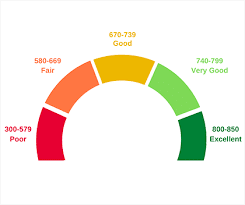

FICO defines fair credit as having a credit score between 580 and 669. The lenders on this list are appropriate for borrowers with fair credit, even though many personal loans demand scores above this level. Even though you’ll be able to get a loan with a score under 670, you shouldn’t anticipate the best terms. The best credit scores often get the greatest loan limits and lowest interest rates. But resist giving up. Even if your credit score is between 580 and 669, lenders are nevertheless willing to offer you finance. In this article, we’ll examine the best credit cards, personal, and mortgage loans for people with fair credit scores.

What is a Fair Credit Score?

A score between 669 and 580 is regarded as fair credit according to the 300–850 FICO credit score range. In addition to other credit accounts like credit cards or mortgages, borrowers with fair credit are more likely to be riskier and may have a harder time being approved for personal loans. If you want to maximize your chances of getting a loan with better terms, it’s advisable to raise your credit score before applying.

Poor payment history, excessive credit use, an excessive number of credit applications, or harsh credit inquiries are the usual causes of fair credit scores. It is essential to concentrate on these aspects of your credit profile if you want to raise a respectable credit score.

Personal Loans With Fair Credit Score

You can get a personal loan only if you meet certain requirements, one of which is your credit score. Those with fair credit scores, which are typically between 630 and 689, may find it more difficult to get approved for a loan than those with strong or exceptional credit.

Still, it’s a possibility. Numerous lenders also take into account other information on an application, including employment, your home’s ownership status, income, and outstanding debts.

Here are the best personal loans for people with a fair credit score, along with details on how to apply for and establish credit.

#1. Upgrade

Upgrade offers accessible online and mobile credit and banking services wexceptWest Virginia, Vermont, and Iowa. The upgrade was founded in 2017. Since then, the platform has given more than 10 million applicants access to more than $3 billion in credit and has continued to grow its web and mobile offerings. Although Upgrade offers loans to people with bad credit histories, its maximum APRs are higher than those of other online lenders.

#2. Avant

Avant is a Chicago-based consumer lending platform that was established in 2012 and provides both secured and unsecured personal loans via a different bank (WebBank). Every state, except Hawaii, Iowa, New York, Vermont, West Virginia, and Maine, except for Washington, D.C., offers unsecured loans. The platform just needs a minimum credit score of 580 to qualify and focuses on middle-class customers with acceptable to good credit.

#3. LightStream

A division of Truist, which was created as a result of the union of SunTrust Bank and BB&T, is called LightStream. The lending platform provides unsecured personal loans ranging in size from $5,000 to $100,000. Although many lenders offer loans that are smaller than the LightStream minimum, very few lenders offer loans that are larger than the maximum. It’s a great choice for people who wish to spread out the payment of major expenses over time because repayment terms range from two to seven years.

#4. Rocket Loans

Rocket Loans, a subsidiary of Rocket Homes and Rocket Mortgage by Quicken Loans, provides personal loans via Cross River Bank. Also, Rocket Loans is a viable alternative due to its accessibility in the majority of states and minimal minimum credit score criteria. Borrowers must pay origination costs, and the repayment period is only three or five years.

If you need money quickly and have a fair credit score (580 or more), Rocket Loans can be a smart choice for you. Cheaper loan choices might be available, depending on your creditworthiness, but the platform levies origination fees of 1% to 6% of the loan amount and APRs that range from 7.161% to 29.99%.

Credit Cards Fair Credit Score

Credit cards for fair credit score are available to consumers with credit scores between 640 and 699 who are establishing new credit or repairing the damage done to their credit. The best credit cards for people with acceptable credit often have no annual fees and offer rewards of at least 1% back, according to WalletHub’s credit card experts.

Credit cards can help you establish a good credit history, which is crucial for managing your finances if you have a fair or average credit score. You may improve your credit score and be approved for credit cards and loans with better terms and cheaper interest rates, which can save you a lot of money, by using the proper card responsibly.

Even while not everyone will be eligible for the finest credit cards for fair credit, that doesn’t mean you have to accept cards with only exorbitant costs. Numerous credit cards for people with fair credit don’t have annual fees and offer extras that help build credit, like free credit scores and credit monitoring. Some even give you cash back on your purchases, high credit limits, or low-interest rates.

We’ve chosen the top credit cards available for people with fair or average credit as a service. Additionally, we have the knowledge you need to find the best credit card for you and advice on how to raise your credit score.

#1. Capital One Platinum Credit Card

The Capital One Platinum Credit Card gives you enough space to concentrate on raising your creditworthiness without being sidetracked by the pursuit of further benefits. You can automatically be considered for a greater credit limit six months after account activation if you make on-time monthly payments, making it a viable alternative for people with fair credit.

#2. Mission Lane Cash Back Visa® Credit Card

Anyone with fair credit who wants to earn small cash-back benefits may discover their ideal match with this card. This card provides a good foundation for building credit because there is no security deposit necessary and it has a relatively cheap annual charge in comparison to other cards available.

#3. Capital One QuicksilverOne Cash Rewards Credit Card

This Capital One credit card delivers a reliable rewards program with only a $39 annual fee and moderate credit restrictions. If you’re looking for a credit card that will raise your credit score and enable you to accrue cash-back benefits, this is a fantastic offer.

#4. Upgrade Cash Rewards Visa®

As it functions as a hybrid credit card/personal loan, this no-annual-fee card is an option for cardholders who are still getting used to managing their credit. Additionally, you might be eligible for a low, fixed interest rate (APR: 14.99% – 29.99%). Additionally, as you make payments, you can earn a respectable 1.5 percent cash back on all purchases.

