How can you get a quick overview of the financial information about your company at any given time? Your balance sheet. It contains information on your debts, assets, and shareholders’ equity value. It shows your company’s overall financial state. You must understand your balance sheet for this reason. It’s called a ‘balance sheet’ because your assets should always equal your liabilities plus your shareholders’ equity. Spending some time getting to know your balance sheet is worthwhile. By interpreting it, you can identify potential risks to your company’s financial health, such as low cash balances or excessive debt-to-cash flow ratios. The amount of retained earnings is one key sign of the company’s future growth and financial health. Are retained earnings recognized as an asset or liability on the balance sheet?

Please read through it as I explain retained earnings, whether they are an asset or liability, how to calculate them, some differences between profits, and some key examples.

Key Points

- Retained earnings (RE) are the net income left over for the business after it has paid dividends to its shareholders.

- The balance sheet shows retained earnings as neither an asset nor a liability. Rather, they fall within the shareholders’ equity category.

- On your balance sheet, retained earnings are in the equity column beneath liabilities.

- Retained earnings provide funds for functioning activities, help finance plans for future growth, help in debt management, and ensure the shareholder’s value.

What Are Retained Earnings?

Retained earnings are the net income of a business after dividends have been paid out to shareholders and/or owners.

Suppose there’s a positive balance instead of a negative one (which might be a bad sign regarding the business’s financial health). In this case, a company has several ways to use the surplus income besides dividing it (in part or completely) as dividends to shareholders, according to the number of shares each holds. This includes:

- Setting up mergers, acquisitions, or partnerships

- Doing share buybacks

- Investing the money in business growth

- Funding a product launch

- Taking care of operating expenses

- Repaying debt

It allows you to use a formula to measure how much money you’ve accumulated on an income statement. They are included in the equity portion of a company’s balance sheet. Other portions contain the overall obligations and assets. People sometimes wonder if retained earnings are assets because they can be utilized to purchase them.

What Is the Difference Between Retained Earnings and Dividends?

Dividends can be distributed in cash or stock. Both forms of distribution reduce retained earnings. Paying dividends leads to a cash outflow, recorded in the books and accounts as net reductions. As the company loses ownership of its liquid assets through cash dividends, its asset value on the balance sheet is reduced, impacting RE.

Nevertheless, a portion is transferred to common stock due to stock dividends despite no cash outflow. For example, if a company pays a dividend of one share for each share owned by investors, the price per share will drop to half. This is because there will be exactly twice as many shares. When a stock dividend is announced, the market price of each share changes based on the dividend percentage because the company has not created any value.

The market price is automatically adjusted; therefore, the share increase may not affect the firm’s balance sheet. However, it will affect the RE since it lowers the per-share valuation in capital accounts.

A business that prioritizes growth can use RE to fund operations like marketing, R&D, working capital needs, capital expenditures, acquisitions, and other cash-demanding activities. As a result, it can decide to pay no dividends at all or very little. Such companies have had high retained earnings over the years.

A maturing business typically has low RE because it doesn’t have many options or high-return projects to allocate the excess cash. Instead, it may prefer to distribute dividends.

Are Retained Earnings Recognized as an Asset or Liability on the Balance Sheet?

The balance sheet shows retained earnings as neither an asset nor a liability. Rather, they fall within the shareholders’ equity category.

The total net income a business has kept and chosen not to pay out as dividends to its shareholders is known as retained earnings. They result from the company’s cumulative profits. An organization can choose to keep its profits for internal reinvestment or to pay a portion of them as dividends to shareholders when it makes a profit.

The balance sheet represents the total shareholders’ equity, which comprises share capital, additional paid-in capital, retained earnings, and accumulated other comprehensive income. A company’s owners’ claim to its assets following the settlement of all debts is represented by its shareholders’ equity.

Since they represent the fraction of profits reinvested in the business rather than dispersed to shareholders, they are essential to shareholders’ equity. They show the business’s potential for expansion and its capacity to profit.

Although retained earnings are not classified as assets or liabilities, they indirectly impact the company’s financial health. Specifically, high retained earnings indicate the company’s profitability and potential for future growth, while low or negative retained earnings may point to unprofitability or financial difficulties. Retained earnings are important in evaluating a company’s financial position and performance, even though they are not explicitly classified as assets or liabilities.

Where Can I Find Retained Earnings on the Balance Sheet?

On your balance sheet, retained earnings are in the equity column beneath liabilities. Since net income as shareholder equity is essentially a firm or corporate loan, it is a liability. The company can pay dividends to shareholders or reinvest shareholder money into business expansion. Prioritizing the accumulation of retained earnings is a wise financial move for any company aiming for long-term expansion.

I have provided a balance sheet below illustrating an example of shareholder equity with retained earnings. Keep in mind that shareholders’ equity and stockholders’ equity are synonymous.

