Since the start of the financial crisis in 2008, top management and valuation practitioners alike have seen significant changes in the underlying parameters that drive and are used to derive the value of companies. The market risk premium is one of these important indicators. We’ll discuss the market risk premium in detail in the article. We’ll discover more about the current market risk premium in this article.

This is the increased return an investor will earn (or expects to receive) from holding a risky market portfolio rather than risk-free assets.

The market risk premium is a component of the Capital Asset Pricing Model (CAPM), which analysts and investors use to determine the acceptable rate of return on investment. The concepts of risk (volatility of returns) and reward are central to the CAPM (rate of returns). Investors always desire to have the highest possible rate of return mixed with the lowest possible volatility of returns.

CAPM formula = Risk-Free Rate of Return + Beta * (Market Rate of Return – Risk-free Rate of Return)

Market Risk Premium Formula = Market Rate of Return – Risk-Free Rate of Return

The difference between the projected return on investment and the risk-free rate is referred to as the market risk premium.

To comprehend this, we must first examine a simple notion. We’ve all heard that higher risk equals higher reward. So, why wouldn’t that be true for investors who have made the mental shift from savers to investors? When a person invests in Treasury bonds, he expects a minimal return. He does not want to take any additional risks, so he receives the minimum rate. But, if a person is willing to invest in a stock, shouldn’t he expect a higher return? At the very least, he would anticipate more than what he would get if he invested his money in Treasury bonds!

That is where the concept of market risk premium comes into play. This is the difference between the expected rate of return and the minimal rate of return (also known as the risk-free rate).

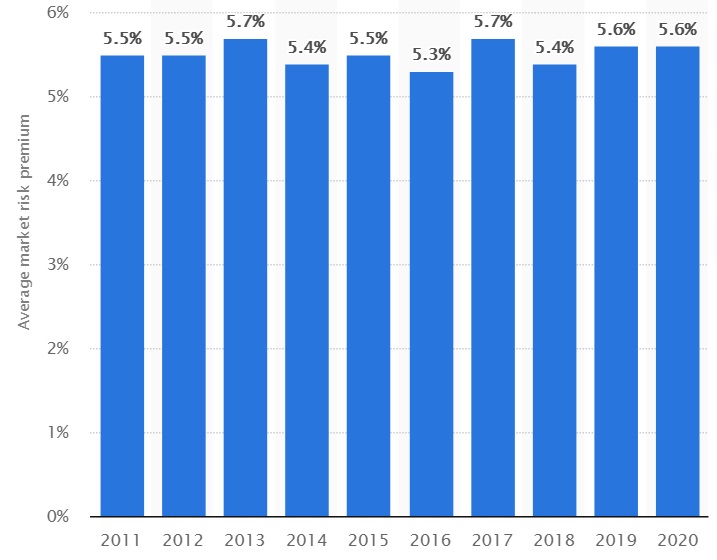

In 2020, the average market risk premium in the United States was 5.6 percent. This means that investors expect a little better return on their investments in that country in exchange for the risk they face. Since 2011, the premium has been between 5.3 and 5.7 percent.

What causes Country-specific risk?

There are two major sources of risk in investments. First, inflation reduces the real value of an asset. After one year, a $100 investment with 3% inflation is worth only $97. Investors are also concerned about the dangers of project failure or non-performing loans.

Analysts have traditionally considered the US Treasury to be risk-free. This viewpoint has shifted, but many advisors continue to use treasury yield rates as risk-free rates. Given that US government assets are accessible in a variety of terms, investment managers have a choice of methods for forecasting future market events.

The Market risk premium formula is straightforward, but there are some details to consider.

Market Risk Premium Formula = Expected Return – Risk-Free Rate

Let us now examine each component of the market risk premium formula.

First, consider the estimated return. This predicted return is entirely reliant on how an investor thinks. And what kind of investments does he make?

From the perspective of the investors, we have the following possibilities —

#1. Risk-tolerant investors:

These are investors who understand the market’s ups and downs and are willing to take whatever risks are necessary. Risk-tolerant investors will not expect much from their investments, thus the premiums will be substantially lower than for risk-averse investors.

#2. Risk-averse investors:

These are usually new investors who haven’t put much money into risky investments. They have saved money in fixed deposits or savings bank accounts. After considering their investment options, they begin to invest in stocks. As a result, they anticipate a considerably higher return than risk-averse investors. As a result, the premium is bigger in the case of risk-averse investors.

Now, the premium is also determined by the type of investments in which the investors are willing to invest. If the investments are too risky, the expected return will be much higher than for less risky investments. As a result, the premium would be higher than that of less risky investments.

There are two other factors to consider when calculating the premium.

The required premium is the difference between the minimum rate that investors can expect from any type of investment and the risk-free rate.

This is the difference between the historical market rate of a specific market, such as the NYSE (New York Stock Exchange), and the risk-free rate.

Interpretation

The market risk premium model is an expectancy model because both of its components (expected return and risk-free rate) are subject to change and are influenced by volatile market forces.

To fully grasp it, you must first understand the basis for computing the expected return in order to calculate the market premium. And the foundation you select should be relevant to and consistent with the investments you have made.

In most cases, all you need to do is look for historical averages to use as a guideline. If you invest in the NYSE and want to calculate market risk premium, all you have to do is look up the past performance of the stocks you want to invest in. Then calculate the averages. Then you’d have a figure to work with. One thing to keep in mind is that by using historical figures as a basis, you are assuming that the future will be exactly like the past, which may turn out to be incorrect.

What is the correct market risks premium calculation that is not flawed and is in line with the current market condition? Then we need to look for Real Market Premium. Here is the formula for the Real Market Risk Premium.

