With a lot of fuss surrounding which is a better option between a deed of trust and a mortgage, this post is timely. You would agree with me that making choices, in general, is often a big deal especially when you have no idea what you are getting into. However, it gets easier when the facts are laid out plainly before you and you know what you want. In other words, a clear match between the two, (mortgage vs deed of trust) is the first step to making that choice less frustrating. But in the same vein, we will also have to take look at what the term “deed of trust” really means, best practices in California, and a sample of the form.

What is a Deed of Trust?

A deed of trust is a legal document that serves as a contract between you, the homebuyer, and your lender. In clear terms, it indicates that you must repay the loan, bringing into the picture a third party known as the trustee, who will hold legal rights to the property until you do.

Basically, it helps to secure a loan as it is registered in public documents. As a result, borrowers are obligated to sign a trust deed where a state needs one in order to obtain a home loan as much as they would for a mortgage in another state.

Deed of Trust’s Parties

A deed of trust comprises of three parties, in contrast to a real estate mortgage, which only has two parties: the creditor and the lender. But let’s take a break on that considering the fact that we’ll take a broader look at Mortgage vs Deed of trust later in this post.

So basically the list below are parties that make up a deed of trust:

- The borrower, who is also known as the trustor (the person purchasing the home or other piece of real estate).

- The Lender, who is the person or individual bringing up the funds for the purchase is known as the lender.

- The Trustee, who is a third-party entity that has legitimate rights to real estate. Since trustees do not represent either the seller or the buyer in a real estate deal, they are often neutral. Typically, the trustee is a distinct legal body, such as a title corporation.

- A Guarantor is a fourth person that is may join the equation in a deed of trust. He/She is someone who signs alongside the trustor. This also gives the trustee some other way to retrieve funds if the creditor fails in their responsibilities.

How does a Deed of Trust Work?

In a real estate sale, such as the purchasing of a house, a lender gives the borrower money in return for one or more promissory notes (a legal note that promises to pay a loan) attached to a trust deed. This agreement gives an independent trustee, such as a title company, escrow company, or bank, legal title over the real property, which counts as collateral for the promissory notes. However, the creditor retains equal title—the right to gain sole ownership—as well as full use and responsibility for the land or property.

This state of affairs persists during the loan’s maturity cycle. If the trustor (borrower) fails to meet their commitments under the lease, the trustee reserves the right to sell the property. On the other hand, if the lending terms are fulfilled and the buyer fulfills their obligations, the trustee transfers/reconveys custody of the property to the buyer, who now has full title to the property.

Components of a Trust Deed

For the most part, the majority of the components in a deed of trust are the same as in a lease. These basically include the following:

- The loan’s initial amount

- A legal overview of the property that serves as protection or collateral for a loan.

- Names of the three parties

- The loan’s origination and maturity dates

- The mortgage’s terms and conditions

- Fees on late payments

- Legal actions and processes if a default arises default

- Alienation and acceleration clauses (this is when the court declares a homeowner delinquent or when they sell the home)

- Provisions like prepayment fees or the terms of an adjustable-rate mortgage for Riders, if any.

P.S: If the creditor does not pay according to the promissory note’s terms, the trustee may file a notice of default. The trustee may also appoint a new trustee to oversee the mortgage process. In most cases, this is done by filing a formal Substitution of Trustee.

Mortgage vs Deed of Trust

A deed of trust is often an alternative for mortgages in some jurisdictions. Basically, a mortgage policy establishes a lien on real property, covering the homeowner in the event that the creditor fails to meet their obligations. But while both a deed of trust and a mortgage give the lender a security interest in the land, unlike a typical mortgage, the lender does not own the security interest. Other major differences and similarities between mortgage and deed of trust (mortgage vs deed of trust) include the following;

Read Also: Bargain and Sale Deed: How it Works, Importance, Components & Drawbacks

- The creditor and the seller are the only parties to a mortgage deal. On the other hand, Deeds of Trust comprises of an additional party (Trustee). The third-party trustee retains the equitable title to the real property held by a deed of trust.

- A promissory note is kept by the lender until the debt is returned in full, and unlike a deed of trust, it is not usually registered with the county recorder or registrar of titles (also known as the county clerk, register of deeds, or land registry).

- Both trust deeds and mortgages are vital to creating liens on real estate and private loans in the bank.

