As a U.S. citizen with money in accounts abroad, understanding the basics behind FBAR filing is needed to have an easy tax season. It may be surprising to know that if you have money in a foreign account, you have special reporting requirements, known as FBAR. So here we will be going through all you to know about FBAR filling. We are going to look at how and when to file the FBAR. Furthermore, we’ll see the instructions and requirements for filing the FBAR form and also note the FBAR 2023 deadline and penalties attached.

FBAR

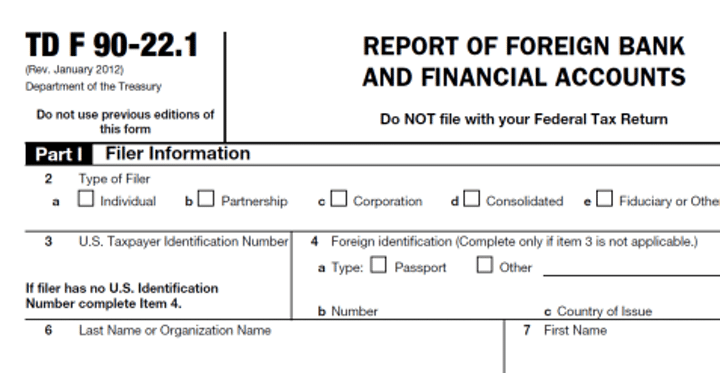

You may have heard or come across FBAR filing, but you don’t know what it’s about. FBAR stands for “Foreign Bank Account Report”. It refers to FinCen Form 114, Report of Foreign Bank and Financial Accounts.

Some taxpayers while trying to avoid paying their taxes, hide their money in accounts overseas. To tackle this issue, the U.S. has come up with ways to keep track of assets belonging to U.S. persons overseas.

The FBAR came into existence as part of the Bank Secrecy Act of 1970 (BSA). It was established to prevent taxpayers from avoiding paying taxes by hiding assets overseas. However, it’s only over the last two decades that the IRS started enforcement of foreign financial account reporting rules for American taxpayers.

The purpose of the report is to inform the IRS of any accounts or other assets you own overseas. On this form, you must report all your foreign financial accounts. Accounts include brokerage accounts, bank accounts, mutual funds, and more.

This law also requires you to keep specific records on each of these accounts throughout the year. If you fail to comply with any of these FBAR requirements, you may face penalties and fines from the IRS.

Under the Bank Secrecy Act, each US person must file an FBAR report if the combined total of your foreign accounts is at least $10,000 during the calendar year. For Instance, you may have $2000 in account A, $5000 in account B, and $9000 in account C. Although none of the accounts is over $10,000, you will have to report the different accounts ABC. This is because the aggregate is over $10,000.

Also, you should note that an FBAR must be filed whether or not the foreign account generates any income.

How to file an FBAR

FBAR filing is not to the Internal Revenue Service, unlike our tax payments. It goes directly to the U.S. Department of Treasury, specifically FinCen instead. Also, you don’t send it by mail with your federal tax return. Rather, it is done electronically with the Financial Crimes Enforcement Network’s BSA E-Filing System.

It is possible to allow another person to file the FBAR on your behalf. However, you must complete FinCEN Report 114a, Record of Authorization to Electronically File FBARs. This form is not sent in with your FBAR filing. Instead, you should keep a copy of it to give to the IRS if necessary. It must be filed electronically through FinCEN’s BSA e-filing system or with a preparation service such as business yield services.

In the case of married taxpayers, in very few situations are you may be able to submit a joint FBAR. If you own accounts jointly with your spouse, and either none or only one of you own a separate account, you are able to file a single report. Else, each spouse must file their own. If you are filing a prior year or an amended form, you must still use FinCEN’s website to do so. But you must file in separate accounts.

FBAR requirements

To report accurately on an FBAR form, you must keep specific records of each of your foreign financial accounts. You should keep these records even after you have filed the FBAR in question. It’s important to keep backup documentation so that you can back up your claims in the event of an audit.

Documents needed for proper FBAR reporting will include;

- The account number

- The name listed on the account

- The type of account

- The name and address of the financial institution

- The maximum value of the account during the year

You can fulfill the FBAR requirements of the law by keeping any document that includes this information. Examples include copies of filed FBARs and bank statements. Be sure to keep the right records for at least five years from the FBAR deadline.

Also, to file the FBAR as an individual, you must personally and/or jointly own a reportable foreign financial account that needs the filing of an FBAR for the reporting year. There is no need to register to file the FBAR as an individual. If you are NOT filing the FBAR as an individual (as in the case of an attorney, CPA, or enrolled agent filing the FBAR on behalf of a client) you must obtain an account to file the FBAR by registering to Become a BSA E-Filer.

Note that if you are filing an FBAR because you have signature authority over an account owned by someone else, you are not responsible for keeping records. Instead, the owner of the account will have to collect and maintain the appropriate documents.

FinCen Form 114 reporting exemptions

Certain people may be exempted from filing an FBAR even if they meet the requirements listed above. For example, if all of your foreign financial accounts are on a consolidated FBAR, you do not need to file an additional FBAR.