Real Market Risks Premium = (1 + Nominal Rate / 1 + Inflation Rate) – 1

We will go over everything in detail in the example section.

Let’s begin with a simple one and work our way up to more complex ones.

Let’s take a closer look at the specifics below –

| In percentage | Investment 1 | Investment 2 |

| Expected Return | 10% | 11% |

| Risk-free rate | 4% | 4% |

In this instance, we have two investments and have been given information on the expected return and risk-free rate.

Let’s have a look at how market risk premiums are calculated.

| In percentage | Investment 1 | Investment 2 |

| Expected Return | 10% | 11% |

| (-) Risk-free rate | 4% | 4% |

| Premium | 6% | 7% |

In most circumstances, our assumptions must now be based on the predicted return on historical figures. That is, the rate of premium is determined by what the investors expect as a return.

Let us now consider the second example.

The breadth and conceptualization of market risks premium and equity risk premium differ, but let’s look at the equity risk premium example, as well as equity, which may be regarded as one sort of investment as well.

| In percentage | Investment |

| Large Company Stocks | 11.7% |

| US Treasury Bills | 3.8% |

| Inflation | 3.1% |

Let’s have a look at the equity risk premium now. The equity risk premium is the difference between the projected return and the risk-free rate on specific equity. Assume that investors anticipate earning 11.7 percent on large firm shares and that the yield on US Treasury Bills is 3.8 percent.

As a result, the equity risk premium would be –

| In percentage | Investment |

| Large Company Stocks | 11.7% |

| (-) US Treasury Bills | 3.8% |

| Equity Risk Premium | 7.9% |

What about inflation, though? What would we do if the inflation rate increased? In the next real market risk premium example, we will look at this.

| In percentage | Investment |

| Large Company Stocks | 11.7% |

| US Treasury Bills | 3.8% |

| Inflation | 3.1% |

We all know that it is the expectation model, and when we need to calculate it, we need to look at previous numbers from the same market or for the same investments to get a sense of what to expect as an expected return. Herein lies the significance of genuine premium. We will account for inflation before calculating the true premium.

The real market risk premium formula is as follows–

1 – (1 + Nominal Rate / 1 + Inflation Rate)

First, we must calculate the nominal rate, i.e., the normal premium –

| In percentage | Investment |

| Large Company Stocks | 11.7% |

| (-) US Treasury Bills | 3.8% |

| Premium | 7.9% |

We will now take this premium as a nominal rate and calculate the real market risks premium.

Real Premium = (1 +0.079 / 1 + 0.031) – 1 = 0.0466 = 4.66 %

It is useful for two reasons in particular –

First, in terms of inflation and real-world statistics, the real market premium is more realistic.

Second, there is little to no risk of expectation failure when investors predict a return of 4.66 percent -6 percent.

Because this is an expectancy model, it cannot be accurate most of the time. However, if you are considering investing in stocks, the equity risk premium is a far superior notion (there are many approaches from which we can calculate this). For the time being, let us examine the Concept’s constraints –

- This is not a precise model, and the computation is subject to the investors’ choices. That suggests there are too many variables and not enough foundation for proper computation.

- When calculating market risks premiums using historical numbers, it is expected that the future would be comparable to the past. However, in most circumstances, this is not the case.

- It does not account for the rate of inflation. As a result, the genuine risk premium is a far superior idea to the market premium.

What Does Equity vs. Market Risk Premium Mean?

The excess return anticipated on an index or investment portfolio above the specified risk-free rate is known as the market risk premium. The predicted return of a stock over the risk-free rate, on the other hand, is represented by an equity risk premium, which only applies to stocks.

What Does the CAPM Market Risk Premium Mean?

The difference between the anticipated return on a market portfolio and the risk-free rate is known as the market risk premium (MRP). The slope of the security market line (SML), a graphical representation of the capital asset pricing model, is equal to the market risk premium (CAPM).

What Distinguishes Risk Premium from Market Risk Premium?

The higher return you receive on riskier assets is referred to as the market risk premium. The projected return on an investment that is more than the risk-free rate is referred to as the risk premium, also known as the equity risk premium.

Is It Better to Have a Higher or Lower Market Risk Premium?

An increased premium suggests that you would allocate a larger portion of your portfolio to equities. The expected return on a stock is also connected to the equity premium by the capital asset price. A stock that, according to its beta, is riskier than the overall market should provide returns that are even larger than the equity premium.

In conclusion

The equity risk premium is determined by subtracting the risk-free return from the projected asset return (the model makes a key assumption that current valuation multiples are roughly correct)

The equity risk premium can help investors evaluate stocks by providing some direction, but it attempts to anticipate a stock’s future return based on its past performance. Because projecting future returns is difficult, assumptions about stock returns might be harmful. The equity risk premium is based on the premise that the market will always deliver higher returns than the risk-free rate, which may or may not be correct. The stock risk premium can serve as a guide for investors, but it is a limited instrument.

Does the market risk premium change over time?

“The market premium is not always 6% but varies over time by as much as its mean.

What factors influence market risk premium?

The five main risks that comprise the risk premium are business risk, financial risk, liquidity risk, exchange-rate risk, and country-specific risk. These five risk factors all have the potential to harm returns and, therefore, require that investors are adequately compensated for taking them on. (phentermine)

Does market risk premium include inflation?

When market risk premium calculation is done by taking into account the historical figures, it’s assumed that the future would be similar to the past. But in most cases, that may not be true. It doesn’t take into account the inflation rate. Thus, the real risk premium is a much better concept than a market premium.

Is market risk premium the same as equity risk premium?

The market risk premium is the additional return that’s expected on an index or portfolio of investments above the given risk-free rate. On the other hand, an equity risk premium pertains only to stocks and represents the expected return of stock above the risk-free rate.