#5. Credit One Bank Wander® Card

This card can be ideal if you want to build your credit while earning travel rewards and avoiding a security deposit. It not only has some of the best travel rewards rates of any card available with acceptable credit, but it also allows you a chance to acquire a respectable sign-up bonus, which is even less common on cards with this level of credit.

Fair Credit Score Mortgage

Many individuals with fair credit scores believe they cannot obtain a mortgage. Since only those with credit scores of 800 or higher belong to the credit score elite, those with fair credit are not among them. Instead, borrowers with fair credit are more likely to have a few missed payments or late payments. The good news is that you can still obtain a mortgage with a respectable credit score. IIntelligentlenders might be enthusiastic about your company.

Fair credit borrowers are necessary for lenders. That is a result of overhead at lenders. Borrowers across the credit spectrum aid them in boosting profitability and maintaining operations.

Not all borrowers have credit scores above 800. To increase output and profits, lenders must also take into account borrowers with fair credit. Lenders essentially want folks with fair credit to be able to obtain financing.

A mortgage to think about if your credit score is fair is:

#1. FHA financing

Borrowers can get an FHA mortgage with 3.5 percent down as long as their credit score is at least 580. There is a 10% down payment required for credit scores below 580. Additionally, borrowers with credit scores below 620 and a high debt-to-income ratio must now undergo manual underwriting.

#2. VA mortgages

There is no official minimum credit score required by the VA. However, actual VA lenders are free to add their credit score requirements These requirements typically range from 620 to 660. Homebuyers with qualifying military experience are eligible for VA loans, which need no down payment.

#3. Conventional 97 percent financing

Two examples of three percent down conventional loans are the new Fannie Mae HomeReadyTM mortgage and the Freddie Mac Home Possible Advantage® mortgage. Several fresh private-sector options require only three percent down.

Tips for Comparing Personal Loans for Fair Credit

When comparing personal loans for fair credit scores, keep the following in mind:

- Evaluate interest rates at their highest. With fair credit, you’re likely to receive an interest rate at the high end of the range because interest rates are heavily influenced by your qualifying credit score. So be sure to compare the maximum rate when comparing personal loans for people with bad credit.

- Prequalify with a provider, if at all possible. You have the option to prequalify for a personal loan with several lenders. This entails that you can provide information about your income, your intended purpose for the loan, your housing condition, and other factors to find out about possible loan limits, interest rates, and repayment alternatives.

- Verify any additional charges. Some lenders of personal loans don’t impose origination fees, late payment penalties, or prepayment fines. Some, though, might tack on all or some of these fees. Consider the fee structure in addition to the prospective interest rate when evaluating personal loans.

- Consider your options for customer service with the lender. Before you sign the loan agreement, there is one more thing to think about if you’ve found a lender. Although customer service may not seem important, it can be extremely important if you have problems making payments or are having financial difficulties while making your repayments.

How to Get A Personal Loan With Fair Credit

- Examine your credit reports. To find any mistakes or opportunities to raise your credit score, check your reports from the three main credit bureaus. Consider spending more time improving your score if it is already rising before you apply for a personal loan.

- Examine lending criteria. The aforementioned lenders accept applicants with fair credit, but many also take into account income and DTI. Some lenders look at a wide range of variables, including your work history and the college you attended. Learn what information each lender wants on a loan application by comparing qualification standards.

- Prequalify. Pre-qualify to determine your likelihood of receiving a personal loan approval and to browse prospective offers. A soft credit check is used in the procedure, which has no impact on your credit score.

- Submit an application When you’ve located a lender. While many major lenders offer quick and easy online applications, some banks and credit unions may insist on a face-to-face meeting.

Where to Get Fair Credit Loans

The same businesses that offer traditional personal loans also offer fair credit loans. They consist of the following:

- Banks.

- Credit unions.

- Online lenders.

- Peer-to-peer lenders.

Credit unions and online lenders are frequently the best options when looking to get a loan with fair credit. They frequently have less onerous restrictions than banks, as well as lower interest rate caps and fees than peer-to-peer lenders, which is why.

Is a 650 credit score bad?

Scores between 650 and 749 are regarded as “fair,” scores between 700 and 749 as “good,” and scores between 300 and 649 as “bad.”

Is a 600 credit score fair or poor?

Your score falls within the range of scores, from 580 to 669, considered Fair. A FICO® Score of 600 is below the national average.

What credit score range is fair good?

580-669. In general, credit ratings between 580 and 669 are regarded as fair, and those between 670 and 739 are as good.

How to get ca redit score from 650 to 800?

- Always pay your bills on time.

- Maintain low credit card balances

- Consider your credit history carefully

- Expand your credit portfolio

- Check your credit reports

How bad is a 620 credit score?

A 620 credit score is considered fair.

How to go from a 600 to a 700 credit score?

- Lower your credit utilization.

- Limit new credit applications.

- Diversify your credit mix.

- Keep old credit cards open.

- Make on-time payments.

How accurate is credit karma?

The credit scores and reports you see on Credit Karma originate directly from TransUnion and Equifax, two of the three major consumer credit bureaus. The credit scores and reports you see on Credit Karma should accurately represent your credit information as published by those bureaus

How long does it take to go from a 600 to a 700 credit score?

You may be able to raise your credit score by 100 to 150 points in 90 days, depending on your credit history.

Related Articles

- UPGRADE CREDIT CARD: Free Tips, How to Do It, Limit & Review

- WHAT IS A FAIR CREDIT SCORE? How To Improve It

- The BEST CREDIT CARDS FOR FAIR CREDIT 2023 (Detailed Guide)

- WHAT IS BUSINESS CREDIT: Definition, and Uses

- WHAT IS CONSIDERED AN EXCELLENT CREDIT SCORE? Detailed Guide