If you are the lucky recipient of a $1 million lottery prize, you have two choices: 10 annual payments of $100,000 each (totaling $1 million during that period) or a lump sum payment of $1 million made immediately. Which is the best choice, tax implications aside? Your comprehension of the time value of money (TMV), its calculation, and its examples will determine the answer.

Time Value of Money

According to the time value of money (TVM) theory, a certain sum of money is worth more now than it would in the future because of the potential for future gains. In finance, time’s monetary value is the bedrock idea. Having cash in hand is preferable to be promised payment at some future time. The term “present discounted value” can be used to refer to the time value of money.

Value Changes with Time

If you want to invest your money and see it grow over time, you need to have a firm grasp on how money’s value fluctuates over time. Even if you merely put money in a savings or CD account, you can still earn compound interest.

On the other hand, cash on hand will depreciate if not invested. It’s easy to see the difference when you compare what a dollar will purchase now with what it did when you were a kid. This is because both inflation and the potential for lost revenue cause your dollar’s value to decline. You will lose more than just the purchasing power of your money to inflation if you hide $10,000 under your bed for a decade.

“So many young people are so busy managing their lives that they are missing out on the compounding returns of investing modest sums of money.” If a person at age 25 decided to invest $50 per month, they would need to contribute three to four times as much if they waited until age 35.

The time value of money (TMV) idea is the bedrock of nearly all financial and investment choices. Consider the time value of money while making financial decisions such as asking for a loan, negotiating a wage, or buying a purchase.

Time Value of Money Calculation Examples

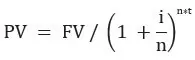

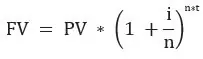

Here is the formula for Time Value of Money Calculation with Examples

0r

0r

Time Value of Money Examples

The fundamental calculation for calculating the time value of money is as follows: future value of money, present value (PV), future value (FV), the value of the individual payments in each compounding period (n), the number of periods (t), the interest rate (I). The formula for calculating the time value of money is based on these factors

Let’s look at an example of the Time Value of Money calculation:

Example 1

Mary purchases a stock that is expected to yield $20 in dividends in year one and $21.6 in year two. As soon as he receives the second dividend, he plans to sell the shares for $333. 3. What is its intrinsic value?

in this stock, is a 15% return necessary?

To ensure that the needed return is 15%, Mary tries to establish the intrinsic value of the stock. The investor begins by calculating the dividends’ present values for years one and two. Using the aforementioned equations, he discovers,

- $20 x ((1.15) x 1) x current value (Year 1)

- $20 / ((1.15) 2) corresponds to the present value (year 2).

- The first- and second-year dividends in this instance total $17.3 and $16.3, respectively.

- Second, he calculates the selling price two years from now’s the present value.

333.3% of the selling price, divided by 1.15, is the PV.

= 252.0

Mary now adds the present value of the dividends and the present value of the selling price to determine the intrinsic value of the stocks.

Total Annual Present Value + Total Annual Present Value (Selling Price)

= $17.4 + $16.3 + $252.0

= $285.8

Example 2

You can compare the amount of money you would have if you invested the $15,000 today with holding out for the $15,500 for two years using this method. Assuming the aforementioned scenario, let’s say you have the option to invest the $15,000 you receive from the car sale today in a CD that pays 2% annually on a monthly basis compounded interest. How to calculate how much money will be worth in two years is as follows:

FV = $15,000 x (1+(0.2/12))(12×2)=$15,612

For the $15,000 you spent on the car today, it will be worth $15,612 in two years. If you hold off on receiving the $15,500 payment until two years from now, you would forfeit $112 in interest that you could have earned. With assets that have bigger returns, like stocks or real estate, the odds of being unsuccessful will be significantly greater.

What are the Elements of the Time Value of Money?

Consideration of five factors is necessary for any time value of money problem. The letter in parentheses indicates the symbol that is employed in mathematical computations. You can often compute the final element using a formula or a financial calculator when only four of the five parts are known.

- (n) Periods. Periods are the total number of time units that comprise the holding time.

- (i) Rate.A common way to express interest or a discount rate is as an annual percentage.

- . (PV) Present Value . The present worth of a sum of money informs you of its current value.

- (PMT) Payment. The amount of money received or equally distributed for each period is known as the payment. Positive payments are those received, and negative payments are those made.

- (FV) Future Value . The future value is a certain amount of money that is projected to be received or distributed in the future.

The difference between a sum of money in the present and that same sum in the future is known as the time value of money. The value of money today exceeds that of money in the future.

The appropriate rate that connects the two sums is the discount rate. The present value is made up of the current quantity, the future quantity, and the future value.

What Is the Time Value of Money for Example?

Let’s have a look at some time-worth of money examples. At the end of the year, you would have $105 if you invested $100 (the present value) for a year at a 5% discount rate (the future value). In light of this example, $100 today will be worth $105 in a year.

$105 = $100 x 1.05

$100 = $105 / 1.05

Similarly to this, $100 is now only worth $95.24 after being reduced by 5%.

$95.24 = $100 / 1.05

What Are the 4 Basic Time Values of Money Variables?

Present Value (PV), Time Number of Periods (n), Interest Rate (r), and Future Value (FV) are the four variables (FV).

Why Is the Time Value of Money Important?

Retirement planners and investors can make the most of their savings by using the time value of money concept. Understanding this idea, which relates to your savings, assets, and purchasing power, is essential to developing financial literacy.

Savings

Because you did not save aside enough money for your retirement, you could have to decide between a relaxed retirement and one that is stressful. Because your Social Security payments could not completely cover your living expenditures, it’s imperative to have supplemental income.

The most important resource in this case is time. The sooner you understand this idea and incorporate it into your financial planning, the better off you and your retirement savings will be.

Investments

There is a chance that your current investment will increase and compound in value. You will have $1,020 in your account the following year if you deposit $1,000 into a high-yield savings account with a 2% annual interest rate, for example. The next year, you increase the $1,020 total by $20.40. The earnings may increase in value over time.

If you had received the initial $1,000 a year later, the opportunity to earn $20, or a year’s worth of 2% interest, would have been lost. The opportunity cost of waiting is made up of the loss of the first $1,000 as well as potential benefits. When examining investments, it is crucial to balance risk and return because some assets are more volatile and have higher risks than others.

“Investments could vary in value, especially in the short term, but they can appreciate at a pace greater than inflation, “This is crucial in the long run.”

Purchasing Power

As a result of purchasing power inflation, which is the consistent loss of purchasing power, buying power often declines over time. For instance, you could have purchased 20 gallons of milk if you needed $50 worth of milk and a gallon cost $2.50 in the 1990s.

Thirty years later, you still want to purchase $50 worth of milk, but due to inflation, the cost per gallon has increased to $3.50. Currently, just 14 gallons may be bought. In other words, saving money today will yield better rewards than waiting 30 years to do it.

What are the Two Factors of Time Value of Money?

The two elements that specifically influence the temporal value of money are

- Opportunity cost

- Interest rates

Opportunity Cost to Individuals

The exact amount of money spent in each transaction is its “dollar cost,” but when you spend money, you also lose other things. The term “Opportunity Expense” refers to the cost associated with giving up the chance to use that money for something else.

Imagine wishing to travel to Japan. You are preparing to buy the plane ticket after saving up $2,000 for an unforgettable trip. Unfortunately, you get distracted while looking up airfare and wind up watching cat videos for the next six hours. In one of the videos, you fall in love with a Bengal kitten and decide you must immediately purchase one. You look up local cat breeders and learn the going rate for a cute, spotted Bengal kitten.

$2000 (this includes all necessary pet food and supplies).

Time Value of Money and Opportunity Cost

You have two options: either get in touch with the breeder straight away to buy a kitten or go back to organizing your vacation to Japan. In either case, you will use the $2000, but you can only use it in the one you choose. Due to the fact that pursuing one objective typically hinders pursuing a number of other goals, opportunity cost results from this (at least at the same time).

In this case, the temporal value of money is significant. In our first example, you were given the option of lending your friend $100. You won’t be able to use the $100 for personal costs until they reimburse you, even if they do so right away.

Interest Rate

One will earn more money at a higher interest rate. Investing with frequently compounding interest rates could result in bigger returns. However, one should be aware that an investment with a higher interest rate typically has a higher risk. Risk is the possibility that the return on an investment will be lower or higher than anticipated.

A savings or investment strategy with a fixed interest rate (the rate won’t vary throughout the course of the investment) assures a certain return but also entails a significant amount of risk. The amount a person makes from this kind of investment won’t grow if average interest rates climb.

Making sure that interest rates are higher than the rate of inflation is another factor to take into account. The constant increase in the average price of a market basket of products is referred to as inflation. Wealth won’t increase if someone has money invested at 4% and inflation is 4%. They will actually lose money after taxes.

Related Articles

- FAIR VALUE ACCOUNTING: Definition & Benefits of Fair Value Accounting

- BUSINESS VALUE: Meaning & How to Calculate It!!!

- Present Value Formula: Definitions, Examples, Formula & Calculations

- ZERO-BASED BUDGETING (ZBB): Meaning, Merits and Demerits

- PRESENT VALUE OF ANNUITY: Definition, Formula, and Calculator