An amortization schedule is a very significant tool in the business world. This is because it helps businesses and investors to understand and forecast their costs over time. However, in this article, more details shall unfold as we highlight amortization calculations, loans and a mortgage calculator.

Amortization Schedule

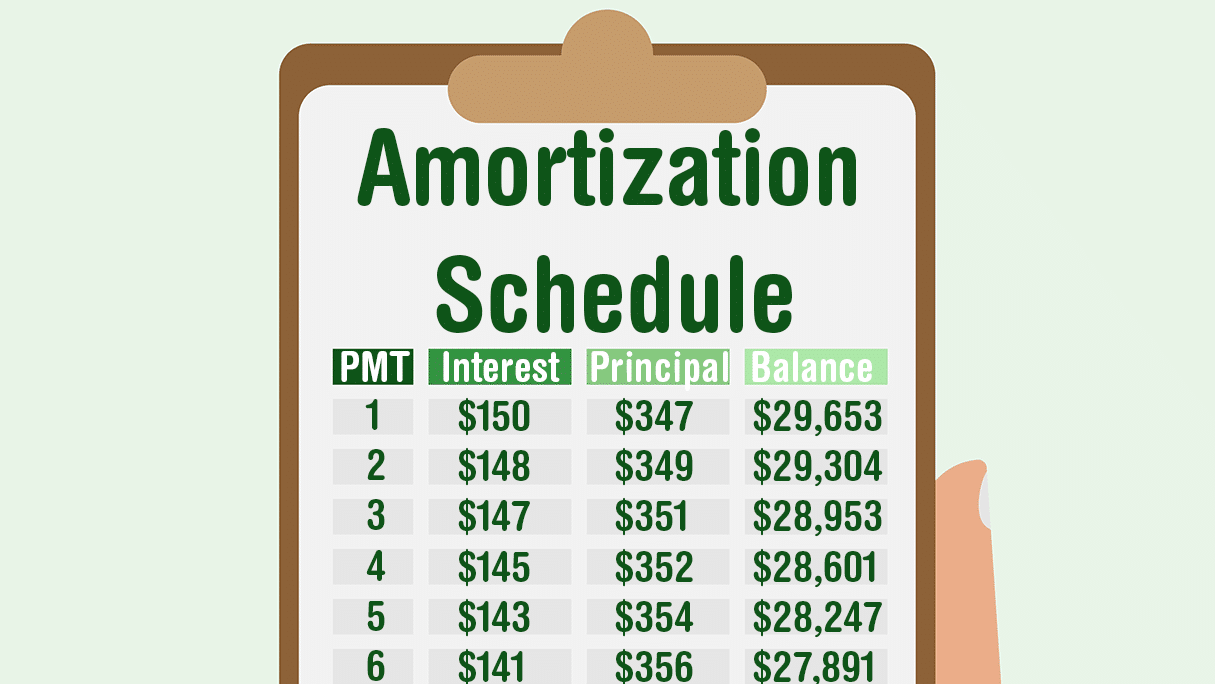

An amortization schedule is a periodic table describing each payment on an amortizing loan (typically a mortgage), as generated by an amortization calculator. In other words, simply put that amortization refers to the process of paying off a debt over time through regular payments. Any part or portion of each payment is for interest while the remaining amount is applied towards the principal balance. Using an amortization schedule, borrowers can track their dept and how it will be repaid.

Methods for Amortization Schedule

There are various ways to amortize a loan. They include:

#1. Straight line

A straight-line amortization, also known as linear amortization. It occurs when the total interest amount is spread evenly over the lifetime of a loan.

#2. Declining balance

The declining-balance is an accelerated method of amortization where the periodic interest payment falls, but the principal repayment increases with the term of the loan.

#3. Annuity

An amortized loan in the annuity method comprises a series of payments made between equal time intervals. Although, there are two types of annuity namely;

- The ordinary annuity: Here, payments are made at the end of each period.

- The annuity due makes payments at the beginning of each period.

