The majority of individuals across the globe are presumed to be aware of their home equity. However, quite a number of them, get lost along the line. As a homeowner, you must fully understand how home equity works. This is especially true if you want to refinance your mortgage or take out a loan against your home. Basically, this is a simplified guide that will help you calculate home equity seamlessly, covering all you should know about home equity, home equity loans, and all you should know threading down this path.

But before delving fully into that, let’s quickly cover the basics.

What is Home Equity?

Simply put, the value of a homeowner’s interest in their home is known as home equity. In other words, it is the present market worth of the property (less any liens that are attached to that property). Hence, as more mortgage payments are made and market forces affect the present value of the property, the amount of equity in a house—or its value—fluctuates over time.

How Does Equity Work in a Home?

When a portion—or all—of a home is purchased with a mortgage loan, the lending institution holds a lien on the property until the loan is repaid. The part of a property’s present worth that the owner actually owns at any one time is referred to as home equity.

The down payment you make during the original purchase of the property is how you build equity in a house. Then, when a contracted amount of your mortgage payment is assigned to bring down the remaining principal you still owe on the loan, you will gain greater equity through your mortgage payments. Property value appreciation might also benefit you because it will improve your equity value.

What is a home equity loan, on the other hand?

What Exactly is a Home Equity Loan and How Does it Work?

A home equity loan is a type of debt consolidation loan that uses your property as collateral. Home equity loans and home equity lines of credit (HELOCs) are the two types of home equity loans.

But then home equity loans are similar to personal loans in that you receive a lump sum payment from the lender and return the loan in monthly installments. A HELOC, on the other hand, works similarly to a credit card in that it allows you to borrow money as needed. The draw durations for HELOCs are typically 10 years. You can use money from the credit line during this time, and you’re just responsible for interest payments.

Both alternatives require you to have a particular amount of home equity, which is the percentage of your property that you own. Lenders usually need you to have between 15 and 20 percent equity in your home.

Divide your current mortgage balance by the market value of your house to find out how much equity you have. If, for example, your current balance is $100,000 and your home’s market value is $400,000, you have a 25% equity stake in the property.

A home equity loan may be an excellent option if you can afford to repay the amount. If you can’t afford to pay back the loan, the lender may foreclose on your house. This can damage your credit, making it difficult to qualify for future loans.

Basic Uses for Home Equity Loans

According to Bankrate, the most popular reasons homeowners borrow from their equity are debt consolidation and home improvements. Borrowers may use home equity for a variety of reasons, including education expenditures, vacations, or other large purchases.

Borrowers can deduct interest paid on HELOCs and home equity loans if they use the funds to buy, develop, or enhance the home that serves as collateral for the loan under the Tax Cuts and Jobs Act of 2017.

However, the interest rate on a home equity loan varies depending on the lender and the home equity product you choose. In 2020, for example, home equity loan rates were 5.1 percent to 5.89 percent, while HELOC rates were 4.52 percent to 6.2 percent.

One disadvantage, on the other hand, is that closing expenses and fees for home equity loans and lines of credit are identical to those on a traditional mortgage. Closing costs vary, but depending on the property’s worth, they might range into hundreds of dollars.

How to Make an Application for a Home Equity Loan

Start by verifying your credit score, determining the amount of equity in your property, and examining your finances before applying for a home equity loan.

Next, look at home equity loan rates, minimum requirements, and fees from a variety of lenders to see if you can afford a loan. While you’re at it, also double-check that the lender offers the home equity product you require; some only offer home equity loans or HELOCs, not both.

Personal information such as your name, date of birth, and Social Security number will be requested when you apply. You’ll also have to provide evidence, such as tax records, pay stubs, and confirmation of homes insurance.

How Much Equity Do You Have In Your Home?

The difference between the current market worth of your property and the total quantity of loans (most notably, your principal mortgage) lodged against it is your home equity value.

The amount of credit you can get through a home equity loan is determined by how much equity you have. Assume your home is valued at $250,000 and your mortgage balance is $150,000. You’ll have $100,000 in home equity if you deduct your remaining mortgage from the home’s worth.

Subtract the amount you owe on all loans secured by your home from its appraised value to determine how much equity you have in your home.

How Big a Home Equity Loan Can You Get & How to Calculate

Only a few lenders will allow you to borrow the entire amount of your home equity. Depending on your lender, credit, and income, you can often borrow 80 percent to 90 percent of the available equity. So, in the case above, if you had $100,000 in home equity, you may receive an $80,000 to $90,000 home equity line of credit (HELOC). When assessing how much home equity you can borrow, race, national origin, and other non-financial factors should never be taken into account.

Here’s a second example that considers a few more variables. Assume you’ve been paying on your property for five years and have a 30-year mortgage. In addition, according to a recent appraisal or assessment, the market worth of your home is $250,000. And say, you still owe $195,000 on the original $200,000 loan. Keep in mind that practically all of your early mortgage payments are used to pay down the interest.

In other words, you have $55,000 in home equity if there are no other debts attached to the property. This is equal to the current market worth of $250,000 minus the $195,000 in debt. You can also calculate your home equity percentage by dividing your equity by the market value. The home equity proportion in this situation is 22 percent ($55,000 divided by $250,000 =.22).

Let’s say that in addition to your mortgage, you also have a $40,000 home equity loan. Instead of $195,000, the total debt on the property is $235,000. Your overall equity drops to just $15,000, bringing your home equity percentage down to 6%.

Costs of Transactions

Because real estate is one of the most illiquid assets, taking out a loan against your home equity usually comes at a price. Total closing fees in the United States are normally between 2% and 5% if you ultimately sell the residence. Many of these costs are normally paid by buyers, but be aware that they could be used as a justification to negotiate a lower sale price.

If you get a home equity loan, you’ll almost certainly have to pay a loan origination charge. Second mortgages and home equity lines of credit (HELOCs) typically have higher interest rates than the initial mortgage. After these transaction fees are included, the amount of home equity you can really use is less than what you have in theory.

The Loan-to-Value Ratio

The loan-to-value ratio is another approach to communicate equity in your home (LTV ratio). The remaining loan balance is divided by the current market value to arrive at this figure. Your LTV is 78 percent in the second scenario stated above. (Yes, it’s the inverse of your 22 percent home equity percentage.) It rises to 94 percent when you add in your $40,000 home equity loan.

Lenders dislike high LTVs because they indicate that you may be using too much leverage and may be unable to repay your debts. They might tighten lending conditions during times of economic turmoil. A perfect scenario was seen during the economic crisis of 2020. Banks increased their credit score criteria, particularly for home equity lines of credit (HELOCs), from the 600s to the 700s. There was also a reduction in the amount of money they were willing to lend and the percentage of home equity they were willing to offer.

Furthermore, when the market value of a home fluctuates, both LTV and home equity values fluctuate. During the subprime mortgage debacle of 2007–2008, millions of dollars in ostensible home equity were wiped out. Prices do not always increase. The impact of the 2020 crisis on house equity, in the long run, is unknown. Indeed, global housing prices were expected to rise until 2021 as a result of the stay-at-home policy and individuals seeking larger homes to accommodate their work, schooling, and personal lives.

In addition, firms’ expanding work-from-home policies, which may extend beyond COVID, have enticed many families to relocate from the city to the suburbs.

What Impact Does the Loan-To-Value Ratio Have On Your Loans?

The loan-to-value ratio is a popular metric that lenders use to make loan and finance decisions (LTV). This calculation compares the amount of the loan you’re seeking to the home’s value when you first apply for a mortgage. If you have a mortgage, your LTV ratio is calculated using the balance of your loan. If you have a high LTV ratio, you may be compelled to pay private mortgage insurance (PMI) or you may be able to refinance.

Divide your existing loan balance (found on your monthly statement or online account) by the appraised value of your house to get your LTV ratio. To convert that figure to a percentage, multiply it by 100.

Equity and Private Mortgage Insurance

Keep track of your loan-to-value ratio if you paid private mortgage insurance (PMI) on your first mortgage. When a home’s LTV ratio is 78 percent or below, the Homeowners Protection Act compels lenders to automatically remove PMI (provided certain requirements are met). When your loan total hits 78 percent of your home’s initial appraised value, your loan is usually canceled. You have the right to request that your lender remove your PMI if your LTV ratio falls below 80% ahead of schedule due to extra payments you made.

