Money orders are nearly as simple to fill out as a personal cheque. Different channels employ various formats, but they all want the same core information. Most money orders are processed by one of three companies: Western Union, MoneyGram, or the United States Postal Service.

Here’s a step-by-step guide to when to use a money order, where to purchase one, and how to properly fill it out.

What Is a Money Order?

A money order looks and functions similarly to a check, but you do not need to have a bank account to use one. This is because you pay the face value of the money order when you purchase it. You can purchase one for a few dollars more than the face value using cash or a credit or debit card.

When Should You Use a Money Order?

When you need to pay someone or someone needs to pay you and cash, a personal check or a smartphone app aren’t viable options for whatever reason, a money order may be the answer.

A money order is a piece of paper, but it is more secure than cash because it is addressed to a specific recipient, who must endorse it and provide identity to cash it. Money orders are useful for those who do not have a bank account or who do not wish to accept personal checks. Even if you use checks, you may not want to reveal the personal information printed on them with specific recipients, such as your address and account number. Money orders are generally accepted since they are prepaid, which eliminates the risk of a bouncing check.

Money orders are not as secure as certified and cashier’s checks issued by financial organizations. They do, however, have substantially higher fees and necessitate visiting a bank during business hours, whereas a money order is a simpler and less expensive choice.

Where Can You Get a Money Order to Fill Out?

So yet, online money orders are uncommon and expensive. So, to purchase a money order, you must normally go to a store that sells them and depart with a paper money order in hand.

Fortunately, many locations in the United States sell money orders, many of which have late and weekend hours. You may get one at any Walmart, CVS, or 7-Eleven, as well as any of the 31,300 USPS retail locations. Money orders are also available from banks, credit unions, grocery store chains, and check-cashing services.

Money orders have a $1,000 restriction, but you can order more than one at a time.

Related: Can you Buy a Money Order with a Credit Card? (Pros & Cons)

What is the Cost for Money Orders?

Almost all money order purchases are subject to a fee, so it’s a good idea to shop around. Most Walmart shops charge $1.00, but the USPS charges $1.30 to $1.75 depending on the amount. Prices are much higher on the international market. The USPS, for example, charges at least $10.55 plus a surcharge.

Banks, credit unions, and other merchants’ prices can be much higher. Some banks, on the other hand, provide them for free to certain types of consumers.

Credit card issuers typically impose exorbitant fees for money order purchases since they are treated as cash advances. You may also accrue interest charges, so avoid this alternative if at all possible.

Related: How to Cash a Cashier’s Check: All you should know

What Information Is Required to Fill Out a Money Order?

To fill out a money order, you must first know the precise monetary amount you require. This will be machine-printed directly on the money order and cannot be changed later. You must also have the full name of the person or firm to whom you will issue the money order. If you are not accurate, the recipient may have difficulty cashing it.

When paying a business, include the account or invoice number to guarantee that the payment is properly credited to you. You can fill out this information later, but if it’s lost or stolen, a blank money order (as long as the cash amount is on it) is as good as cash.

Also, unless you’re at your bank and can withdraw it from your account, bring a debit card or cash to pay for your money order.

Note: If you neglect to fill out the recipient’s name on your money order and then lose it, anyone can cash it; it is essentially found money.

Read Also: WHERE CAN I GET A MONEY ORDER: Best Locations

General Information

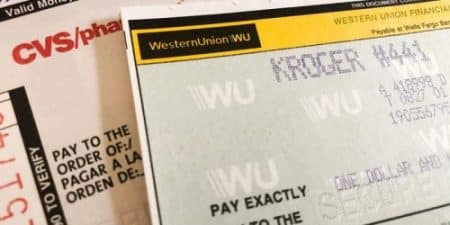

The procedures for filling out a money order differ depending on the organization, whether it’s Western Union or the US Postal Service. The appearance of each institution’s money order may also differ slightly. However, you will typically require the following information:

However, to properly fill out a money order, you must include the following information:

#1. Name:

Include the entire name of the person or business being paid with the money order. This box could be titled “Pay to the order of,” “Pay to,” or “Payee.” If you leave this section empty or make the money order payable to cash, anyone can cash it and you risk losing the funds if the money order is lost or stolen. Some issuers also demand the purchaser’s name in the “From” box.

