What runs through your mind when thinking of an irrevocable trust to transfer assets to your beneficiary. A Qualified Personal Residence Trust(QPRT) is a type of irrevocable living trust you can depend on. It is designed to reduce the amount of gift and estate tax. Oftentimes, one incurs these taxes when transferring an asset to a beneficiary. This article is a quick tool to QPRT trust, rules, sales of residence, and unwinding a QPRT.

What is Qualified Personal Residence Trust(QPRT)?

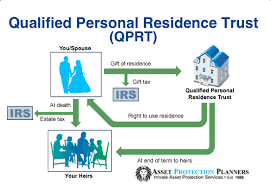

A Qualified Personal Residence Trust (QPRT) is an irrevocable trust that allows a creator to remove a personal home from their estate for the purpose of reducing gift tax rate incurred when transferring assets to their beneficiaries.

It also allows the owner of the residence to remain living on the property for a period of time with a retained interest. In this case, once the stipulated period is over, the interest remaining is transferred to the beneficiaries as a remainder interest. However, the asset protection in this trust comes into effect partially because it is an irrevocable trust. Therefore, as a trust of this nature, it can protect the assets therein that it passes down to your beneficiaries.

See Also: Grantors Trust: A Simple definitive guide (Updated!)

In other words, an irrevocable trust is basically transferred out of the grantor’s estate and into a trust, which effectively owns that property. This is to ensure that the property is passed down to family members at the time of death. In this case, a gift tax may be levied on the property’s value at the time it was transferred into the trust.

Basically, the major property you can only transfer to the trust is your primary residence and sometimes the secondary residence. Meanwhile, you cannot transfer Investment or rental property. One important thing you should take into consideration when using this technique is that you will need to discontinue all rental activity prior to transferring the residence to the trust

Read Also: REVOCABLE TRUST: What is Living Revocable Trust?

How Can One Set Up a QPRT?

- Write the Irrevocable Trust Agreement

- Fund the Trust With Your Residence

- Obtain an Appraisal of Your Residence for Gift Tax Purposes

- Report Your Gift to the IRS

What are QPRT Trust Rules?

You can agree with me that Rules are a set of instructions that tell you what you are allowed to do and what you are not to do. Therefore in a Complete Qualified Personal Residence Trust(QPRT), there are also some rules governing a grantor.

- The QPRT grantor rules sketch out certain requirements when an irrevocable trust can hold some of the corresponding strategies as a revocable trust by the IRS. Certain circumstances lead to the creation of what is known as intentionally defective grantor trusts.

- In such circumstances, a grantor is answerable for paying taxes on the trust income although the trust assets are not included in the owner’s estate. Therefore, such assets would only apply to a grantor’s estate if the individual runs a revocable trust. This is because the individual would definitely own property kept in the trust.

- Grantor trust rules also state that trust becomes a grantor trust if the creator of the trust has a reversionary percentage greater than 5% of trust assets at the time of transferring the assets to the trust.

Other QPRT rules outlined by the IRS are as follows:

- Power to add or change the beneficiary of a trust

- The capability to borrow from the trust without sufficient security

- The power to use the benefits from the trust to finance life insurance premiums

- Power to make changes to the trust’s creation by interchanging assets of equivalent value

Moreover, there are lots of Benefits in a QPRT Trust. They include:

- Ability to change benefits residence

- Estate Tax Benefits

- Lifetime use of home

- Asset Protection from lawsuits

- Gift Tax Benefits

Unwinding a QPRT

If the QPRT terminates, you will have to give the remainder heirs a fair market rent. These returns will reduce your estate. Moreover, if you still wish to unwind the QPRT, there are feasible alternatives that you may confront such as Living in the house rent-free which will cause the inclusion of estate tax. Also, the remainder interest holders will have to allow their interests back to you

Furthermore, the capacity to unwind a QPRT depends on the state law as well as the case law. Consequently Unwinding a QPRT should have no income tax upshots. (Unless the trust is a non-grantor in the sale of its assets to the grantor.) Although may have gift and estate tax outcomes. However, the above-mentioned tax outcomes, in turn, depend on the nature of the trust as well as the nature of the reform.

How Do You Calculate QPRT?

The program evaluates the grantor’s retained interest and uses that figure to derive the value (income interest plus reversion). Next, the grantor’s retained interest is deducted from the trust’s initial capital contribution. The resulting amount is the QPRT that is subject to taxation.

What Is QPRT Sale of Residence?

A QPRT is also planned to be a grantor trust therefore it essentially means that the trust will be

ignored for income tax purposes. Therefore, the grantor can still subtract all real property tax

payments on the residence in the QPRT on his or her personal income tax returns as far as the

QPRT owns the residence.

In addition, If the property is sold after the term of the QPRT has lapsed, even though the grantor may be leasing the property, the capital gain will not be taxed to the grantor. Rather to the persons who acquired the property when the QPRT ended. Also if there be sales of residence in QPRT, the capital gains tax might be more expensive than if the grantor had owned the residence at his or her demise.

Although, you can also sell the residence in the trust at any time. The sale profits are not reinvested in a new residence in two years. These funds are kept as a Grantor Retained Annuity Trust (GRAT). For example, if you choose to downsize your residence, the sale yields from the residence in QPRT can procure a smaller home and the remainder will be viewed as GRAT.

Conclusion

Finally, Today a general estate planning method is to decrease the size of an estate by transferring a residence to a qualified personal residence trust (QPRT). However, suitably structured QPRT will halt the value of the residence at the time the trust is formed. This results in significant estate tax savings while easing to keep the value of many estates below the $1 million inceptions.

Although reducing estate taxes and required appreciation are strong motives for planning a QPRT. Wishing to implement or create a QPRT consider the prevailing federal interest rate under IRC section 7520 as an important factor to start with.

- LIVING TRUST: Overview, Cost, Templates, Pros & Cons (+Writing Guide)

- REVOCABLE TRUST: A Comprehensive Guide (+ How it Works)

- LIVING TRUST VS WILL: Best option in the US (+Major differences)

- Health Savings Account Rules (HSA Rules) 2022 (Updated!)

- Financial Roulette: Spinning the Wheel or Strategic Investing?

Disclaimer:

Pieces of information contained in this article are not tax or legal advice. Therefore they are not a substitute for such advice. As state and federal laws change often, such, information in this article might not reflect most of the recent changes to the law. We sincerely urge that you consult an accountant or an attorney for legal or tax counsel.