A strong borrowing power makes life easier. Your ability to attain significant milestones like renting a house, purchasing a vehicle, or obtaining a mortgage for your first house is significantly influenced by this three-digit figure, which touches almost every aspect of your financial life.

A very high borrowing power of 700 or more is needed for the majority of credit cards. Additionally, credit scores of 750 or above are often required for cards with several advantages, such as cashback and travel incentives. However, if you apply for the correct credit card, you might still get approved for one even with lower borrowing power.

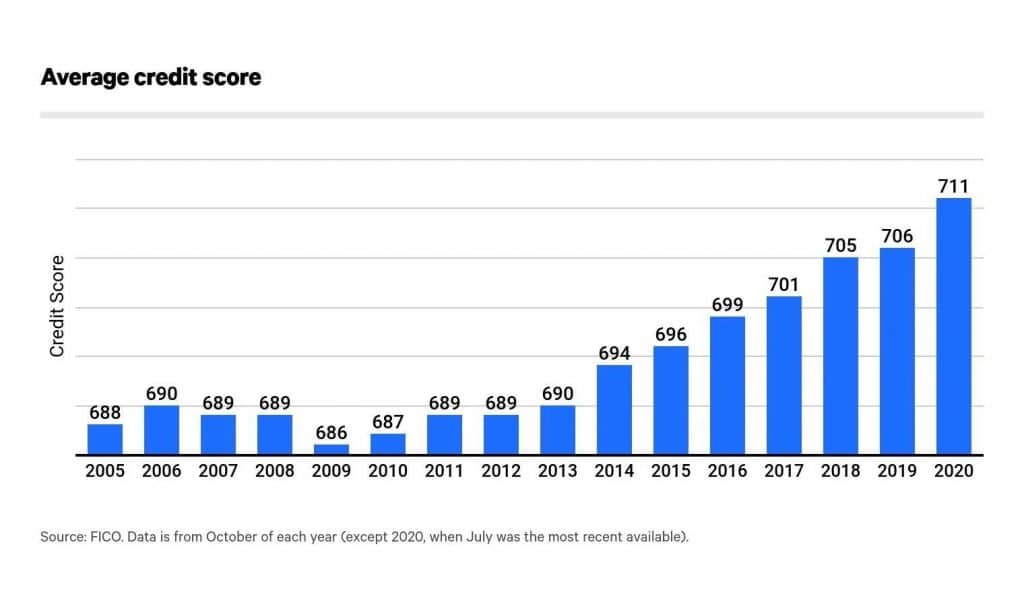

Ranges of Credit Scores

Before we go into the details, let’s quickly review the FICO (Fair Isaac Corporation) credit score range:

Deficient: 300 to 579

Fair: 580 to 669

Good: 670 to 739

Excellent: 740 to 799

Outstanding: 800 to 850

As a result, FICO ratings vary from 300 to 850. At this point, it’s crucial to keep in mind that the better alternatives you have available to you, the higher your credit score is.

Why is Having a Good Credit Score Crucial?

Lending institutions, whether for a vehicle, a house, or anything else, want to see that you are creditworthy and can be trusted to repay their money on time before they decide to provide you with the loan. To determine whether to accept your loan and how much to offer you, they may consider your credit record and borrowing power. Because of this, it’s crucial to maintain the best credit score possible.

You must pay your bills on time and not be late with your dues. It is also better not to think about online loans, like a “quick 500 dollar loan“, because they have high-interest rates and you can not calculate your finances to pay off the debt, which will ruin your rating.

Borrowing Power for a Bank Card

A credit card is available for almost everyone, regardless of credit score. However, the cards offered to customers with lesser credit scores won’t have the greatest rates or conditions.

Cards for Those With Good to Average Credit

A decent FICO borrowing power is between 580 and 670, and if you fit this description, you may select from a variety of reliable bank cards.

This is a wonderful choice for anyone trying to improve their creditworthiness while simultaneously collecting cash rewards on a rewards plastic that needs a borrowing power between 580 and 740.

An alternative is a secured bank card. Secured cards have the same appearance and functionality as regular cards, but the spending limit must be “secured” with your funds. Your security deposit will be maintained in an FDIC account insured for your protection. However, you will forfeit your warranty if you don’t pay.

Credit Cards for Outstanding to Decent Credit

If your borrowing power is in the good (670 – 799) to exceptional (800+) range, you should be able to be approved for a bank card that gives you rewards for your purchases. Do your homework before applying for a rewards card since not all reward cards (or issuers) have the same credit criteria.

Minimum Credit Score Required for a Credit Card

You may get approved for a bank card regardless of your loan history. Of course, the plastic card provider could be concerned given that you’ve previously made late payments. Even if they aren’t precisely what you’re looking for, choices do exist.

Depending on the card, a high borrowing power often comes with several benefits. If your score is excellent, you have several bank cards to pick from with exceptional deals.

When Will Your Credit Score Start To Improve?

Your borrowing power may increase by any amount—no minimum, maximum, or average — each month. Likewise, no activity will always result in a certain number of points. The precise reasons why your borrowing power is poor will determine how long it takes to improve. Your borrowing power might rise significantly in a single month if the main factors affecting it — debt utilization — are eliminated. It will take many months of on-time payments to observe any improvement in your borrowing power if it is low due to numerous collections and shady payment history.

Credit Score Boosting Advice

Try the following if you need to raise your terrible borrowing power to qualify for a rewards card or a low-interest loan:

#1. Avoid Exceeding Your Debt Limit

Your borrowing power may suffer if you go above your loan limit. Because of this, spending more than 30% of your available credit on all accounts might be considered using more than just one card’s limit. Don’t allow your credit card debt to spiral out of hand by keeping credit limits within the specified range.

#2. Become a Licensed User

Adding yourself as an authorized user on someone else’s loan card is a wise move if you want to improve your debt. It might be low-risk and gives you the chance to raise or enhance your borrowing power.

#3. Apply for Fewer Cards

If the suggestions mentioned above don’t help you, are you still considering how to raise your borrowing power?

Avoid applying for too many different cards when searching for new plastic money. Do your homework and only apply for bank cards that you have a good chance of being accepted for since applying for too many cards at once will damage your borrowing power over time.

Conclusion

The good news is that there are easy measures you can take to raise and maintain your credit score despite the significant influence it may have on your life. There is little ambiguity about what your score represents and how it is determined, and loan bureaus and card issuers have made it simpler than ever for you to check your score often so you can know where you stand.

There are simple actions you may follow to raise your score if it is poor or fair. Though not always simple, the procedure is manageable. Additionally, there is a significant payout, including stronger rewards programs and reduced APRs, which makes the effort much more valuable.