COGM (Cost of Goods Manufactured) describes a schedule or statement that illustrates a company’s overall production expenses over a period of time. COGM is also the complete cost of manufacturing products and transferring them into finished goods inventories for retail sale, as the name implies. So, let’s see the formula for calculating the cost of goods manufactured and how to calculate it.

Cost of Goods Manufactured Formula

The following is the formula for calculating the cost of goods manufactured, along with a summary of what each piece of the formula means:

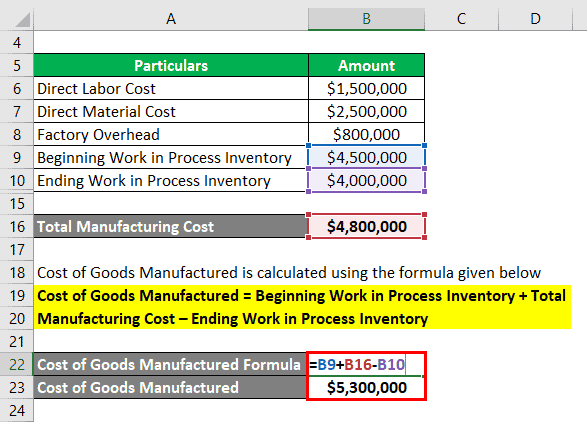

COGM = Beginning work in process (WIP) inventory + Total manufacturing cost – Ending WIP inventory

The formula to calculate the Cost of Goods Manufactured is:

- + Materials used Directly

- + Direct Labor Employed

- Plus Factory overhead

- + Beginning Work in Progress (WIP) Inventory.

- Then deduct ending Work in Process (WIP) Inventory =COGM.

Beginning work in process (WIP) inventory

The beginning WIP inventory formula is the value of products in production that haven’t yet been completed. Companies usually assess WIP inventory at the end of a financial term or at the start of a new one.

For example, your company produced 10,000 things in the previous month, with 6,000 of them only partially completed. The following month’s WIP inventory would be 6,000 items.

Total manufacturing cost: direct materials and labor

The total manufacturing portion of this formula is the direct materials, direct labor, and manufacturing overhead that you pay for during a specific period of time for the creation of items. By adding the beginning raw materials to the purchases made as well as subtracting that amount from the final raw materials, the direct materials can be computed.

Raw materials are stockpiled items that will be employed in the manufacturing of finished goods. For a certain time period, moreover, direct labor refers to how much was paid in labor costs. This is usually so simple to compute and can be done by multiplying the number of hours worked by each employee’s hourly wage. Manufacturing overhead costs are expenses that are incurred regardless of whether or not inventory is produced. Manufacturing overhead costs include things like rent for a factory building and depreciation on equipment.

Ending work in process (WIP) inventory

By adding the initial WIP inventory to the production costs and deducting the cost of goods manufactured, the final WIP inventory can be computed. For example, your company has $5,000 in initial WIP inventory, spends $25,000 on manufacturing costs, and records $23,000 in the cost of products manufactured in a given month.

The following is the formula for calculating the finishing WIP inventory: $5,000 plus $25,000 minus $23,000 equals $7,000

Schedule of cost of goods manufactured

To calculate the cost of goods manufactured you must add your direct materials, direct labor, as well as manufacturing overhead to get your businesses’ total manufacturing cost. Secondly, you will add the beginning work-in-process and subtract the ending work-in-process from the total manufacturing cost to get the cost of goods manufactured.

Unfortunately, it is not as simple as it seems, as each working part has multiple equations within. But the cost of goods manufactured schedule simplifies this process. The schedule also reports the total manufacturing costs for the period that were added to the work‐in‐process (WIP). It then adjusts these costs for the change in the WIP inventory account to arrive at the cost of goods manufactured. Below is a breakdown of this schedule.

COGM = Beginning WIP Inventory + Total Manufacturing Cost – Ending WIP Inventory

The Cost of Good Manufactured Schedule

| Direct Materials | (Beginning Raw Materials + Purchases – Ending Raw Materials) |

| + Direct Labor Costs | |

| + Manufacturing Overhead | |

| = Total Manufacturing Cost | (Direct Materials + Direct Labor + Manufacturing) |

| + Beginning Work in Process (WIP) Inventory | |

| – Ending WIP Inventory | |

| = Cost of Goods Manufactured | (Total Manufacturing Cost + Beginning WIP – Ending WIP) |

How to Calculate Cost of goods manufactured

The cost of goods manufactured (COGM) is a measure that determines if production expenses are excessively high or low in comparison to revenue. The equation also analyzes the production expenses associated with goods completed over a given time period. In other words, the overall cost of converting inventory into a finished product for a corporation.