Obtaining a Home Equity Line of Credit (HELOC)

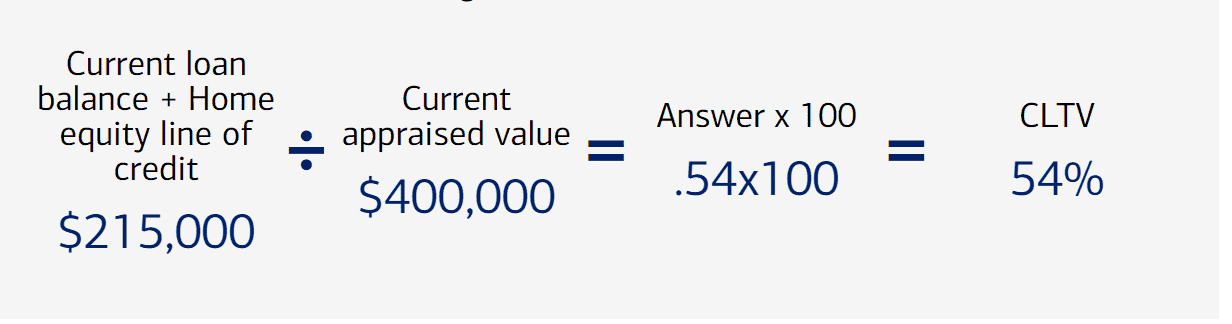

Another key statistic to make if you’re considering a home equity loan or line of credit is your combined loan-to-value ratio (CLTV). The worth of your house is compared to the entire amount of loans secured by it; including the loan or line of credit you’re looking for.

Trisha has a $140,000 loan outstanding and wants to apply for a $75,000 home equity line of credit. If she were accepted, she calculates her CLTV ratio as follows:

Using the combined loan-to-value ratio to calculate the loan-to-value ratio;

To qualify for a home equity line of credit, most lenders require a CLTV ratio of less than 85% (though this percentage may be lower or vary from lender to lender), therefore Trisha would most likely be eligible.

It’s crucial to keep in mind, however, that the value of your home can change over time. You might not be eligible for a home equity loan or line of credit if the value drops. Worse still, you can end up paying more than your home is worth.

How Can You Raise Your Home Equity?

If the value of your property drops over time, your equity may decrease as well. You can rebuild or increase home equity by paying down your loan’s principal and lowering your loan-to-value ratio if it remains constant, that’s after you’ve been able to calculate the variables. However, this happens automatically if your payments are amortized (that is, based on a plan that allows you to return your loan in full at the end of its term).

So, consider paying more than your needed mortgage payment each month if you want to reduce your LTV ratio faster. This aids in the reduction of your loan balance. (Make sure you don’t have any prepayment penalties on your loan.)

Furthermore, maintain the value of your house by keeping it clean and well-kept. You may also be able to raise the value of your home by making modifications. However, before investing in any renovations that you expect would increase the value of your house, you should consult an appraiser or real-estate consultant. Remember that no matter what you do, economic conditions might affect the value of your home. If home prices rise, your LTV ratio will decline and your home equity will rise, whereas decreasing home prices would negate the value of any upgrades you make.

What Is the Importance of Home Equity & Knowing How to Calculate?

For a variety of reasons, increasing your home’s equity is critical. To begin with, it contributes to your net worth because, unlike nearly every other asset purchased with a loan, your home can continue to appreciate in value after you have paid it off. You can also use your equity to support living expenses such as home renovations, a down payment on a second property, or schooling – we’ll get into that later. Finally, the more equity you’ve built up in your home, the more profit you’ll be able to make when it’s time to sell it. But then, equity takes time to grow, therefore it should be part of a long-term financial strategy rather than a quick cash plan.

On the other hand, these would be impossible to achieve without an in-depth knowledge of how to calculate your home equity, LTV, and so on.

What Are My Options for Accessing My Home Equity?

Now that you know how to calculate your home equity, you also need to know how to access it. There are various ways to access your home equity, each with its own set of advantages and disadvantages. Here are a few of the most popular:

Home Equity Loan: A loan with a fixed rate and a lump sum payment that has a predictable monthly payment.

Home Equity Line of Credit (HELOC): A revolving credit line that allows you to borrow money using a portion of the equity in your home.

Cash-Out Refinance: A mortgage that replaces your current one but is larger than your loan total, allowing you to pay out the difference.

Reverse Mortgage: A loan for homeowners aged 62 and up in which the lender pays you back your equity.

