Credit ratings are critical because they reflect the risk involved with purchasing a specific bond. A credit rating of investment-grade bonds suggests a minimal risk of credit default, making it an appealing investment vehicle, particularly for conservative investors.

What Is an Investment Grade?

The quality of a company’s credit is referred to as its investment grade. To be deemed an investment-grade issue, the firm must have a Standard & Poor’s or Moody’s rating of ‘BBB’ or better. Anything less than a ‘BBB’ rating is regarded as a non-investment grade. If the company or bond is rated ‘BB’ or lower, it is considered junk grade, and the likelihood that the company would repay its outstanding debt is considered speculative.

Any purchase or sale of investment-grade bonds, bills, or notes will be accompanied by a credit rating. As the company’s strength and debt load vary, so does its rating. If a firm incurs more debt than it can handle, or if its earnings outlook deteriorates, the company’s rating will suffer. The company’s rating will normally improve if it reduces its debt or finds a means to raise potential earnings.

What Securities Are Classified as Investment Grade?

Government and private fixed income products, such as bonds and notes, are deemed investment grade in finance if they have minimal default risk. Credit rating organizations such as Standard & Poor’s and Moody’s assess investment grades on a relative scale. Such credit ratings represent a borrowing organization’s ability and willingness to repay its debt and are based on a variety of financial and economic characteristics that determine the borrower’s creditworthiness. Investment grade securities have a Standard and Poor’s rating of BBB or above or a Moody’s rating of Baa3 or higher.

Details about Investment Grade Credit Rating

In the case of municipal and corporate bond funds, a fund company’s literature, such as its fund prospectus and independent investment research studies, will state that the fund’s portfolio as a whole has “average credit quality.”

Credit ratings for investment-grade issuers are those that are higher than BBB- or Baa. The credit rating agency determines the actual ratings. Investment-grade credit ratings for Standard & Poor’s include:

- AAA: AA+: AA: AA-

Companies with any credit rating in this category have a strong ability to return their loans; however, those with a AAA rating are at the top of the heap and are believed to have the highest ability to repay loans of all.

Many institutional investors have implemented a strict policy of only investing in investment-grade bonds.

The following ratings are found in the next category down:

- A+: A: A-

Companies with these ratings are thought to be solid entities with strong financial repayment capacities. However, such businesses may face difficulties when the economy deteriorates.

Standard and Poor’s investment-grade credit ratings in the bottom tier are as follows:

- BBB+: BBB: BBB-

Companies with these ratings are typically regarded as “speculative grade” and are significantly more vulnerable to shifting economic conditions than the previous group. Nonetheless, these businesses have a strong ability to repay their debt obligations.

Moody’s defines investment-grade bonds as having the following credit ratings:

- Aaa: Aa1: Aa2: Aa3: A1: A2: A3: Baa1: Baa2: Baa3

The highest-rated Aaa bonds have the lowest credit risk of a company failing to repay creditors. Mid-tier Baa-rated corporations, on the other hand, may still contain speculative components, posing a significant credit risk—particularly those that paid the debt with forecasted future cash flows that did not materialize as planned.

What Is a Non-investment Grade?

Non-investment grade securities have a rating of less than Baa3 or BBB-1. The most well-known variety is high yield, which refers to securities issued by a publicly-traded firm or municipality following a rating drop or other bad occurrence (so-called “distressed”). High yield debt can also be debt that was initially issued at a lower investment grade. High yield bonds have become more extensively used in investor portfolios as a source of additional yield over investment-grade bonds since the 1980s.

Private debt, a new sort of non-investment grade asset, has gained traction. These are loans issued directly to corporations that are not publicly traded. These loans often have higher yields due to the unavailability of funding for these businesses and the illiquidity premium these loans carry. They necessitate extensive basic study and due diligence on the part of the lender, not only due to the increased risk but also due to the sophisticated nature of the loan structure.

What Is the Risk/Reward Profile of Non-Investment Grade?