- A trust deed is not the same as a loan despite the fact that it is classified as such.

- Whether you have a deed of trust or a mortgage determines the type of foreclosure you’ll face. You’ll almost always face a nonjudicial foreclosure if you have a deed of trust. Your lender will have to go through the courts if you have a mortgage.

- If you have a mortgage debt, your lender will need to pursue a court foreclosure to reclaim your property. This means that foreclosing on a mortgage takes a lot longer and costs a lot more money. As a result, if your state allows it, many mortgage lenders will employ a deed of trust instead of a mortgage, as well as nonjudicial foreclosures. Your lender will almost always spend less time and money retrieving your property in this situation.

Promissory Notes

Promissory notes are a vital component of deeds of trust. The underlying piece basically serves as collateral for the sums the lender gives out to fund the real estate transactions. Major elements of a promissory note are;

- the interest rate,

- payment terms

- the buyer’s obligation to pay the loan

- the balance of the loan plus interest

Carefully analyzing the above, it’s safe to say that promissory notes make up at least 50-60% of the components of a Deed of Trust. Furthermore, when the debt is paid off, the promissory note is signed “paid in full” and returned to the creditor along with a registered reconveyance deed. Over the duration of the loan, the promissory note is held by the issuer. Until the loan is paid off, the creditor has just a copy.

Similarities

The following are some of the similarities between a deed of trust and a mortgage:

Both of these options allow your lender to reclaim your home through foreclosure. Both deeds of trust and mortgages have the same essential function. They’re both agreements that say your lender can foreclose on your home if you don’t follow the terms of your loan. Although the type of foreclosure varies, the procedure remains the same.

Both are governed by state legislation. State laws apply to both deeds of trust and mortgages. This implies that the type of contract your lender must use is determined by your state’s legal requirements. Only a mortgage is permissible in some states. Lenders can only use a deed of trust in some cases. Only a few states (Alabama and Michigan, for example) allow both. If your state allows both types of contracts, your lender will decide which one you get.

The Benefits and Drawbacks of Investing in Trust Deeds

Investors looking for high yields often turn to the real estate market, which would be incomplete without a deed of trust. The trust deed investor/lender loans money to a developer working on a real estate project through this document. This implies that the investor’s name will have to appear on the deed of trust. At the end of the deal, the lender earns interest on his loan and receives his entire principal back.

But then you are faced with the question, Who exactly are the people involved in deals like this? Definitely not banks. Banks are unable to lend to such kinds of developments. On the other hand, cautious lenders can move too slowly, especially for developers on a tight deadline.

This often leaves them in a tight spot. As a result, trust deed investors come into play. The goal is to earn a high rate of return on their investments. They literally benefit from diversification into a new asset class without needing to be specialists in real-estate development or management: this is a passive investment.

However, Investing in trust deeds comes with certain risks and drawbacks.

- Real estate shares, unlike bonds, are not liquid, which means that investors cannot get their capital back immediately.

- Furthermore, borrowers should only expect the debt to attract interest; any further capital appreciation is impossible.

- Investing parties could take advantage of any legal flaws in the trust deed, resulting in expensive legal entanglements that could jeopardize the investment.

- The average investor with little experience can struggle. This is because finding reputable and trustworthy developers, projects, and brokers necessitates in-depth knowledge.