#2. Address:

Some money orders ask for your current mailing address in case the recipient has to contact you about the payment. If you are concerned about your privacy, you may be able to omit this information. Inquire with the money order issuer and the recipient about the requirements. USPS money orders have an address field on the left for the recipient’s address and another on the right for the purchaser’s address, so both the recipient’s and your addresses are displayed.

#3. More information:

You may need to include additional information on the money order in order for the payment to be processed appropriately. This may contain your account number, transaction or order data, or any other information that will assist the recipient in determining the cause for the payment. This field could be titled “Re:” or “Memo.” If there isn’t a field for it, write it on the front of the paper.

#4. Signature:

Some money orders necessitate a signature. On the front of the document, look for a field labeled “Signature,” “Purchaser,” or “Drawer.” Do not sign the documents back because this is where the recipient will sign to endorse the money order.

Keep all receipts, carbon copies, and other documentation you receive after filling out your money order in case there is a problem with your payment. These documents may be required to cancel the money order, and they might be useful when tracing or confirming a payment.

To purchase the money order, you will also need a mode of payment (cash, check, debit card). Some issuers also limit your payment options. For example, you will very certainly be unable to purchase a money order with a credit card.

How to Fill Out a Money Order

It’s simple to learn how to draft a money order, but it’s critical that you do it correctly. You can ensure that your cash are sent to the correct person or business by following these simple procedures.

#1. Fill the Payee’s Name

The payee is the person or money who receives the money order. If you’re making a cash payment to an individual, this may be a person. If you’re utilizing the money order to pay a bill, it may be the name of a company.

The name of the payee or recipient should be written in the field marked “Pay to the Order of” or “Pay to” on your money order. If the money order is lost or stolen, write their name clearly and in ink so that it cannot be changed later.

Filling out the payee area first is critical because anyone can enter their name on the money order and cash it until that is done.

#2. Enter the Payee’s Address

You should notice another field for the payee’s address underneath the space for the payee’s name. This is where you’ll enter the recipient’s address.

You may include the payee’s home address if they are a person. If you’re using a money order to pay a business, enter the business address here.

Once again, it is critical to write this information properly and in ink. Check to make sure you’ve written the street number and name accurately.

#3. Fill up the Purchaser Information Fields on the Money Order

There are a handful of places where you will enter your details as the purchaser or person who buys the money order.

First, you’ll fill your name, depending on where you buy it, this area on the money order may be labeled “From” or “Purchaser.”

After that, you’ll write down your address. If this information is required, it is usually placed beneath your name.

#4. Finish the Memo Line

You may notice a “Memo” field somewhere on your money order. This is where you’ll write the money order’s purpose.

Assume you’re utilizing a money order to buy a used car from a private seller. You might include a statement in the memo line stating that this is the money of the funds.

If you’re paying a bill, you may put it in the memo line. Include the account number for the bill you’re paying here as well.

#5. Sign the Money Order to complete it.

There should be a “Signature” field somewhere on the money order. Once you’ve finished filling out the remainder of the money order, add your signature here.

This final step before sending it to the receiver is not necessary for USPS postal money orders.

On the back of the money order, you may notice a space for a signature, but that is not for you. After receiving the money order, the payee signs it here.

Tips to Fill Out a Money Order

- When filling out money orders, always use a pen.

- Inquire with the company to which you are sending the money order about how they would want to be addressed on the money order.

- When carrying a big sum of money to acquire a money order, exercise extreme caution and discretion.

- A blank money order is equivalent to cash. Fill it out as soon as possible. You will lose your money if it is lost or stolen.

What to Do After Filling Out a Money Order

After you’ve completed all of the required fields on the money order, go over it again to ensure that all of the information is correct. If you realize you’ve made a mistake, don’t try to fix it yourself.

Instead, show the inaccuracy to the individual or firm from whom you are purchasing the money order. They may be able to repair it for you depending on their rules. If you’ve already paid for the money order, you may have to cancel it and buy a new one.

If you haven’t yet paid for your money order, you must do so before you may send it. To pay for money orders, you usually need cash or a debit card. However, certain money order companies will accept credit card payments.

Aside from the face value of the money order, you must additionally pay any fees imposed by the issuer, which can range from less than a dollar to $5, depending on where you acquire the money order.

