A successful cash flow forecast may be the single most important component of a business plan. If there isn’t enough money to pay the bills, all of the policies, strategies and existing business operations are useless. That’s what a cash flow forecast is for: forecasting the cash requirements ahead of time. So in the course of this post, we will take care of every detail of cash flow forecasting models, templates, and tools.

We use the term “cash” to refer to money that can be spent. Your bank account, deposits, and liquid securities such as money market funds are all examples of cash. It’s not just money in the form of coins and bills

What you Should know about Cash Flow Forecasting

The ensuing paragraphs cover important details you should know when it comes to Cash flow forecasting, its tools, its uses, and the different methods of forecasting.

#1. Profits aren’t the same as cash

Profitable businesses will run out of cash if they don’t keep track of their finances and control their cash flow as well as their income.

For example, your company might spend money that does not appear on your profit and loss statement as an expense. Your profit margins are lowered as a result of normal expenses. However, certain expenditures, such as inventory purchases, debt restructuring, new equipment, and asset purchases, decreases your cash flow but not your profitability. As a result, the company could spend money while still appearing successful.

On the sales side, your company can make a sale to a customer and issue an invoice, but not receive payment right away. The sale increases your profit and loss statement’s revenue, but it doesn’t appear in your bank account until the customer pays you.

This is why a cash flow forecast is crucial. It enables you to forecast how much money you’ll have in the bank at the end of each month, regardless of how profitable your company is.

#2. Two ways to create a cash flow forecast

Cash flow forecasts can be done in a variety of ways. The “Direct Method” is the first, and the “Indirect Method” is the second. Both methods are correct and valid. In other words, it is a matter of preference. You can choose the method that works better for you and is the easiest to understand.

Experts, unfortunately, can be obnoxious. It seems like every time you use one tool, a supposed business finances guru tells you you’re doing it wrong. Sometimes, this indicates that the professional isn’t knowledgeable enough to recognize that there are several options. (Xanax)

The direct approach of cash flow forecasting

The direct method of cash flow forecasting is less common than the indirect method, but it is much simpler to use.

It’s less common because it’s difficult to build using standard reports from your accounting software. However, if you’re making forecasts – looking ahead in time – you won’t be depending on data from your accounting system, so it may be a safer option.

The disadvantage of using the direct method is that some bankers, accountants, and investors may prefer to see a cash flow forecast using the indirect method. But don’t worry; the direct approach is just as reliable. After we’ve covered the direct process, we’ll go into the indirect method.

The direct method of cash flow forecasting is based on the simple formula:

Cash Flow = Cash Received – Cash Spent.

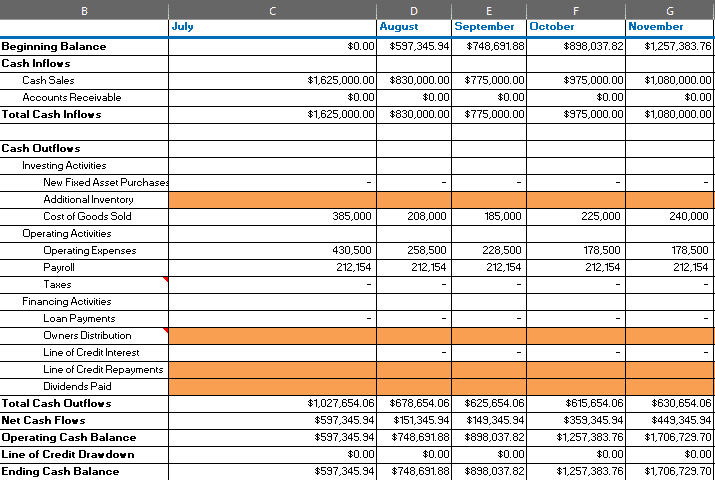

Here’s how the cash flow forecasting looks in practice with a template:

Let’s start by estimating the cash you’ll get, and then we’ll move on to the rest of the cash flow forecast.

Forecasting cash received

You get money from four different places:

#1. Sales of your products and services

This is the “Cash from Operations” portion of the cash flow forecast. When you sell your goods and services, some consumers will pay you in cash right away – this is the row in your spreadsheet labeled “cash sales.” You receive the funds immediately and may deposit them into your bank account.

You may also be required to submit invoices to customers and then receive payment. This allows you to keep track of the money owed to you in Accounts Receivable. On the other hand, when consumers pay their invoices, the money appears in the “Cash from Accounts Receivable” row of your cash flow forecast. The simplest way to predict this row is to consider which invoices will be paid by the prospects/customers and when they will be paid.

#2. New loans and investments in your business

You may also get cash by taking out a new bank loan or making an investment. When you get this kind of money, you’ll record it in the loan and investment rows. It’s important to keep these two forms of cash inflows seperate; primarily because loans must be repaid while investments do not.

#3. Sales of assets

Vehicles, facilities, and real estate are examples of assets owned by your company. When you sell an asset, you typically receive cash, which you monitor in your cash flow forecast under the “Sales of Assets” tab. The profits from the sale of a truck that your business no longer requires, for example, will appear on your cash flow statement.

#4. Other income and sales tax

Aside from sales, businesses may generate revenue from a variety of sources. For example, the money in your business’s savings account can generate interest income.

Sales tax, VAT, HST/GST, and other tax systems are all used by many companies to raise taxes from their customers. Businesses should report the accumulation of this money in the cash flow forecast in a particular row, rather than in sales. You want to do this because the money earned from taxes isn’t yours; it’s the government’s money, and you’ll have to pay it to them eventually.

Forecasting cash spent

You’ll prepare a cash flow forecast for what you plan to spend in a few categories, similar to how you model the cash you plan to receive:

#1. Cash spending and paying your bills

Cash Spending and Payment of Accounts Payable are two forms of cash spending linked to your business’s activities that you can plan for. When you use petty cash or pay a bill right away, it’s called cash spending.

There are, however, bills that you get and then pay later. Accounts Payable is where you keep track of these bills. When you pay bills that you’ve been monitoring in accounts payable, that cash payment will appear as “payment of accounts payable” in your cash flow forecast. Consider what bills you’ll pay and when you’ll pay them when forecasting this row.

Loan payments, asset acquisitions, dividends, and sales taxes are all excluded in this category of the cash flow forecast.

#2. Loan Payments

When you predict debt/loan repayments, you should include the principal repayment in your cash flow forecast. The interest on the loan is reported as a “non-operating cost,” which we’ll go through later.

#3. Purchasing Assets

You’ll model asset acquisitions in your cash flow forecast in the same way you monitor asset sales. Purchases of long-term, tangible assets are known as asset purchases. Vehicles, machinery, buildings, and other items that you may be able to resell in the future. If you keep inventory on hand, you will be able to buy it as an asset.

#4. Other non-operating expenses and sales tax

Other expenditures that are called “non-operating” in your company can exist. These are costs that are not directly related to the operation of your company, such as savings and interest paid on loans.

You’ll also estimate when you’ll have to pay taxes and include those cash outflows in this portion.

The Indirect Method

The indirect method of cash flow forecasting is just as accurate as the direct method and yields similar results.

Whilst the direct approach examines cash sources and uses, the indirect method begins with net income and adds items such as depreciation that affect profitability but not cash balance.

Furthermore, since you can easily get the data for the report from your accounting system, the indirect approach is more common for making cash flow statements in the past.

The indirect cash flow statement is created by taking your Net Income (profits) and then adding items that affect profit but not cash. You can even get rid of items like promotions that have been scheduled but not yet paid for.

To find out your real cash flow, you’ll make five types of changes to your profit number:

#1. Make the necessary adjustments to account for the change in accounts receivable

Not all of the profits are paid in cash right away. You must change the net profit in the indirect cash flow forecast to account for the fact that some of your revenues did not result in cash in the bank but instead boosted your accounts receivable.