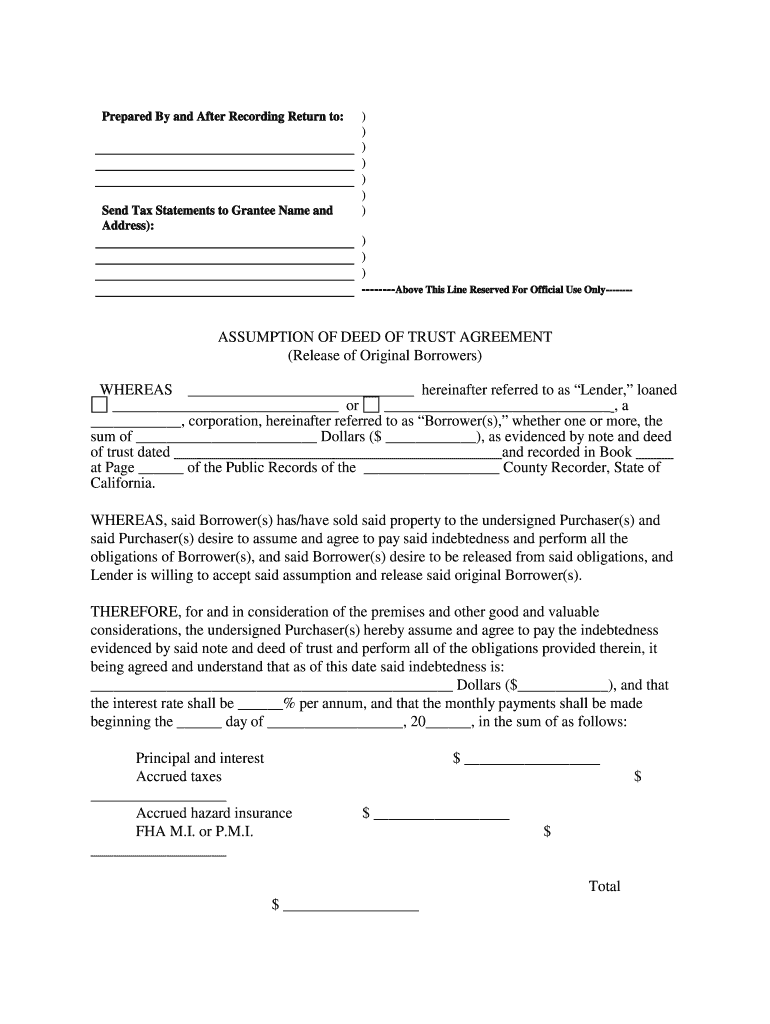

A Trust Deed Example in the Real World (Form in California)

The example below shows a short form of a deed of trust contract used in California for most lenders. It also shows their conditions. Basically, the form starts with a glossary of words and blank spaces for the borrower, lender, and trustee to fill out their information. The amount borrowed as well as the property’s address is also required.

Following this clause, the contract specifies the transition of property rights and uniform covenants, which include:

- Information on how to pay the principal and interest

- Funds held in escrow

- Liens (legal claims over the property).

- Insurance details and maintenance of structure

- Structure occupancy—requires the landlord to move in within 60 days of receiving the loan.

- Nonuniform covenants, which state default, or violation of any of the arrangement clauses. It further states that the loan in question is not a home equity loan—that is, one from which the borrower would receive cash—but rather one for the purchase of the house.

The deed of trust concludes with a signature space for the creditor, who must sign in the presence of a notary and two witnesses.

What Is a Deed of Trust?

A Deed of Trust is a secured real-estate transaction that is used in some states instead of mortgages. In most states, the borrower gives the trustee legal title to the property, which he or she keeps in trust for the borrower’s use and benefit.

How Does a Deed of Trust Work?

A Deed of Trust is an agreement between a lender and a borrower to transfer ownership of the property to a neutral third party who will act as trustee. Until the borrower pays off the loan, the property is held by the trustee. The legal title to the property, on the other hand, is held by the trustee.

What Is the Purpose of a Trust Deed?

In funded real estate transactions, trust deeds give a third party—such as a bank, escrow business, or title company—legal ownership of a property to hold until the borrower repays the lender. Investing in trust deeds can give a steady stream of income.

What Is the Difference Between Deed of Trust and Deed?

Both a warranty deed and a deed of trust can be used to change who owns a piece of property. But who is protected is different between these two contracts. As you now know, a deed of trust protects the person who gets the money (lender). On the other hand, a warranty deed helps protect the property owner.

Is Deed of Trust Legally Binding?

Yes, the owners are legally bound by it. However, when splitting financial assets in divorce proceedings, a Family Court may overlook this. A Declaration of Trust protects owners because it is a legally binding document. This is especially comforting if a situation arises between owners who have divorced.

Conclusion

For Real Estate Investors who do not want to get actively involved, trust deed investing is a viable option. Hope this post was able to give a heads up concerning deeds of trust in general with reference to forms in California. You can reach out in the comment section for questions on how to go about this.

- Reconveyance Deed of Trust: Practical Guide !!!

- Declaration of Trust: Best US Practices & Definitive Guide

- LIVING TRUST: Overview, Cost, Templates, Pros & Cons (+Writing Guide)

- Mortgage: Simple 2023 Guide for Beginners and all you need Updated!!!

- Declaration of Trust: Best US Practices & Definitive Guide