Home Equity Investments: These loans provide you with near-immediate funds in exchange for a percentage of your home’s future value without requiring you to sell or take on more debt. There are no monthly payments or interest to worry about.

What Can I Do With My Equity?

While there are numerous ways to use your home equity it eventually pays off, in the long run, to be deliberate and strategic about how you use the monies you get. Spending the money on house upgrades that can potentially increase the value of your home, for example, is definitely a better decision against going on a luxurious vacation or shopping binge. Here are other options to keep in mind:

#1. Getting Out of Debt

One of the most common reasons for homeowners to use their equity is to pay off debt, such as credit cards and student loans. This can be made even easier with a home equity loan because there are no monthly payments to worry about.

#2. Renovate Your Residence

Home improvement and renovation projects are other typical uses of equity. The advantages are excessive. First, you’ll have the luxury and pleasure of having that ideal kitchen or lovely patio. As previously said, the remodeling may also enable you to earn more money for your home if you decide to sell in the future.

#3. Purchase a Second Residence

Have you ever fantasized about owning a holiday home? What about a rental property that generates additional income? You can use your equity to help fund a down payment on a new home. You’ll be diversifying your portfolio with real estate in addition to having a go-to getaway destination.

#4. Your Company’s Funding

Tons of homeowners take advantage of their home equity to establish or expand their small businesses without having to take out a loan (and the hurdles that come along with getting approved for one).

#5. Enjoyable Retirement Life

If you need money for current — or future — expenditures that your retirement savings won’t cover, such as health care, your home equity can come to your rescue and provide you with peace of mind as well as some extra cash. This is particularly appealing if you intend to sell your house within the next ten years. Though it is not needed, it may be advantageous to utilize the funds from the sale of the home to pay down for retirement plans.

#6. Invest in Education

With college tuition rising every year, it may be a wise decision to use your equity to help pay for your child’s education or to begin paying down your student loan debt.

#7. Diversify Your Investment Portfolio

Home equity investments are a popular way for homeowners to diversify their portfolios. A well-rounded portfolio comprises stocks, bonds, mutual funds, and real estate, as well as other investments that span at least a few different industries. You can reduce the danger of a substantial loss in one place by dispersing your assets.

#8. Invest in Your Growing Family

It’s no secret that the costs of growing your family, whether it’s your first or fourth child, can quickly pile up. Childbirth, IVF, adoption, surrogacy, and raising a kid can all be paid for with the equity in your home.

#9. Obtain Emergency Money

Unexpected events abound in life. Whether you need cash quickly to pay medical bills or deal with other unexpected expenses, your home equity can help.

These are just a few examples of ways you may use your equity to live a less stressful life — and a home equity investment can help you accomplish it without taking on debt, worrying about monthly payments or interest, or selling your property. Now you can decide how you’ll use your home equity considering that you know how to calculate it, what it is, and why it’s significant!

How Do I Calculate 20% Equity in My Home?

To Calculate 20% Equity in Your Home, you’d need to follow the steps below;

- Determine your home’s fair market worth. To have your home appraised, contact a professional appraiser.

- Calculate the amount you owe on your mortgage.

- To figure out how much equity you have, subtract your loan balance from the fair market value of your home.

How Do You Calculate Percentage of Equity?

To calculate your home equity percentage, divide your equity by the market value of your home. (45,000 divided by 200,000 is 22.5) You have a home equity percentage of 22.5 percent in this case.

What Is the Payment on a 50000 Home Equity Loan?

An example of a loan payment is $501.49 per month for a $50,000 loan with a 3.80% interest rate over 120 months.

How Much of My House Equity Can I Borrow?

Home equity loans are secured by your property, so you cannot borrow more than the value of your home’s equity. Your equity is the difference between the value of your property and the amount you owe on your mortgage. Lenders may lend you up to 85 % of this value.

How Does Home Equity Work?

Your equity is the proportion of your property that you own relative to the amount you still owe on your mortgage. For instance, if your home is worth $300,000 and you owe $150,000 on your mortgage, you have equity of $150,000, or 50 percent.

DISCLAIMER!!!

We make every effort to ensure that the information in this post is as accurate as possible as of the date it was written, but things can change quickly. Any linked websites are not endorsed or monitored by BusinessYield Consult. Individual circumstances vary, so talk to a financial, tax, or legal professional to figure out what's best for you.