500,000. The new vehicles will be employed in commercial operations and will not be sold for at least 10 years, which is their expected life span.

Entries must be made in their individual accounting ledgers to account for the credit purchase. A debit to the asset account for the amount of the purchase ($500,000) will be made because the company has accumulated more assets. A credit entry of $500,000 will be made to notes payable to account for the credit purchase.

Within the same class, double entries are also possible. If the bakery made a cash transaction, a credit-to-cash and a debit-to-asset would be applied, resulting in a balance.

It's vital to understand that a debit or credit does not imply a rise or decrease in value. However, remember that a debit entry is necessary to raise an asset account, whereas a credit input is required to expand a credit account.

The DEAD RULE

The DEAD rule is a simple mnemonic that helps us remember to always Debit Expenses, Assets, and Dividend accounts, in that order. In such cases, the normal balance is a debit, and debits increase the accounts while credits decrease them. Once you understand the DEAD rule, it’s easy to see how any other accounts would be handled in the exact opposite way as the DEAD rule accounts.

Types of Accounts

Asset, liability, capital, expense, and income accounts are among the most frequent types of accounts in the world of accounting.

- Asset accounts help to track the items, equipment, and cash that a company possesses.

- Liability accounts are accounts that show what a company owes to other businesses or suppliers, such as equipment or items they buy on credit, a building mortgage, or credit card amounts that will be paid later.

- Capital accounts are accounts pertaining to shareholders’ equity, such as common stock, preferred stock, and retained earnings.

- Expense accounts show how much money was goes to things like advertising, wages, administrative fees, and rent.

- Income accounts help to track the various kinds of money received from different sources, such as interest, investment income, and revenue from the sale of goods and services.

Who Makes Use of Double-Entry Accounting?

The double-entry accounting system is required by law for public enterprises. For the most part, the Financial Accounting Standards Board (FASB), a non-governmental organization, makes decisions on generally accepted accounting principles (GAAP). On the other hand, GAAP requires public firms to follow all rules and methods.

Double-entry accounting is also a compulsory practice for small firms with more than one employee or those intending to qualify for a loan. This technique provides a more accurate and comprehensive way to track a company’s financial position and growth rate.

How to Avoid Errors Using Double-Entry Accounting

When a firm grows and its business transactions become more complicated, the likelihood of administrative errors increases. You should understand that double-entry accounting does not completely eliminate errors. Rather, it helps to reduce them on balance sheets and other financial statements by requiring debits and credits to balance.

It follows the formula Assets = Liabilities + Shareholders’ Equity, of course. The balancing requirement ensures that any errors are quickly identified. It also ensures that the business can track the incorrect entry can be before it leads to more complicated errors.

What Is Double-Entry in Accounting?

What is the definition of double-entry accounting? Double-entry accounting is a bookkeeping approach that keeps track of where your money comes from and where it goes. Every financial transaction has two entries: a “debit” and a “credit” to indicate whether money is transferred to or from an account.

What Is the Main Rule for Double-Entry Accounting?

The double-entry rule is as follows: whenever a transaction increases the value of an asset or expense account, the value of the increase must be recorded on the debit or left side of these accounts.

What Are the Four Rules of Double-Entry?

Every business transaction is recorded in two or more accounts under the double-entry system of bookkeeping.

Principles of the Double-Entry Accounting System:

- Credit is written on the right, debit on the left.

- Every debit must be matched by a credit.

- Debit receives the benefit, whereas credit provides it.

What Are the Types of Double-Entry?

In double-entry accounting, transactions can be recorded using any combination of the five types of accounts: assets, liabilities, equity, revenue, expense, gains, and losses. Each journal entry has two sides. On the left is a debit, and on the right is a credit.

Why Is It Called Double-Entry?

Double-entry bookkeeping is a way to keep track of business transactions in which an entry is made in at least two accounts for each business transaction, either as a debit or a credit. In a double-entry system, the amounts written down as “debits” must match the amounts written down as “credits.”

- GENERAL LEDGER: Easy Templates, Examples And all you need (+ Free pdfs)

- Cash Accounting: Best Cash Accounting Methods In 2023 (+ Detailed Guide)

- ACCOUNTING PROCESS: Understanding the 8 Steps in the Accounting Cycle

- ACCOUNTS PAYABLE PROCESS: How to Manage the Process Effectively

- Automating Accounts Payable Process: What You Should Know Before Automation