Lenders are often faced with the challenge of trusting borrowers to clear their debts on time. However, the 5 Cs of credit have become a helpful tool in overcoming these challenges. The lender can use the 5Cs of the credit system to test the creditworthiness of potential borrowers. What are the 5 Cs of credit, and why are they important in credit analysis? We’ll find out in this article. A PDF is also attached to show how lenders rank the 5 Cs of credit.

What Are The 5Cs of Credit?

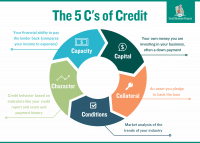

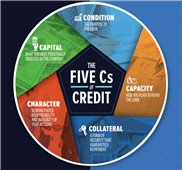

The 5 Cs of credit are character, capacity, capital, collateral, and conditions. This system when used weighs the 5 attributes of a borrower and determines whether the borrower is eligible for a loan or not. These components help the lender understand the owner and the business and determine creditworthiness. Knowing each of the 5 Cs of credit gives a better understanding of what the borrower needs and how to prepare for the loan application process.

The Lender may look at a borrower’s credit reports, credit scores, income statements, and other documents relevant to the borrower’s financial situation. Thus, the lender can make decisions based on the findings. Furthermore, they also consider information about the loan itself, as it also determines the creditworthiness of the borrower. We’ll study these 5 Cs individually in the next section, including their roles in credit analysis.

Read Also:ONLINE LOANS: BEST OPTION TO LOOK OUT FOR (+ HOW TO APPLY GUIDE)

5 Cs of Credit Analysis

Lenders use the 5 CS of credit analysis to determine the risk associated with making a loan. Regardless of the type of financing needed, a bank or lending institution wants to know the applicant’s business and personal financials. Credit analysis is governed by the 5 Cs: character, capacity, condition, capital, and collateral.

The 5 Cs of credit method of evaluating a borrower incorporates both qualitative and quantitative measures. The method of analyzing a borrower’s efficiency is not the same for all lenders. However, the use of the 5 Cs systems is common to all, individuals or organizations alike.

#1. Character

Character is one of the 5 Cs of credit. Lenders need to know the borrower and guarantors are trustworthy. Furthermore, the lender needs assurance that the applicant is capable and has all the required education to successfully run the business. Consequently, lending institutions may require a certain degree of experience in management. Other factors that the lenders consider include the credit history of the applicant, and whether or not the borrower has a criminal record.

The lender is equally interested in the borrower’s track record for paying debts. That’s why the first C is also referred to as credit history. They examine the credit reports of the borrower, which contain information about how prompt the borrower has been in repaying debts in the past. This helps the lender to evaluate the borrower’s credit risk.

#2. Capacity

This is the second of the 5 Cs of credit. You can also refer to it as cash flow. The lender examines the cash flow of the borrower. This cash flow determines whether the business is able to repay the loan within the stipulated time. The cash flow should be sufficient to support business expenses and debts and also provide salaries enough to cater for personal needs.

Capacity measures the borrower’s ability to repay a loan by comparing income against recurring debts and assessing the borrower’s debt-to-income (DTI) ratio. Lenders calculate DTI by adding together a borrower’s total monthly debt payments and dividing that by the borrower’s gross monthly income. Applicants with lower DTIs stand a better chance to qualify for a new loan. Lenders differ in their preferences for approving a loan, although most will prefer applicants with a DTI of about 35% or less. Also, lenders are sometimes prohibited from approving loans for customers with higher DTIs. Some loans require a specific level of DTI of the applicants before they can be approved. For example, qualifying for a new mortgage will require the borrower to have a DTI of 43% or less. This is to ensure that he can comfortably afford the monthly payments for the new loan.

#3. Capital

This is another member of the 5 Cs of credit. It is the amount that the loan applicant is willing to invest in his business. Lenders also want to know the applicant’s personal investment in the proposed business. They will want to know that the applicant is willing to contribute personal assets to make the business grow. This indicates the willingness of the applicant to take personal risks to ensure the growth of the business. In fact, a large contribution by the borrower indicates the applicant’s level of seriousness, thus increasing his chances of qualifying for a loan. For example, an applicant who can put a down payment on a home relatively finds it easier to receive a mortgage. He also avoids the requirement to purchase additional private mortgage insurance (PMI).

#4. Collateral

Collaterals are assets that the applicant of a loan presents to serve as a secondary source of payment. They help the applicants to secure loans as it assures the lender of recovering his loan if the borrower defaults on his loan. In most cases, the object of the loan application often determines what the collateral will be. For example, homes serve as collateral for mortgages, while cars serve as collateral for auto loans.

Loans that are backed by collaterals are often referred to as secured loans or secured debts. They are often issued with lower interest rates and better terms, in contrast to unsecured loans.

#5. Conditions

Another member of the 5 cs of credit is the condition. The lender needs to understand the condition of the business, and the economy. He wants to know how the business will be affected by conditions outside the applicant’s control. Such conditions include the state of the economy, legislative changes, and industry trends. The lender also examines the intention of the applicant for borrowing. Lenders tend to approve loans that define a specific purpose more than the less specific ones. Additionally, the lender wants to know that the loan will be recovered in due time, given the working conditions of the business.

Why Are the 5 Cs of Credit important?

Lenders use 5 Cs analyses to decide whether a loan applicant is eligible for credit and to determine related interest rates and credit limits. They also help determine the riskiness of a borrower or the likelihood that the loan’s principal and interest will be repaid in a full and timely manner.

5 Cs of Credit PDF

There are pdf copies that show how banks and lending institutions rank the 5 Cs of credit in the loan applications. You can download one here.

Which of the 5 Cs is the most Important?

A focus on any one of the five Cs would be a mistake because they all matter. Depending on the circumstances, certain lenders may be given more credit for certain categories.

A lender’s decision on whether or not to extend credit is often based on the applicant’s character and financial ability. Financial institutions typically evaluate these two factors when making loans based on debt-to-income (DTI) ratios, maximum household incomes, minimum credit scores, and other criteria. The size of the down payment and the amount of collateral offered will both affect the terms of the loan, but they are typically not the deciding factors.

Which of the 5 Cs refers to an Individual’s Credit History?

A borrower’s “character” is a composite of their financial background and current status. A borrower’s character is comprised of their payment history, credit score, credit history, and their relationship with previous creditors.

Conclusion

Understanding the 5 Cs of credit is critical to your ability to access credit and do it at the lowest cost. we already know what the 5 Cs of credit are. Delinquency in just one area can dramatically affect the credit you get. If you find that your bank denies you access to credit or only offers it to you at high rates, you can use your knowledge of the Five Cs to do something about it. Work on improving your credit score, save up for a larger down payment or pay off some of your outstanding debt. Also, make sure you have a useful asset that can serve as collateral as this will also increase the chances that they’ll approve your loan.

People also ask whether there is the 6th C of credit. Well, we most times refer to the credit report as the 6th C. Note that banks in all parts of the world have different criteria for ranking the 5 Cs. You can source for pdf copies that show how different banks rank the 5 Cs for credit applications.

- CONSUMER CREDIT: Meaning, Types, Pros, and Cons

- ONLINE LOANS: BEST OPTION TO LOOK OUT FOR (+ HOW TO APPLY GUIDE)

- WHAT ARE HARD MONEY LOANS, Example, Rates & How-to Guide

- HARD MONEY LENDERS: Best Hard Money Lenders For The First Time Investors (Updated)

- Charter Account: Best Easy Guide to Get Started (+ free course)