Likewise, if all of your foreign financial accounts have joint ownership with a spouse who is already filing an FBAR, you don’t have to file your own copy of the form. But, be sure to complete and sign FinCEN Form 114a to let your spouse file on your behalf. Keep in mind that your spouse can file on your behalf regardless of your filing status. But you cannot file this form jointly if either of you owns a separate foreign account of any value. If any different accounts exist, you must file separate FBARs.

Also, these set of individuals are exempted from the FBAR filing:

- An individual that owns or has signature authority over a bank account in a US military financial institution operated by the United States. This should be for the purpose of servicing US government operations abroad.

- An employee or officer of a bank under the authority of the Comptroller of the Currency, Board of Governors of the Federal Reserve System, Federal Deposit Insurance Corporation, or Office of Thrift Supervision. Also, you should have no personal interest in the bank account.

- You are an employee or officer of a domestic corporation that has equity securities listed on a national securities exchange. Also, you have no personal interest in these securities.

- An employee of a domestic corporation that has assets that exceed $10M and more than 500 shareholders. You should have no personal interest in these assets.

The FBAR form

The online FBAR form does not allow you to save your progress during filing. After submission, a read-only copy of your FBAR will be available for download

If a filer holds a financial interest in more than 25 accounts, check the yes box in item 14 and indicate the number of accounts in the space provided. Do not complete any further items in Part II or Part III of the report. Sign the form in item 44/45 and enter the date signed in item 46. Any person who lists more than 25 accounts in item 14 must provide all the information called for in Part II and Part III when requested by the Department of the Treasury. You can contact business yield services to get started with the FBAR filing.

FBAR 2023 Deadline

To avoid tax penalties, make sure to file FinCEN Form 114 timely. The FBAR deadline is April 15 in the calendar year you’re reporting. The FBAR 2023 deadline is April 15th as well. This form has an annual filing requirement. If you cannot file the form before the FBAR filing deadline, there is an automatic FBAR 2023 deadline extension to October 15.

If you need to file the FBAR form later than April 15, 2023, you will need to meet special conditions to extend the deadline further. For example, if there was a pandemic, the government may offer an additional FBAR extension for the FBAR 2023 deadline.

FBAR penalties

So what happens when you don’t file before the FBAR 2023 deadline when you’re supposed to? I’m sure your guess is as good as mine, penalties! Under the current rules, if you’re required to file but either do not file on time or do not correctly report your foreign accounts, you can be subject to a penalty of up to $10,000 per violation. This is true even if you did not know you were required to file.

If you knowingly fail to file the FBAR penalties are much harsh. When you’re aware of your requirement and do not file accurately, or if you don’t file it on time, you could get hit with a $100,000 penalty per violation or an even higher penalty, depending on your account balances at the time of the violation. There are penalties even if the failure resulted from an honest misunderstanding of the rules.

Before 2003, it was the responsibility of FinCen to investigate any crimes related to the FBAR. However, the delegation of this authority is currently with the IRS.

The amount of FBAR penalties you will owe depends on your specific circumstances. The maximum penalties permissible by law have an annual adjustment for inflation.

Civil Monetary Penalties

Currently, the maximum civil monetary penalties are as follows:

- Negligent violation – $1,166

- Non-willful violation – $13,481 for each negligent violation

- A pattern of negligent activity – $90,743

- Deliberate failure to file or maintain required records. 50 percent of the amount in the account at the time of the violation or $134,806.

- Deliberate failure to file or maintain required records while also violating specific other laws. The greater of 50 percent of the amount in the account at the time of the violation or $100,000.

- Deliberately falsifying an FBAR. 50 percent of the amount in the account at the time of the violation or $100,000.

Criminal FBAR Penalties

The maximum criminal penalties that may apply are as follows:

- Willful failure to file or maintain required records. Up to five years in prison, a fine of up to $250,000, or both.

- Willful failure to file or maintain required records while also violating specific other laws. Up to 10 years in prison, a fine of up to $500,000, or both.

- Knowingly and willingly falsifying an FBAR – Up to five years in prison, a fine of up to $10,000, or both.

In the past, it was possible to avoid filing a required FBAR form without facing any consequences because FinCen did not have the resources to enforce filing requirements.

However, the IRS now has the power and third-party information to enforce this law. Taxpayers are no longer able to neglect their FBAR responsibilities without facing severe consequences.

As recently as 2018, one U.S. taxpayer who failed to file required FBARs faced a staggering penalty of $800,000.

Some taxpayers believe that even if they are caught, and there is a penalty assessment, the IRS won’t enforce the penalty. The IRS statute of limitations on assessing FBAR penalties is six years. So far, taxpayers’ attempts to use the 8th Amendment to avoid excessive fines related to FBAR violations have failed. Consequently, the IRS has the ability to attach to your income and assets to recover outstanding FBAR penalties and freeze your passport

Common Mistakes

The law surrounding FBARs can be tricky, especially when dealing with other complex tax laws. Here are some of the most common mistakes taxpayers make when dealing with the FBAR.

#1. Misunderstanding the filing threshold.