Keep your receipt after you’ve paid. This receipt should include a tracking number that you may use to trace the money order and determine when it has been cashed.

Your receipt will also be useful if you need to cancel or replace a money order later because it was lost or stolen. If a money order goes missing and you don’t have the original receipt, you can have a difficult time getting your money back.

How to Send a Money Order

Once you’ve completed all of the fields, make sure to remove the receipt. This stub contains the money order’s official identification number and can be used to trace whether or not the money order was cashed. It also serves as a record of your payment.

You can safely hand-deliver or mail the money order to your receiver now that you have a completed money order and a receipt. It can only be cashed by the recipient.

What Happens If You Don’t Fill Out a Money Order Correctly?

Unfortunately, it is difficult to fix a mistake. For example, if you write the wrong payee name or misspell it, you must request a refund, which may take up to 30 days, according to Western Union.

Money Order Errors to Avoid When Filling Out Your Money Order

Filling up a money order shouldn’t be difficult if you know what information is required and where it should go. However, before completing a money order, keep the following typical blunders in mind:

- Incorrect spelling of the payee’s or recipient’s name

- Inputting the incorrect payee or recipient address

- By leaving the receiver field empty

- Incorrectly writing your name or address

- If you’re using a money order to pay a bill, don’t include an account number in the memo line.

- Failure to sign the money order

- You’ve misplaced your receipt.

Another common blunder is failing to compare money order buying fees before purchasing one. Although money orders are normally inexpensive, certain issuers charge more costs than others.

You should also look at a money order company’s policies for canceling or replacing a lost or stolen money order. Ideally, you should not have to worry about losing or having a money order stolen. But, if either scenario occurs, it’s useful to know ahead of time what you’ll need to do to fix the matter and get your money back.

What is the Procedure for Canceling a Money Order?

If you misplace a money order, you can cancel it with the service provider who issued it. Contact them with details about your money order and follow their cancellation processes. You must normally fill out a cancellation form and pay a charge before you can get a replacement money order or a cash refund.

The Advantages of Money Orders

Money orders are a secure method of payment for buyers. You can send a document that can be tracked and cashed only by the intended recipient. Money orders, as opposed to checks, allow you to keep certain information secret, such as your bank account number. They’re also beneficial for transactions that don’t accept checks.

If you need to purchase and fill out a money order, you can do so at a variety of locations, including the post office, financial services firms such as Western Union, retail establishments such as Walmart, or a traditional bank. Most merchants sell these for under a buck, but you’ll have to pay a little more if you go to your bank or credit union.

Money orders are typically a secure means of payment for merchants. Buyers must pay for a money order with cash or a cash equivalent, so it will not bounce like a personal check.

Some credit card companies will let you pay for a money order with a credit card, but they will classify the transaction as a cash advance and charge you cash-advance fees and high interest.

Disadvantages of Money Orders

Until recently, money orders were a popular and low-cost payment method. New fintech payment alternatives, such as Zelle and Venmo, have developed, though. These alternatives to money orders are less expensive, simpler, and faster. As a result, you might want to look into alternative modes of payment. Due to amount constraints and issuing fees, large transactions may necessitate the usage of multiple money orders. A cashier’s check might be a better option in this situation.

Similarly, money orders are not a replacement for a conventional bank account that allows you to write cheques or use a debit card. Money orders, unlike check or debit card purchases, require you to pay a fee each time you make a payment, making them less economical for frequent transactions.

Similarly, money orders are occasionally counterfeit and used in typical internet scams, so make sure you fill them out correctly and that any monies you receive clear your bank before spending them.

Alternatives to Money Orders: Other Methods of order

A money order is a safe and secure way to send money, but it is not the only option to pay people or businesses.

You could, for example, always pay in cash. However, while paying with cash may seem like a natural decision, it is not always a viable option. Furthermore, paying with cash does not leave a paper trail in the same way that paying with a money order does.

If you want to use a payment method other than money orders and have a bank account, you can do so by:

- ACH Transfer

- Wire Transfer

- Personal Checks

- Cashier Check

- Certified Check

Each of these choices provides a safe method of making payments. The main distinctions between them are in terms of price and speed.

ACH Transfer

An ACH transfer allows you to electronically move money from one bank account to another. If you need to pay your mortgage, for example, you may use an ACH transfer from your bank.

