If you’re interested in learning more about cost-based pricing, including its advantages and disadvantages, you’ve come to the right place. Cost-based pricing is a strategy in which the selling price of a good or service is based on how much it costs to make it. I want to share everything I’ve learned about this vital pricing strategy through real-life examples.

Whether you’re a business owner like me or someone who wants to learn more about pricing strategies, this article will provide you with the necessary information. You won’t want to miss out on value-based pricing vs cost-based pricing and cost-based pricing examples. I’m excited to share this information with you. Let’s get started!

Key points

- Cost-based pricing involves summing up all manufacturing expenses, including variable and fixed costs, and then setting a price that covers them while making a profit.

- Understanding internal and external issues, like how competitors and customers view your firm, is crucial.

- Customers value a product or service in terms of value-based pricing. Changing market conditions, customer needs, and product or service features determine price strategy.

- Cost-based pricing is straightforward and predictable. However, undervaluing items, neglecting market demand, and not generating the most money in shifting marketplaces are risks.

- Cost-based pricing includes positives and cons that organisations must weigh to determine if it suits their strategy and market performance.

- Calculate overall production costs, including variable and fixed costs, and determine a price that covers expenses and makes a profit.

- Understanding internal operating expenses and external issues like competition and customer perceptions is crucial.

- Value-based pricing prioritizes the perceived value of the product or service to customers. The choice of pricing strategy depends on factors such as market dynamics, customer preferences, and the offering’s unique value proposition.

- While cost-based pricing offers simplicity, ease of calculation, and stability in pricing, potential drawbacks include the risk of undervaluing products and neglecting market demand. and a potential inability to maximize profits in dynamic markets.

- Businesses must weigh the pros and cons of cost-based pricing to determine whether it aligns with their overall business strategy and market conditions.

What is Cost Based Pricing

Cost-based pricing is a business strategy in which the prices of goods are set by carefully calculating the costs of making and running the business. This method ensures that all the costs of product marketing are considered. By carefully considering these factors, companies can set prices that cover costs like raw materials, labor, and overhead. This way, they can also make an intelligent profit margin.

All the production cycle costs are carefully examined at the start of the process, making it easy to see how much money needs to be spent. After moving away from this cost-centered view, companies use the collected cost data to create pricing plans that are both competitive and long-term. Cost-plus pricing is like a financial compass; it helps businesses find the right mix between recuperating costs and making money in a constantly changing market.

Cost-Based Pricing Example

Consider a hypothetical scenario for a company manufacturing custom-made furniture using cost-based pricing.

Step 1: Identify Costs

The first step in cost-plus pricing is identifying and calculating all relevant prices for producing a product unit. This includes:

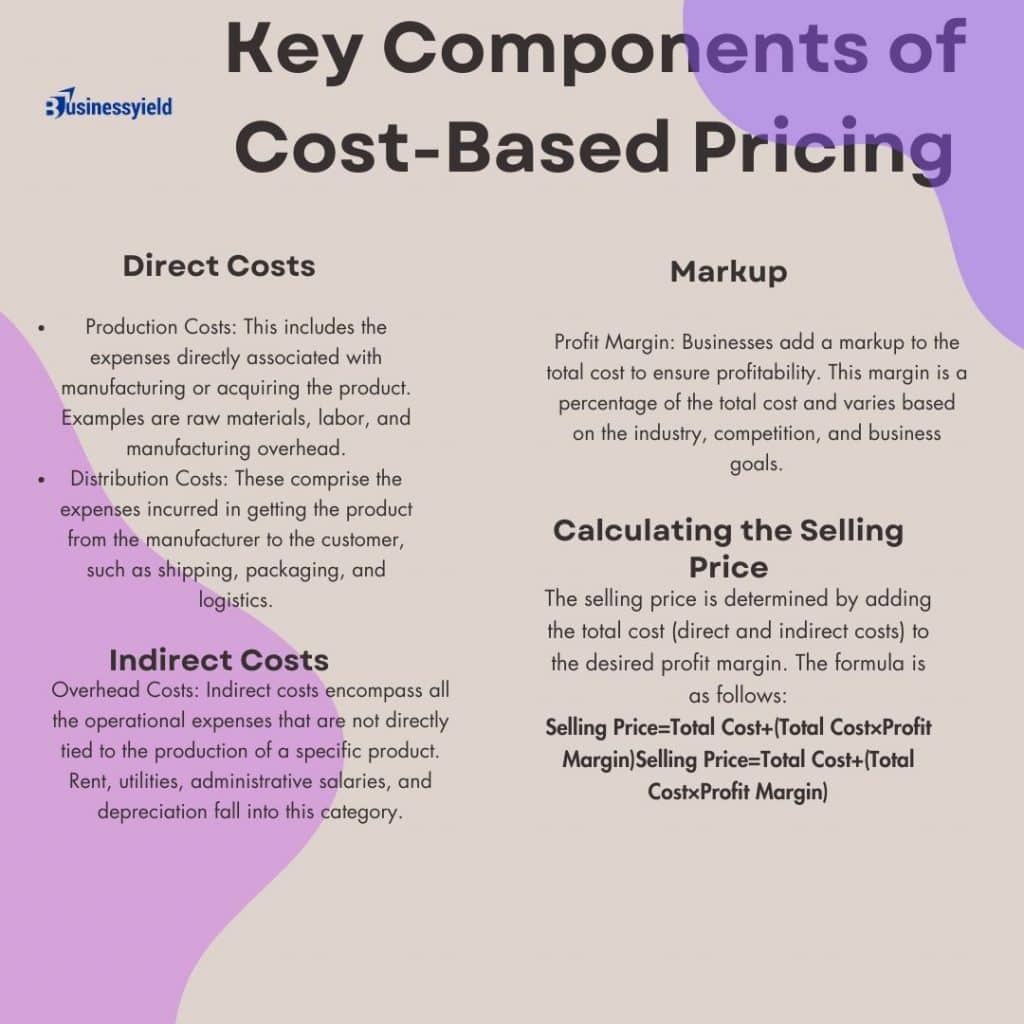

- Direct Costs:

- Raw materials (wood, fabric, etc.)

- Labor costs (wages for skilled artisans)

- Direct overhead (costs directly tied to production, like utilities for the workshop)

- Indirect Costs:

- Indirect overhead (shared costs, such as rent for the entire facility’s administrative expenses)

Step 2: Calculate Total Cost

Credit: pvproductions

Let’s assume the total direct and indirect costs for producing one custom-made piece of furniture are $500.

Step 3: Add Profit Margin

Next, the company decides on a desired profit margin. For this example, let’s say they want a 20% profit margin on the total cost.

Total Cost + (Total Cost x Profit Margin Percentage) = Selling Price

$500 + ($500 x 0.20) = $600

Step 4: Set the selling price.

Therefore, the company would set the selling price for the custom-made furniture at $600 to cover all costs and achieve the desired profit margin.

This approach ensures that the company covers its production expenses and allows a profit to be reinvested into the business or used for future expansions. It provides a transparent and systematic method for determining prices that are both competitive in the market and sustainable for the company.

What Is Cost Value-Based Pricing?

Cost-value-based pricing is a method that surpasses the traditional cost-based pricing approach. This method considers how much a customer perceives a product or service as worth. Unlike the conventional approach that only focuses on production costs, this method assumes the benefits, features, and overall value of what a business is selling. Customers pay for a product or service based on the value they see in it, and companies can set prices accordingly to include production costs and perceived value. This approach can make businesses more competitive, cater to a broader range of customers, and gain a fair market share by setting prices that align with the perceived value of their products or services.

Read also: What Is Pricing? Understanding Pricing In The Marketing Mix

Value-Based Pricing vs Cost Based Pricing

From what I’ve learned, cost-based pricing is based on how much it costs to make something, ensuring that costs are paid while still leaving a profit margin. On the other hand, value-based pricing looks at how much customers think something is worth and how much they are willing to pay based on perks and the market’s movement.

Cost-based Pricing is based on how much something costs to make. However, my study suggests that this method might not consider outside factors like market trends and customer tastes. On the other hand, value-based pricing sets prices based on what customers want and what the product is worth.

Based on my research, it is simple, but value-based Pricing seems better at meeting the market’s needs. It looks at how customers feel about a brand, how well-known it is, and what makes a product unique. This could help businesses charge more and make more money generally.

Cost-Based Pricing Strategy

Cost-based pricing is a way of setting prices for goods and services based on carefully determining their cost of production. It involves selecting the best pricing structure by considering direct expenses, overhead fees, and targeted profit margins. By using this method, businesses can ensure that the prices they set cover their production costs and allow them to make the profit level they want.

This approach is used in industries where production costs play a significant role in determining the final price. Businesses utilize cost-based pricing to achieve financial goals while maintaining transparent and honest pricing. Cost-based pricing may not be as flexible as other pricing strategies based on the market, but it gives businesses a solid way to cover their costs and make a lasting return.

Check out our article on Maximizing Revenue for Restaurants: Exploring Cost-Effective Strategies

Cost-Based Pricing Advantages and Disadvantages

Advantages

- Simplicity: cost-plus pricing is straightforward, making it accessible for businesses of all sizes.

- Cost Recovery: It covers all production costs, helping the business recover expenses and maintain financial stability.

- Profit Control: The method allows for a predetermined profit margin, providing a clear understanding of the profitability associated with each unit sold.