As previously stated, both high yield and private loans provide a higher yield than other types of investments. Furthermore, through direct origination, private loans might include risk-mitigation aspects. Lenders are able to invest at the top of the company’s capital stack because they offer a source of non-bank investment for enterprises that would not otherwise have access to capital.

This means that the loans, known as senior secured debt, are secured by the company’s assets, and the lender has first priority recourse. This combination of enhanced yield and risk reduction may result in a better return/risk profile.

What Is the Definition of Investment Grade Bonds?

Investment-grade bonds are corporate and government debt that bond rating agencies believe will be repaid in full, plus interest.

Remember that a bond is just debt taken on by a company or government body to fund projects, similar to how you would borrow to buy a house or finance a car. While every debt, whether personal or corporate, is given with the idea that it would be fully repaid, this is not always the case.

That is why credit rating companies such as Fitch, Moody’s, and Standard & Poor’s assess bonds. Investment-grade bonds are assigned ratings of BBB- (Standard & Poor’s and Fitch) or Baa3 (Moody’s). These ratings indicate that investment-grade bonds are less risky and more likely to be repaid. Thus, they are suitable for more conservative portfolios looking for diversification of income.

Junk bonds are at the other end of the rating spectrum. They are risky debt with attractive yields but a higher likelihood that the issuer will fail to repay your investment or meet their interest payment obligations.

Benefits of Investment Grade Bonds

#1. Stocks are less risky.

Because bonds don’t have the same volatility (or price changes) as stocks, the value of your bonds is far more likely to remain constant on a daily basis. In the uncommon event that a firm goes bankrupt, bondholders are paid out before stockholders. Thus, it increases the likelihood that you will receive a full return on your investment.

#2. Creating income.

Income investors and retirees favor investment-grade bonds because they provide a consistent and predictable income source. While certain equities pay dividends, they are not guaranteed, unlike bond interest payments.

#3. Higher returns than other fixed-income options.

Investment-grade bonds often yield more than treasuries or municipal bonds. While interest rates on most bonds are currently low, the longer-term average yield on investment-grade corporate bonds is 2%, compared to 1.3 percent on municipal bonds.

Investment Grade Bonds’ Drawbacks

#1. Lower than stock returns.

Bond yields have historically been lower than the returns available from stocks. If you invest too much of your portfolio in bonds, it may be more difficult to fulfill your retirement or other investment goals. “You won’t be able to stay up with inflation,” says Maggie Gomez, a certified financial planner (CFP) of Money with Maggie.

#2. There is less liquidity.

If you invest directly in bonds rather than through bond funds, you may be unable to liquidate your assets in a pinch. Bonds must normally be held until their maturity date, thus your money will most likely be unavailable for several years. Alternatively, if you can sell your bonds on the secondary market, you may have to sell at a loss.

#3. There is less transparency.

Most corporate bonds are traded over-the-counter (OTC), which means the market has less liquidity as well as less price transparency. This raises the risk that you will pay more than you should. This is why financial consultants recommend that most investors stick to bond funds rather than individual bonds.

Potentially large buy-ins are necessary. Most bonds are issued in $1,000 increments and cannot be purchased in smaller amounts. For those wishing to begin investing in individual bonds, this can result in significant cash requirements.

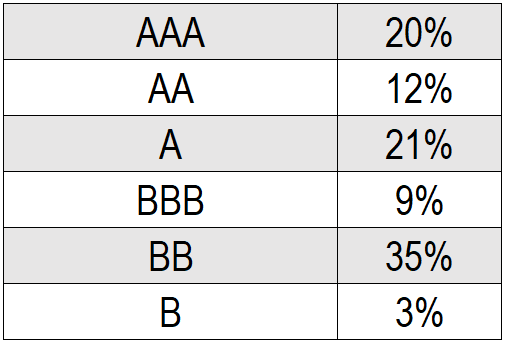

Investment-Grade Bonds Example

An investor is interested in investing in a floating rate fund. His criterion is that the fund’s bonds must have a majority (>50%) of investment-grade bonds. The fund adheres to the S&P credit rating methodology and has the following credit allocation:

Does the floating rate fund meet the requirement of containing a majority of investment-grade bonds?