This can be more clearly seen in a T-account. For example, let’s say that a company that manufactures furniture incurs the following costs:

- Direct Materials: $100,000

- Direct Labor: $50,000

- Manufacturing Overhead: $60,000

- Beginning WIP Inventory: $10,000

- Ending WIP Inventory: $30,000

| Work in Process (WIP) Inventory | |

| Beginning Balance 10,000Direct Materials 100,000Direct Labor 50,000Manufacturing Overhead 60,000 | 190,000* COGM |

| Ending Balance 30,000 |

With this information, we can solve for COGM, which is on the credit side of the WIP Inventory T-Account. COGM = 10,000 + 100,000 + 50,000 + 60,000 – 30,000 = $190,000*

COGM example 1

Zink Factory starts the year with a $4,000 inventory cost, which is the beginning WIP inventory. The manufacturer spends $10,000 on direct materials, $6,000 on direct labor, and $3,000 on manufacturing overhead throughout the course of the year. The overall production expenses for the factory are $19,000 when they add these three numbers together. The corporation has $5,000 in ending WIP inventory left at the end of the year. The Factory calculates its manufacturing costs as follows:

$4,000 + $19,000 – $5,000 = $18,000

So, for the calendar year, the total monetary amount of inventory completed and moved to the finished goods account was $18,000.

COGM example 2

At the conclusion of last year, Steel Furniture Store had $100,000 in finished items. This quantity is carried forward to the start of the current year and represents the company’s initial WIP inventory. Moreover, the store spends $40,000 on furniture supplies, $50,000 on employee pay, and $30,000 on rent, utilities, and other overhead costs throughout the course of the year. The furniture company also estimated that $60,000 in inventory needed to be completed at the end of the year (ending WIP inventory).

Steel Furniture Store calculates its cost of goods manufactured for the year as:

$100,000 + ($40,000 + $50,000 + $30,000) – $60,000 = $160,000

The cost of goods manufactured formula shows Steel Furniture Store was able to complete and put up for sale $160,000 worth of furniture from the work in process inventory during the year.

How to Find Cost of Goods Manufactured

Cost of Goods Manufactured Equation

The overall manufacturing expenses, including all direct materials, direct labor, and factory overhead, were added to the beginning work in process inventory and subtracted from the ending products in-process inventory to get at the cost of goods manufactured equation. Only the cost of goods finished during the period will be left after applying this calculation.

Another way to think of it is that the cost of goods completed equals the quantity of inventory transferred from the goods in progress account to the finished goods account by the end of the quarter. The total cost of goods manufactured is also a factor in calculating the cost of goods sold. Consider the following scenario.

Steelcase is a Midwest-based furniture company with a factory and offices. So, let’s assume that at the start of the quarter, they had $100,000 in finished products inventory. During that time, it spent $50,000 on chair and table materials, $125,000 on employee pay, and $65,000 on rent and utilities.

Steelcase executives calculated the ending items in process inventory to be $75,000 using the equivalent units of production computation.

For the period, the total cost of products made would be $265,000 ($100,000 + $50,000 + $125,000 + $65,000 – $75,000). Steelcase was able to finish $265,000 of furniture over time and move it from the work in process to the finished goods account before the conclusion of the quarter.

Cost of Goods Manufactured Statement

The income statement is the cost of goods sold, while the figure is supported by the statement of the cost of goods manufactured. The overall production cost and the cost of goods manufactured are the two most essential statistics on this statement. Avoid conflating the words total manufacturing cost and cost of goods manufactured, as well as the terms cost of goods sold.

Manufacturing as a whole. The cost of all resources used in manufacturing during that period is included (meaning, the direct materials, direct labor, and overhead applied). The cost of all items finished during the time is included in the cost of goods manufactured. The Company adds the total manufacturing costs to the beginning work in process inventory and subtracts from the ending work in process inventory. The cost of goods sold is the total cost of all items sold during the period. This includes the cost of goods manufactured as well as the beginning and ending finished goods inventories. The cost of products sold is the only time product expenses are expensed, and it is presented as an expense on the income statement.

Conculsion

In general, having a schedule or statement for the Cost of Goods Manufactured is significant. Since it informs companies and management about whether production costs are too high or too low in relation to sales.

For example, if a company received $1,000,000 in sales revenue but spent $750,000 on CGS, they may want to look for ways to cut their manufacturing expenses in order to boost their gross margin %. In contrast, if another firm produced $800,000 in sales revenue but only spent $400,000 on COGS, even if their sales were smaller, their gross margin percentage would be much higher, making the latter company significantly more profitable.

As a result, management can examine these areas more thoroughly to make any necessary adjustments or changes. This also helps to maximize the company’s net income by having a general picture of what the company is incurring. This could be in terms of manufacturing costs in all of its specific components of materials, labor, as well as overhead.

Frequently Asked Questions

What is the schedule of cost of goods manufactured?

To compute the cost of goods manufactured, the cost of goods manufactured schedule presents the total manufacturing costs for the period that were added to work in process as well as adjusts these costs for the change in the work in the process inventory account.

What are goods manufactured?

The cost of goods manufactured is a calculation of a company’s total production expenses over a given period of time. It’s also the whole cost of producing items, turning them into inventory, and putting them on the market.

How do you find the cost of goods manufactured?

To calculate a product’s per-unit cost, you must first compute the overall manufacturing cost of all the products produced within the time period. The estimated value is then divided by the number of items. The final amount is the manufacturing cost of one item.