#2. Make the necessary adjustments to account for the shift in payables

You’ll need to pay for costs that you’ve booked on your income statement but haven’t yet billed.

This is similar to how you’d account for accounts receivable. Also since you still have the cash on hand and haven’t paid your bills, you’ll need to add these expenses back in.

#3. Depreciation & Taxes

Taxes and depreciation minimize your profitability on your income statement. Since depreciation has no effect on your cash flow, you’ll need to bring it back in on the cash flow statement. Taxes may have been measured as an outlay, but the funds may still be in your bank account. If that’s the case, you’ll need to factor it back in to get an accurate cash flow projection.

#4. Investments and Loans

You’ll want to include any extra cash you’ve got in the form of loans and savings, just as you did with the direct method of cash flow. In this row, make sure to deduct any loan payments.

#5. Assets Bought and Sold

You’ll need to factor in any asset purchases or sales into the cash flow estimates. This is analogous to the direct approach of cash flow forecasting.

Cash flow is about management

Remember: You should be able to forecast cash flow using informed guesses. This is based on a thorough understanding of your company’s revenues, credit sales, receivables, inventory, and payables flows. These are very useful forecasts. Real management, on the other hand, keeps track of forecasts every month with a schedule versus actual review so that adjustments can be caught early and managed. A successful cash flow forecast can inform you when cash will run out in the future so you can plan accordingly. It’s always best to prepare ahead of time so you can set up a line of credit or gain extra funding to help the company weather periods of low cash flow. Maintain the health of your company with precise and simple cash flow forecasting.

Forecasting cash flow and cash balance

Calculating cash flow is easy in the direct cash flow forecasting model. Simply deduct the amount of money you plan to spend in a month from the amount of money you intend to receive. This is what you’ll call your “net cash balance.” If the figure is positive, you have received more money than you have spent. You would be investing more money than you earn if the number is negative.

By applying your net cash flow to your cash balance, you can forecast your cash balance.

Tools for Cash Flow Forecasting

Cash flow forecasting is sadly not an easy job to complete on your own. You can do it with spreadsheets, but the process is time-consuming and prone to errors. Fortunately, there are inexpensive solutions that will make the process much simpler – and they don’t require spreadsheets or extensive accounting expertise. We’ve covered that in a different post.

Meanwhile, to an extent, the cash flow forecasting spreadsheets, models, and templates mentioned in this post is highly effective. While these cash flow forecasting tools are prone to human errors, they help you get a hold of how it really works.

Either way, some tools you would need for cash flow forecasting include Spreadsheets (Microsoft or Google), real-time data, and other accounting tools like QuickBooks, CashAnalytics, and so on.

What Is Cash Flow Forecasting?

Cash flow forecasting means figuring out how much you will make and spend in the future. A cash flow forecast is an important tool for your business because it allows you know if you’ll have enough money to run the business or grow it. It will also show when more money is leaving the business than is coming in.

How Do You Do a Cash Flow Forecast?

The direct cash flow forecasting method makes it easy to figure out cash flow. Just take the amount of money you plan to spend in a month and take it away from the amount of money you plan to get. This is what you mean by “net cash flow.” If the number is greater than zero, you get more money than you spend.

What Are the Two 2 Main Type of Cash Flow Forecast?

Direct and indirect forecasting methods are the two primary types. Direct forecasting focuses on real flow data, whereas indirect forecasting employs anticipated balance sheets and income statements.

What Are the 4 Basic Forecasting Method?

While there are many commonly used quantitative budget forecasting techniques, This is the four basic forecasting methods:

- straight-line,

- moving average,

- simple linear regression,

- multiple linear regression.

Conclusion

In addition to the aforementioned cash flow forecasting template, here is a more comprehensive model you can edit at your convenience. This is a complete financial projection template that covers other financial aspects you would need when forecasting a cash flow statement.