Although ACH transfers are free, they can take several working days to process. A wire transfer, on the other hand, takes only a few hours to complete. The price for that convenience, though, is usually a fee paid to your bank.

Certified checks and Cashier’s checks

Cashier’s checks and certified checks are two types of official checks that you can obtain through your bank account. A cashier’s check is drawn on the account of the bank, whereas a certified check is drawn directly from your account. However, either one can be used in place of a standard personal check, albeit your bank may charge a modest fee to issue one.

Apps that allow people to pay each other

Paying bills and sending money from your bank account using person-to-person payment applications eliminates the need to write cheques. You can load money into a prepaid debit card, which you can then use to pay bills. If you do not have a typical bank account, you should think about it.

Replacing Money Orders That Have Been Lost, Stolen, or Damaged

Money Orders that have been misplaced or stolen

Postal money orders cannot be stopped, however a lost or stolen money order can be replaced.

- It may take up to 30 days to confirm a money order loss or theft.

- It may take up to 60 days to investigate if a money order has been misplaced or stolen.

- A $6.95 processing fee is charged to replace a lost or stolen money order.

Related Check Cashing Services and Stores: How They Work

Obtaining a Refund

- Bring your money order receipt to any Post Office.

- To begin a Money Order Inquiry, speak with a shop employee at the counter.

- After commencing the inquiry, you can check the status of your money order and the progress of your investigation by accessing the Money Orders Application.

- We will send you a replacement money order if your money order is verified to be lost or stolen.

What should I do if I have questions or concerns about my money order?

If you have questions or concerns about your money order, you should contact the issuing company or the financial institution where you purchased it. They will be able to provide you with more information and assistance.

Is there a limit to the number of money orders I can purchase at one time?

It depends on the issuing company or financial institution. Some may have a limit on the number of money orders you can purchase at one time, while others may not. You should check with the issuing company or financial institution for more information.

Can I cash a money order at any bank or financial institution?

Not all banks and financial institutions will cash money orders. It is best to check with the institution you plan to use to see if they will cash your money order. Some institutions may charge a fee for cashing a money order.

What happens if a money order bounces or is rejected?

If a money order bounces or is rejected, it means that it was not able to be processed due to insufficient funds or because it was filled out incorrectly. If this occurs, you may need to purchase a new money order and try again.

What should I do if my money order is lost or stolen?

If your money order is lost or stolen, you should report it to the issuing company or financial institution as soon as possible. They may be able to issue a replacement or refund, but this will depend on the company’s policy.

How long is a money order valid for?

The length of time a money order is valid for will vary depending on the issuing company or financial institution. Some money orders may be valid for up to a year, while others may have a shorter time frame. It is best to check with the issuing company or financial institution for more information.

Conclusion

Money orders can be a convenient way to transfer and receive money. They are a widely accepted method of payment, never expire, and can easily be replaced if lost or stolen. Furthermore, because money orders are prepaid, unlike checks, they will not bounce, making them a safe way to make purchases, pay debts, or send money through the mail.

Knowing how to obtain and use money orders helps you to add this solid instrument to your financial toolbox.

How to Fill Out a Money Order FAQ’s

What is the limit for a money order?

Money orders are usually limited to $1,000. Some establishments may limit them to smaller amounts. If you need to buy many money orders to get around the limit, you might be better off buying a cashier’s check for the entire amount.

Can I do money orders online?

Money orders are now available online, however, they differ from those purchased in person.

Do money orders clear immediately?

To count for that business day, money order must be deposited with a teller at a bank or an ATM before 10:00 p.m. local time. The cash would be available for withdrawals the following business day, as well as to paychecks and purchases that post to your account the following night.

How do I overnight a money order?

Request an overnight mail envelope from a postal clerk. Fill out the envelope’s address. Place the money order inside the envelope. On the overnight postal parcel, request insurance, and delivery confirmation.

- How do Money Orders Work? (+How to Buy with Debit Cards)

- PAYMENT DATE: 2023 Dividend, SSI stimulus & SSA Stimulus Dates (Updated)

- Can you Buy a Money Order with a Credit Card? (Pros & Cons)

- Sales Order Automation Process Steps (+ Free Sales Order Form Template)

- How To Start Trading: Best Easy 2023 Guide & Practices (+Quick Tips)