Some mistakenly assume that they don’t need to file an FBAR form as long as none of their accounts reach $10,000 during the year. They even go out of their way to prevent any account from reaching this balance. However, the FBAR threshold is based on your accounts’ aggregate balance, so individual balances are not important. If the sum of all accounts is ever greater than $10,000 during the year, you must file an FBAR.

#2.Thinking that the law only applies to bank accounts.

Bank accounts are not the only assets that have a reporting requirement on the FBAR. The rule applies to many different types of foreign financial accounts and assets. This includes life insurance policies with cash value, mutual funds, and many more.

#3. Assuming that ownership of the account matters.

Provide you have authority over a foreign financial account and you meet the filing threshold, you must submit this form.

#4. Assuming the FBAR doesn’t apply to minor children.

There is no reporting exception for minors. A child must also file if the filing requirement applies.

#5. Thinking the government won’t notice the missing forms.

Some people mistakenly believe that they don’t need to file an FBAR. The government has measures in place to make sure that United States taxpayers follow the law. Suppose you fail to file a required FBAR. In that case, the United States government will check the information (or lack thereof) provided by you with the information it receives from foreign financial institutions holding your accounts. When it’s clear that you have not filed the required forms, you will face civil and criminal penalties. If you have ever filed an FBAR form in the past, you are now in the FinCen database. It’ll even be easier to track your activity.

Omitted Account Mistakes

#1. Not reporting foreign pension accounts.

Generally, foreign pension accounts are reportable on the FBAR.

#2.Not reporting FBAR crypto (cryptocurrency).

While there is no definite guidance on whether FBAR crypto is reportable (although guidance is expected to be forthcoming stating that cryptocurrency is reportable), a conservative (aka “safe”) approach would be to report. In fact, recently, FinCEN has now announced (FinCEN Notice 2020-2) an intention to amend the rules to require FBAR disclosures for a virtual currency like Bitcoin.

#3. Not reporting business accounts.

All foreign accounts, business, and personal must be reported.

So now that we know how important the FBAR report is, there is no need to delay. So no matter how complicated your US tax return is, business yield services are ready to help with your FBAR filing. The FBAR 2023 deadline is around the corner!

What accounts are required to be reported on FBAR?

FBAR requires individuals to report foreign bank accounts and other financial accounts, such as brokerage accounts, if the combined balance of these accounts exceeds $10,000 at any point during the calendar year.

How do I report multiple foreign bank accounts on FBAR?

Individuals are required to report all of their foreign bank accounts and other financial accounts on FBAR. Each account must be reported separately on a separate FBAR form.

Can I file FBAR electronically?

Yes, FBAR can be filed electronically through the Financial Crimes Enforcement Network (FinCEN) website.

How do I correct errors on a previously filed FBAR?

Individuals can correct errors on a previously filed FBAR by filing an amended FBAR. The amended FBAR must be filed electronically, and the amended form should be clearly labeled as “Amended.”

What happens if I do not report my foreign bank account on FBAR?

If an individual does not report their foreign bank account on FBAR, they can face severe penalties, including civil fines, criminal penalties, and in some cases, imprisonment. The penalties for not reporting foreign bank accounts on FBAR can be substantial and far exceed the balance in the account.

How does the IRS determine if a foreign bank account is reportable on FBAR?

The IRS determines if a foreign bank account is reportable on FBAR by reviewing the combined balance of the individual’s foreign bank accounts and other financial accounts. If the combined balance exceeds $10,000 at any point during the calendar year, the accounts are reportable on FBAR.

Can a corporation file FBAR for its foreign bank accounts?

Yes, a corporation can file FBAR for its foreign bank accounts. FBAR reporting requirements apply to corporations, partnerships, trusts, and other entities in addition to individuals.

FBAR FAQ’s

What is due date of FBAR?

On the 15th of April

The annual deadline for filing Reports of Foreign Bank and Financial Accounts (FBAR) for foreign financial accounts is April 15.

What is the difference between FBAR and FinCEN?

FBAR is an abbreviation for Financial Accounting Report (aka FinCEN Form 114) It is more accurately known as the Foreign Bank and Financial Account Reporting form, and it is technically known as FinCEN Form 114. The form is submitted electronically to FinCEN. The form is not part of your tax return.

What are the penalties if forgot to file FBAR?

Failure to file an FBAR on purpose is a felony punishable by 5 years in jail. If it doesn’t get your point across, the civil fines will. While only a small number of people are prosecuted criminally, the IRS routinely imposes civil penalties for intentional failure to submit FBAR.

Do I need to file FBAR if less than 10000?

An account with a balance of less than $10,000 MAY be required to be reported on an FBAR. A person who is required to complete an FBAR must report all of his or her overseas financial accounts, including those with balances less than $10,000.

Related Articles

- UNEMPLOYMENT TAX FUND: Compensation, Overview & All You Need To Know

- DRIVING WITHOUT INSURANCE: Penalties and Fines in the Different States

- List of Federal Government Grants 2021, Updated!!!

- INTERNATIONAL MARKETING: Strategies, Types, Examples, Pros & Cons

- EMBEZZLEMENT CHARGES: How To Beat & Get Out Of These Charges (Detailed Guide)