- Stability: Since it relies on tangible costs, cost-based pricing can offer stability, making it easier for businesses to manage and plan financially.

- Transparency: Customers may appreciate the openness of cost-based pricing, as it provides a clear rationale for the product’s price.

Disadvantages

- Ignores Market Dynamics: cost-plus pricing may overlook market demand and customer willingness to pay, potentially leading to missed opportunities for higher profits.

- Competitive Pressures: In competitive markets, competitors’ pricing strategies influence customer perceptions, disadvantaging businesses using cost-based pricing.

- Limited Flexibility: This method may not adapt quickly to market changes, making it difficult for companies to respond to ever-changing environments.

- Neglects Value Perception: Cost-based pricing ignores a product’s perceived value, which can lead to underpricing or overpricing based on customer perceptions.

- Doesn’t Encourage Efficiency: Relying solely on costs may not incentivize businesses to improve efficiency, innovate, or differentiate, as the focus is primarily on covering expenses and obtaining a set profit margin.

Comprehensive Checklist for Cost-based Pricing

Types of Cost-Based Pricing

Here are the types of cost-based pricing to consider:

#1. Cost-Plus Pricing

In this approach, businesses calculate the total production cost and then add a markup percentage to determine the selling price. The markup accounts for profit and often includes overhead and other indirect costs.

#2. Full Cost Pricing

Full-cost pricing considers both variable and fixed costs associated with production. It ensures that all costs, including direct materials, labour, and overhead, are accounted for when setting prices.

#2. Marginal Cost Pricing

Explanation: Marginal cost pricing focuses on the variable costs of producing one additional unit. The selling price is set based on the incremental cost of producing each additional item without considering fixed overhead.

#3. Absorption Cost Pricing

Absorption cost pricing includes all direct and indirect costs associated with production, allocating a portion of fixed overhead to each unit. This method aims to recover all production costs, both variable and fixed.

#4. Target Costing

Target costing involves setting a target selling price based on market conditions and customer expectations. The business then works backwards to determine the allowable production cost to achieve the desired profit margin.

#5. Rate-of-Return Pricing

Rate-of-return pricing sets prices to achieve a targeted rate of return on investment. Businesses determine the selling price by considering the anticipated profit relative to the total investment in the production process.

#6. Uniform Delivered Pricing

Uniform-delivered pricing sets a consistent selling price for a product regardless of the customer’s location. The business absorbs transportation costs, providing a standardised price for all customers.

What Is the Meaning of Cost-Based Transfer Pricing?

The cost of making the goods or services determines the price of moving them from one department or section within the same company to another. The phrase “cost-based transfer pricing” refers to a method for determining the internal price of goods or services transferred between different departments or divisions of a company. This method has the selling section figure out the transfer price by adding direct and variable costs and a profit markup for making the goods or services.

The goal is to ensure that the selling division is rewarded for its work and expenses and that the internal move doesn’t cost the buying division too much. In decentralized organizations, this method is often used to facilitate smooth deals between different units while keeping costs down and ensuring people are held accountable.

What Is Cost-Based Pricing Framework?

A cost-based pricing framework is a strategic approach for determining an item’s retail price or service by analyzing and incorporating various production costs. This framework typically includes the following key elements:

#1. Cost Identification

We identify and categorize all relevant costs associated with producing a product or service, such as direct materials, labor, and overhead expenses.

#2. Cost Calculation

It calculates the total production cost by summing up the identified costs. This includes variable costs that vary with the production volume and fixed costs that remain constant regardless of the production level.

Credit: freepik

#3. Markup Determination

We are establishing a markup percentage or fixed amount to be added to the total production cost. The markup represents the desired profit margin and may include allowances for overhead and other indirect costs.

#4. Selling Price Setting

I am setting the final selling price by adding the calculated markup to the total production cost. This price is expected to cover all expenses and generate the targeted profit for the business.

#5. Market Consideration

Optionally, factoring in market conditions, competitor pricing, and customer perceptions ensures that cost-plus pricing aligns with external market dynamics.

#6. Adjustment and Review

It periodically reviews and adjusts the cost-plus pricing framework to adapt to changes in production costs, market conditions, or business objectives.

The cost-based pricing framework provides a structured and systematic approach for businesses to establish prices that cover their expenses and meet profit goals. It is beneficial in industries where the production of The final price is heavily influenced by expenses: a product or service.

- GROSS PROFIT MARGIN: Meaning, Examples, Formula, Difference & How to Calculate it(

- PRICING STRATEGIES MARKETING: Definition, Types & How to Choose

- TRADING ON MARGIN: What It Means and Examples

- WHAT IS CONTRIBUTION MARGIN?: Formula and Calculations

- WHO BENEFITS FROM INFLATION: Biggest Winners & Losers