Almost all business transactions require money, making prudent financial management an important part of running a business.

In this article, we will discuss the Degree of financial leverage, how to calculate DFL, the importance of leverage, and many more.

What is a Degree of Financial Leverage (DFL)?

A degree of financial leverage (DFL) is a leverage ratio that measures the sensitivity of a company’s earnings per share (EPS) to fluctuations in operating profit as a result of changes in its capital structure. The degree of financial leverage (DFL) measures the percentage change in earnings per share for a change in operating profit, also known as earnings before interest and taxes (EBIT).

This relationship shows that the higher the level of financial leverage, the more volatile the returns. Since interest rates are usually a fixed expense, leverage increases returns and EPS. This is fine when operating profit is increasing, but can be a problem when operating profit is under pressure.

Financial Leverage

Financial leverage is the ratio of a company’s equity to financial debt. It is an important element of a company’s financial policy. Financial leverage can also mean using the company’s financial resources at a fixed price. A financial leverage of two implies that for one dollar of equity there is two dollars in financial debt. This enables the company to use debt to fund acquisitions of assets.

The concept of leverage is widely used in the business world. It is primarily used to increase the profitability of a company’s equity, especially when the company is unable to increase its operational efficiency and return on investment. Because loan yields are higher than the interest payable on debt, the overall profit of the company increases, and ultimately the profit for shareholders.

The leverage effect can be favorable or unfavorable. It is positive when the income is greater than the cost of the debt. However, it is negative when the company’s profits are less than the cost of insuring the funds. Leverage is an essential source of capital to support limited shareholder investments. It also helps you get the ideal return on equity.

What are Sources of Financial Leverage?

When a company decides to use debt financing for the vast majority of its assets, financial leverage exists. Companies resort to this method when they are unable to achieve their capital demands by issuing shares on the open market. A company that is short on cash will look into loans, credit lines, and other forms of financing if they are in need of more funding.

What are the Types of Financial Leverage?

Leverage comes in two primary flavors: financial and operating. A company can raise capital by issuing fixed-income securities or by borrowing money directly from a lender in order to boost financial leverage.

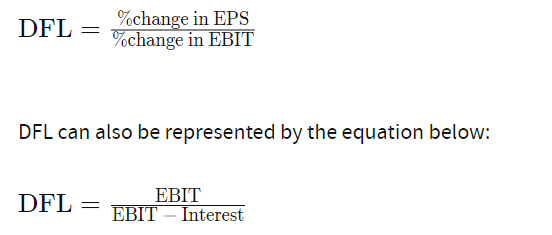

Formula for DFL

The formula for the degree of financial leverage calculates the change in net income resulting from the change in the company’s earnings before interest and taxes. helps determine how sensitive the company’s profit will be to changes in the capital structure.

As can be seen from the formulas below, the level of financial leverage can only be calculated from the Profit and Loss Account. The DFL formula measures the change in net income when the operating result changes by 1% (which can also be referred to as earnings before interest and taxes or EBIT). The output of the DFL formula can be read as “for every 1% change in the operating result, the net result changes by X%”.

Although the formulas only talk about interest expenses, dividends on preferred capital must also be included, as this is the most common type of financing. When the company has preferred capital in its capital structure. If a company is profitable and has no funding other than equity, the DFL is equal to 1. In most cases, however, the DFL is always greater than 1, as debt and preferred equity financing are often used to leverage equity.

What Does the Level of Financial Leverage Tell You?

The higher the DFL, the more volatile the earnings per share (EPS). Since interest is a fixed expense, leverage increases ROI and EPS, which is good when operating income is rising, but can be a problem during tough economic times when operating income is under pressure.

DFL is invaluable in helping a company assess how much debt or financial leverage to choose in its capital structure. If operating income is relatively stable, earnings and earnings per share would also be stable and the company can afford to take on significant debt. However, if the company is in an industry where operating results are quite volatile, it may be wise to keep debt levels down to manageable levels.

The use of financial levers varies greatly depending on the industry and industry. There are many industrial sectors in which companies operate with a high degree of financial leverage. Retail stores, airlines, supermarkets, utilities, and banking institutions are classic examples. Unfortunately, the excessive use of financial leverage by many companies in these sectors has played an important role in forcing many of them to file for Chapter 11 bankruptcy.

Degree of Financial Leverage vs Balance Sheet Financial Leverage

While both the level of financial leverage calculated from the income statement and the most common financial leverage metric used on the balance sheet have to do with quantifying the risk to a company’s capital structure, it does so in two different ways and you can sometimes lead to conflicting results.

The differences arise because the interest rates on debt can vary widely between companies or industries, and the interest rates on debt can also change over time. The amount of financial leverage on the balance sheet may be the same, but if the interest rates are different, the amount of financial leverage will be different because interest expense is charged on the same dollar debt.

How to Measure the Effects of Leverage

The effect of leverage is measured by subtracting the economic rate of return after corporate tax is deducted from the return on equity. Since shareholders’ return on equity is typically higher than the economic performance ratio, leverage plays an important role in meeting investor expectations for return on equity. For this reason, the financial leverage is measured by how the additional debt affects earnings per common shareholder.

What are the Importance of Financial Leverage?

Leverage offers companies the following benefits:

- Leverage is an essential tool that senior management can use to make the best funding and investment decisions.

- It offers a variety of funding sources through which the company can achieve its targeted profits.

- Leverage is also an important investment technique as it helps companies set a threshold for growing their business. For example, it can recommend limits on business expansion once the projected return on the additional investment is below the cost of debt.

Conclusion

Understanding a company’s level of financial leverage can enable an investor to assess the risk and return associated with its capital structure. Interest expenses are the most common type of financing. However, if the company has lease obligations or preferred stock in its capital structure, the related payments should also be included in the DFL calculation.

WE ALSO RECOMMEND THE FOLLOWING