Bonds rated BBB- or higher in S&P’s credit rating system are considered investment-grade. As a result, the floating rate fund mentioned above has 62 percent of its assets invested in investment-grade bonds. As a result, the floating rate fund meets the investor’s condition.

How to Invest in Investment Grade Bonds

Most people should acquire investment-grade bonds through mutual funds, index funds, or exchange-traded funds (ETFs). It is difficult to navigate the bond market, and making excellent investments in specific investment-grade bond issues necessitates specialist knowledge.

The finest bond funds provide a simple and low-cost option to purchase investment-grade bonds. They are simple to buy in a traditional brokerage account or tax-advantaged retirement plan, generally with no commissions and modest cost ratio fees. Furthermore, bond funds provide quick diversification and are professionally managed. Thus it allows you to avoid many of the dangers of individual bond investing.

If you are dead bent on purchasing individual investment-grade bonds from a government or municipality, you should be able to do so directly from the issuer or the financial institution managing the bond issue. Buying corporate bonds directly from a public firm can be challenging. Also, you’ll almost certainly end up buying them on the secondary market, where pricing can be considerably less transparent.

Which Investment Grade Is the Highest?

Credit rating companies like Standard & Poor’s and Fitch Ratings give an issuer’s bonds the highest possible grade or AAA.

What Does High Grade vs. Investment Grade Mean?

Bonds with solid credit ratings of at least “BBB-” are considered investment-grade bonds, whereas those with ratings below “BBB-” are considered high-yield bonds (also known as speculative or junk bonds).

Which Rating Is Superior, BB or BBB?

According to comparable issuers or obligations in the same nation or monetary union, BBB’ National Ratings indicate a moderate level of default risk.

When compared to other issuers or liabilities in the same nation or monetary union, obligations with BB’ National Ratings have a higher default risk.

What Investment Grade Is A+?

The credit ratings A+ and A1 are created by S&P and Moody’s. The investment-grade ratings of A+ and A1 are in the middle, reflecting some but little credit risk. Investors use credit ratings to assess an issuer’s creditworthiness; higher credit ratings are correlated with lower interest rates.

How Is Investment Grade Determined?

The credit rating agency frequently uses indications like leverage, cash flows, earnings, interest coverage ratio, and other financial parameters to determine the investment grade of a certain instrument.

Final Thoughts

Investment-grade bonds can provide consistent cash flows with little risk, making them an excellent choice for conservative investors, income investors, and retirees wishing to diversify their portfolios.

Investment-grade bonds can also play an essential role in your portfolio, particularly as you approach your goal’s end date and wish to lock in your gains. Prior to that, though, most counselors would advise against investing too heavily in bonds since you risk missing out on stock market gains.

Investment Grade FAQs

What is the difference between investment grade and non-investment grade?

AAA is assigned to the highest quality corporate bonds. The worst-performing bonds are rated D or are already in default. Anything graded BBB or higher is considered an investment grade. Anything graded BB or lower is considered a non-investment grade.

What is S&P investment grade?

Issuers and debt issues that obtain a rating of ‘BBB-‘ or higher on the S&P Global Ratings long-term rating scale are generally regarded as “investment-grade” by regulators and market participants, while those that receive a rating lower than ‘BBB-‘ are often considered “speculative-grade.”

Is BB better than BBB?

Investors should be informed that an agency downgrading a company’s bonds from “BBB” to “BB” reclassifies its debt from investment grade to “junk.” Although this is only a one-step decrease in credit rating, the consequences can be significant.

How do I find my investment-grade rating?

Bonds having ratings of BBB- (on the S&P and Fitch scales) or Baa3 (on the Moody’s scale) or higher is considered “investment-grade.” Bonds with lower ratings are deemed “speculative” and are commonly referred to as “high-yield” or “junk” bonds.