#4. Bullet

Ordinarily, the periodic payments of a bullet loan cover the interest charges only. It leaves a huge amount of the last payment at the matured loan that repays the principal.

Read Also: Zillow Mortgage Calculator: How Accurate is Zillow Mortgage Calculator? (+ Quick Tips)

Amortization Calculations

Amortization calculation formular can be somewhat confusing

Moreover, If you know the payment amount, it is pretty straightforward to create an amortization schedule calculations. The example below shows the first 3 and last 3 payments for the above example. Each line shows the total payment amount as well as how much interest and principal you are paying. Notice how much more interest you pay in the beginning than at the end of the loan!

1. An Interest portion of the payment is calculated as the rate (r) by the previous balance.

2. The Principal portion of the payment is calculated as Amount minus(-) Interest. Then sum new Balance bt by subtracting the Principal from the previous balance.

3. The last payment amount may need to be adjusted to account for the rounding or approximation

Loan Amortization

Loan amortization is the gradual reduction of a debt over a given period. It requires the borrower to make planned, periodic payments that are applicable to both the principal and interest. An amortized loan payment first pays off the interest expense for the period.

The easiest way to calculate payments on an amortized loan is to use a loan amortization calculator or table template. However, you can calculate minimum payments by hand using just the loan amount, interest rate and loan term.

However, lenders often use amortization tables to calculate monthly payments and summarize loan repayment details for borrowers. In addition, amortization tables enable borrowers to determine how much debt they can afford. It also evaluates how much they can save by making additional payments and then calculate annual interest for tax plans.

How Loan Amortization Works

Loan amortization breaks a loan balance into a schedule of equal repayments based on a specific loan amount, loan term and interest rate. This loan amortization schedule lets borrowers see how much interest and principal they will pay as part of each monthly payment—as well as the outstanding balance after each payment.

A loan amortization table can also help borrowers:

- Calculate how much total interest they can save by making additional payments

- Reverse engineer a loan payment to determine how much financing they can afford

- Calculate the total amount of interest paid in a year for tax purposes (this applies to mortgages, student loans and other loans with tax-deductible interest)

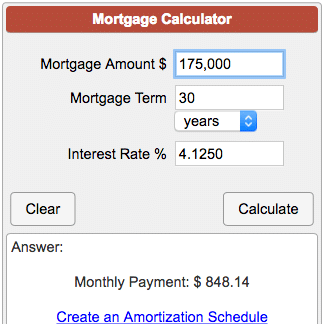

Mortgage Calculator Amortization

Below is an example of an mortgage calculator amortization

Calculator Use

Calculate your monthly mortgage payments on your home based on the term of your mortgage, interest rate, and mortgage loan amount. To include annual insurance and taxes in your calculations, use this mortgage calculator with taxes and insurance.

Mortgage Amount: The original principal amount of your mortgage when calculating a new mortgage or the current principal owed when calculating a current mortgage.

Mortgage Term: The original term of your mortgage or the time left when calculating a current mortgage.

Interest Rate: The annual nominal interest rate or stated rate on the loan. Note that this is the interest rate you are being charged which is different and normally lower than the Annual Percentage Rate (APR).

Monthly Payment: The monthly payment amount to be paid on this mortgage on a monthly basis toward principal and interest only. This does not include insurance or taxes or escrow payments. (payment = principal + interest)

Monthly Payment Calculation

Monthly mortgage payments are calculated using the following formula:PMT=PVi(1+i)n(1+i)n−1PMT=PVi(1+i)n(1+i)n−1

where n = is the term in number of months, PMT = monthly payment, i = monthly interest rate as a decimal (interest rate per year divided by 100 divided by 12), and PV = mortgage amount (present value).

Source: Calculator Soup

Conclusion

An amortization schedule usually shows much interest and principal when you are paying each period. Meanwhile, considering the monthly payment, you should consider the term of the loan. Have it in mind that the longer you stretch out the loan, the more interest you’ll end up paying in the end. Therefore you must make a trade-off between the monthly payment and the sum amount of interest.

Related Articles: