Accounting is important in our everyday life especially when it comes to business. Moreover, many companies use depreciation to bring down the value of assets over time. Here will be looking at depreciation accounting, definition, method, formula, and understanding accumulated depreciation accounting. To help companies, businesses and individuals learn how they can profitably gain from using depreciation accounting.

What is Depreciation Accounting?

Depreciation is an accounting agreement allowing a company to reduce the value of an asset over a period of time. For example, depreciating expensive assets such as machinery and equipment allows companies to extend that cost and make a profit. Moreover, depreciation is an accounting method of assigning the price of a real asset over its period of existence. In other words, depreciation means how much of an asset’s value has been used up. However, companies consider different factors before they can calculate depreciation. The depreciation method is a factor to consider. So let’s survey the different depreciation methods companies use to calculate depreciation.

Depreciation is also used to account for declines in the carrying value over time. The carrying value represents the difference between the original cost and the accumulated depreciation of the years.

.

Depreciation Accounting methods

#1. Straight Line Depreciation Accounting Method

The straight-line depreciation method reduces the value of an asset correspondingly over each period until it reaches its salvage value at the end of its useful life. This is the most common method to calculate depreciation and a straightforward method for allocating the cost of a capital asset. It is also known as the fixed installment method. Moreover, you can calculate a straight-line depreciation method by simply finding the difference between the original cost of the fixed asset and the salvage value by the useful life of the asset.

Assume a $5,000 machine is purchased by a business. The company determines that the salvage value is $1,000 and that the useful life is five years. The depreciable amount is $4,000 based on these assumptions ($5,000 cost – $1,000 salvage value).

The straight-line method calculates annual depreciation by dividing the depreciable amount by the total number of years. In this case, the annual cost is $800 ($4,000 5). This results in a 20% depreciation rate ($800 $4,000).

#2. Declining Balance Method

This method is calculating the depreciation of a fixed asset as a fixed percentage of its net book value at the start of each depreciation period. This method is also said to incur higher depreciation expenses during the earlier years and lower expenses in later years. Although due to the charging rate, applying to the net book value of the asset the net book value of assets will reduce from time to time after charging depreciation.

Therefore, the method is based on the belief that more depreciation should be charged in the early years of the asset. This is as a result of the low repair cost incurred in such years. As an asset furthers into later stages of its useful life, the cost of repairs and maintenance of such an asset increase. Hence, less amount of depreciation needs to be provided during such years. You can also identify this method as the reducing or diminishing balance method.

Using the straight-line example above, the machine costs $5,000, has a salvage value of $1,000, a five-year life, and is depreciated at 20% annually, so the first year’s expense is $800 ($4,000 depreciable amount x 20%), the second year’s expense is $640 (($4,000 – $800) x 20%), and so on.

#3. Sum of Years’ Digits Method

The Sum of years’ digits method accepts depreciation at an accelerated rate. Although, the depreciable amount of an asset charges to a fraction over different accounting periods under this method. This fraction is the ratio between the remaining useful life of that asset in a particular period. However, this method creates higher expenses in the first years and lower expenses in later years of the asset’s useful life.

So, as an asset moves towards the end of its useful life, the benefit gained out of such asset declines. That is to say, the highest amount of depreciation allocates in the first year since no amount of capital has been recovered till then. Accordingly, the least amount of depreciation should be charged in the last year as a major portion of capital invested has been recovered.

An asset with a five-year life, for example, would have a base of the sum of the digits one through five, or 1+ 2 + 3 + 4 + 5 = 15. 5/15 of the depreciable base would be depreciated in the first year. Only 4/15 of the depreciable base would be depreciated in the second year. This continues until year five when the remaining 1/15 of the base is depreciated.

#4. Double Declining Balance Depreciation Method

This is an accelerated depreciation method that is similar to the declining balance and unlike the straight-line method. Further, this method will charge on the reduced value of the fixed asset at the beginning of the year. However, this method charges twice the amount of straight-line method charges which leads to over-depreciated assets at the end of its useful life in contrast to the anticipated salvage value. It is also sometimes used to depreciate fixed assets heavily in the early years, which allows companies to differ income on taxes to later years. Hence, most companies look for different ways to solve such problems. They adjust the amount of the depreciation charged for the previous year. This is done in order to equal salvage value to anticipated salvage value. Moreover, many companies prefer to use straight-line depreciation in the previous year to adjust the over-depreciated salvage value.

For example, an asset with a useful life of five years has a reciprocal value of one-fifth or 20%. For depreciation, double the rate, or 40%, is applied to the asset’s current book value. Although the rate remains constant, the dollar value decreases over time due to the rate being multiplied by a smaller depreciable base for each period.

Note: The double-declining balance method means higher depreciation expenses at the beginning of an asset’s life and lower depreciation expenses as the asset ages.

#5.Units of Production Method

The units of production formula involve the usage rate of an asset. This can also mean the number of units or cycles of activity an asset will use for goods production over its useful life. An example could be how many miles a car traveled through its cycle of usage. Another is how many acres of land a tractor cultivated with the year of using it.

This method simply estimates the total units an asset will produce or activity it covered over its useful lifetime. Depreciation expenses are then derived from calculating the number of units produced or activity covered per time frame. E.g 1 year period. Another way is to calculate the depreciable amount.

Depreciation Accounting formula

#1. Depreciation Accounting formula for the Straight Line Depreciation method

Annual Depreciation Expense = (Cost of an asset – Salvage Value)/Useful life of an asset. Example:

Example: A company purchases equipment for $50,000, which is the entire cost of the asset. With a useful life of 10 years at the end of its useful life, it costs $10,000, meaning it has a salvage value of $10,000. Using the straight-line method calculate depreciation expenses as the difference between the cost of the asset, its salvage value, divided by the useful life of the asset. That is ($50,000- $10,000) / 10 = $4,000 of depreciation expenses each year. This means the company’s expenses on that asset are $4,000 for each year. until the asset reaches $10,00 of its salvage value in ten years.

#2.Depreciation accounting formula for the units of production method

Depreciation Expense = (Number of units produced/ Life in a number of units) x (Cost – Salvage value)

Examples: The cost of a machine is $50,000, with an estimated total unit production of 150 million and a $10,000 salvage value. In the first quarter of its useful life, the machine produced 5 million units. Calculate the depreciation expense using the formula above:

Depreciation Expense = (5 million / 150 million) x ($50,000 – $10,000) = $1.332

#3.Depreciation Accounting formula for Sum of Years’ Digits Depreciation

Depreciation Expense = Depreciable Cost x (Remaining useful life of the asset/Sum of Years’ Digits

Where depreciable cost = Cost of an asset – Salvage Value

Example: Imagine an equipment that costs $50,000 and has an estimated useful life of 10 years and a $10,000 salvage value. To calculate the sum-of-the-years-digits depreciation:

Depreciation cost = Cost of an asset – Salvage value

Depreciation cost = $50,000 – $10,000 = $40,000

Where the asset has a remaining life of 10 years. The next year, the asset has a remaining life of 9 years, the next year 8, and so on. The remaining life of the asset still remains the remaining life of the asset. Therefore, the remaining life of an asset is divided by the sum of the years. In this example, the asset has a useful life of 10 years. Therefore, the sum of the years would be 1 + 2 + 3 + 4 + 5 + 6 + 7 + 8 +9 +10 = 55 years. The remaining life in the beginning of year 1 is 10. Therefore, the RL / SYD = 10 / 55 = 0.18182.

You can also multiply the RL / SYD number by the depreciating cost to determine the expense for each year. For example, At the beginning of year 2, RL / SYD would be 9 / 55 = 0.1636. 0.1636 x $50,000 = $8,180 expense for year.

#4.Depreciation formula accounting for the declining balance method:

Annual Depreciation Expense = 2 x (Cost of an asset – Salvage Value)/Useful life of an asset Or Depreciation Expense = 2 x Cost of the asset x depreciation rate.

Example: Consider a machine that costs $5,000, with a salvage value of $1,000, a 5-year life, and is depreciating rate of 20% each year. Using the formula above:

Annual depreciation expense= 2 x ( $5,000 – $1,000)/ 5=$9,800 Or

Depreciation expense=2 x $5,000 x 20% = $200,000.

#5.Double Declining Balance Formula

Depreciation Expense =( Asset at the beginning of the yearbook value x Rate of depreciation)/100

Example: Evaluate a piece of land that costs $50,000, with an estimated useful life of 10 years and a $5,000 salvage value. To calculate the double-declining balance depreciation. Did you have to write the beginning book value of the asset at the beginning of year 1 and the salvage value at the end of year 10?

This are examples on how to calculate the depreciation rate:

Expense = (100% / Useful life of asset) x 2

Expense = (100% / 10) x 2 = 2%

Most importantly note: This is a double-declining method so, we multiply the rate of depreciation by 2.

3. Multiply the rate of depreciation by the beginning book value to determine the expense for that year. For example, $50,000 x 2% = $1,000 depreciation expense.

4. Subtract the expense from the beginning book value to arrive at the ending book value. For example, $50,000 – $1,000 = $49,000 ending book value at the end of the first year.

Accumulated Depreciation Accounting

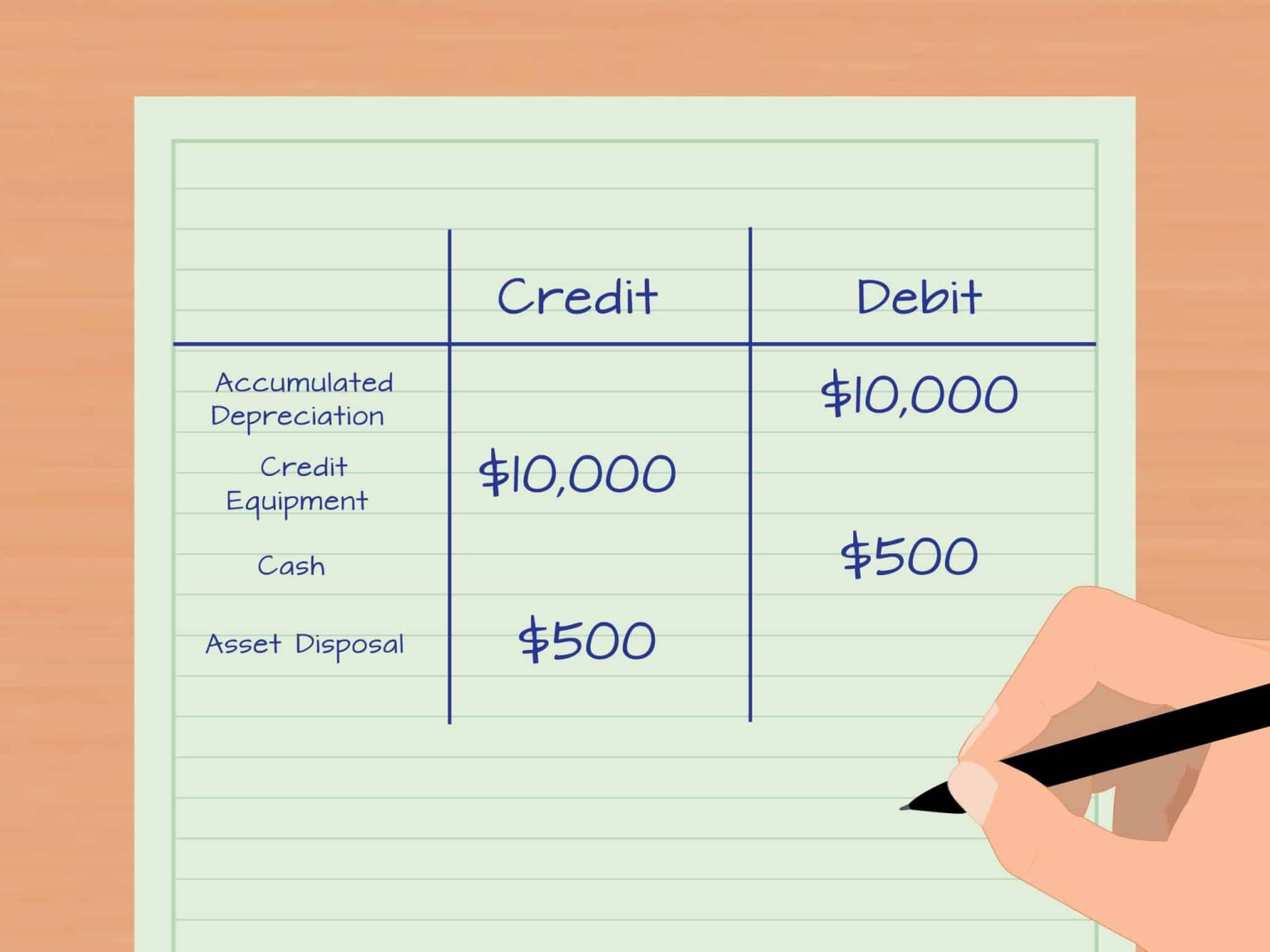

Accumulated depreciation accounting is the overall expenses that have been spent on a depreciating asset over time since the inception of its usage. These asset accounts are otherwise called contra asset accounts- negative asset accounts, which offset the balance in the asset account. Most importantly note that credit to the contra asset account increases its value and debit decreases its value.

However, when a company records depreciation expenses they credit the same amount into the accumulated depreciation account. This makes it easy for the company to give an account for both the cost and the total depreciation of the asset. It also shows the net book value of the asset on the balance sheet.

The matching principle under generally accepted accounting principles (GAAP), states that expenses must correspond to the same accounting period within which the linked revenue is initiated.

With accumulated depreciation accounting, a company must finance a portion of the value of a capital asset over its useful life each year. This means that each year a capitalized asset is in use and initiates profit. However, the costs relating to the use of the asset are on record.

Accumulated depreciation accounting is the overall amount that was depreciated for an asset up to a single point. Each period is added to the opening accumulated depreciation balance, the depreciation expense recorded in that period. The carrying value of an asset on the balance sheet is the difference between its historical cost and the accumulated depreciation.

For example, on January 1, 2015, XYZ Company paid $100,000 for equipment. The equipment is worth $20,000 and has an expected useful life of 8 years. What was the balance of the accumulated depreciation account on December 31, 2017?

($100,000 – $20,000) / 8 = $10,000 in annual depreciation expense

In Conclusion,

So many companies prefer the use of depreciation which allows them to bring down the value of assets over time. Also, they can depreciate expensive assets such as machinery and equipment to extend the cost of that asset and make a profit. Businesses were built to make a profit so companies are able to make a profit from assets that have served them well during their useful life through depreciation. Don’t you think that is awesome? I think it’s one of the most profitable subjects in accounting.

Frequently Asked Questions

Why Are Assets Depreciated Over Time?

Newer assets are usually worth more than older ones. Depreciation is the rate at which an asset loses value over time, either directly through wear and tear or indirectly through the introduction of new product models and factors such as inflation.

How is depreciation recorded in accounting?

Depreciation is calculated by deducting Depreciation Expense from Accumulated Depreciation and crediting Depreciation Expense. At the end of the period, this is recorded (usually, at the end of every month, quarter, or year). Depreciation Expense: This is an expense account, so it appears on the income statement.

Is accumulated depreciation an asset or liability?

On a company’s balance sheet, the accumulated depreciation account is a contra asset account, which means it has a credit balance. It shows up on the balance sheet as a reduction in the reported gross amount of fixed assets.

- BAD DEBT EXPENSE – Definition, Estimation and Calculation

- EARNINGS BEFORE TAX (EBT): Overview, Formular, Importance

- What Is BUSINESS CYCLE?- Definition, Internal and External Causes

- MANAGEMENT ACCOUNTING: A Comprehensive 2021 Guide (Updated)

- SHORT TERM SOURCES OF FINANCE: BEST OPTIONS FOR ANY BUSINESS (+DETAILED GUIDE)