ABC Company

Balance Sheet (as of December 31, 2023)

Assets:

—————————

Cash and Cash Equivalents $100,000

Accounts Receivable $150,000

Inventory $200,000

Property, Plant, and Equipment $1,000,000

Total Assets $1,450,000

Liabilities:

—————————

Accounts Payable $50,000

Short-term Loans $100,000

Long-term Loans $500,000

Total Liabilities $650,000

Shareholder Equity:

—————————

Common Stock $300,000

Retained Earnings $500,000

Total Shareholder Equity $800,000

Total Liabilities and Shareholder Equity $1,450,000

In this example,

- Assets include cash, accounts receivable, inventory, property, plant, and equipment, totaling $1,450,000.

- Liabilities include accounts payable and short-term and long-term loans totaling $650,000.

- Shareholder equity comprises common stock and retained earnings totaling $800,000. Retained earnings represent the company’s cumulative profits that have not been distributed to shareholders as dividends.

- The total liabilities and shareholder equity sum up the total assets, maintaining the balance sheet equation: Assets = Liabilities + Shareholder Equity.

Read also: What Is A Trial Balance In Accounting?

Retained Earnings Formula and How to Calculate It

Retained earnings accounts give you a running total of the money your business has managed to hang onto since its founding. Your RE decreases when you pay dividends to shareholders or reinvest in the firm. Earned savings often increase as your revenues do. If your business has had exceptionally difficult times, or if you are trying to build it up during its inception years, it can end up with cumulative debts and a negative balance.

Using the retained earnings formula is straightforward:

Retained Earnings = Current Retained Earnings + Profit or − Loss − Dividends

Good accounting software, such as Wave’s solution for small businesses, can help you with these calculations.

Your current retained earnings are simply whatever you calculated during your last financial period. The same goes for the net profit or loss, calculated by the month, quarter, year, or accounting period. Whatever dividends you paid shareholders for the period will reduce the amount shown in the statement of RE.

For example, if you had $2,000 in current retained earnings and $8,000 in monthly product sales and chose to distribute $2,000 in dividends to the company’s three shareholders, you would still have $4,000 in retained earnings ($2,000 + $8,000 – $6,000 = $4,000).

After every accounting period, retained earnings have to be recorded. Comparisons of retained earnings between accounting periods can help you make strategic decisions in the future by providing you with important information about the financial health of your business.

How to Interpret the Results of Retained Earnings Calculation

A company’s retained earnings reflect its profit once all dividends and other obligations have been met. If a company’s retained earnings are positive, this means that the company is profitable. If the business has negative RE, it has accumulated more debt than earned.

It’s critical to consider the entire business state while evaluating retained earnings. For instance, a corporation might be expected to have negative retained earnings during its early years of operation. This is particularly true if the business was founded primarily with the support of investors or took out loans. Negative retained earnings, however, could be a sign that a company needs funding if it has been in operation for a while and is not successful enough.

When interpreting the RE of a company, you should also consider the following factors:

- The company’s age: Senior companies are expected to have higher retained earnings because they have had more time to accumulate them.

- The company’s dividend policy: A company may have less RE if it has pledged to pay dividends regularly. Many publicly traded companies pay out greater dividends than privately held companies.

- The company’s profitability: Retained earnings are generally higher for more profitable companies.

- The company’s seasonality: Companies may need to set aside retained earnings during their successful times in sectors like retail, where activity is quite seasonal. This implies that an organization might experience positive and negative retained earnings during its accounting periods.

What Does Negative Retained Earnings Mean?

Generally speaking, a company with a negative retained earnings balance would signal weakness because it indicates that it has experienced losses in one or more previous years. However, it is more difficult to interpret a company with a high RE.

Can You Take Money Out of Retained Earnings?

Yes, you can withdraw funds from retained earnings; however, there are limitations and tax implications to consider. Dividends from RE can be paid to owners or shareholders; however, doing so may impede the expansion of the business. Reinvesting RE into the business is a common practice among high-growth entrepreneurs.

Additionally, you can transfer gains from RE—that is, credits from one account to another—to another person’s capital account. The payment debits the capital account and credits the cash or bank account.

To withdraw money from retained earnings, you can:

- Make a credit entry to the dividends payable account

- Declare that dividends will be paid

- Make a debit entry to the retained earnings account

The balance sheet’s equity section includes a line item called retained earnings that contributes to the overall equity figure. Unless they are disbursed as a salary, dividend, or bonus, RE is tax-free and may be held in a separate account. The tax implications of paying dividends vary.

Practical Examples of Retained Earnings

The following are examples of retained earnings at the end of a company’s accounting period:

Examples 1:

Sam Logistics begins a new accounting period with $100,000 in retained earnings. Over the accounting period, the company brings in $25,000 in net income. At the end of the accounting period, the company’s board decides to pay its shareholders $5,000 in dividends. The formula for the company’s retained earnings at the end of the accounting period would be as follows: $100,000 + $25,000 – $5,000 = $120,000. This means the company’s total retained earnings are $120,000 for the accounting period. This amount will be carried over to the new accounting period and can be used to reinvest in the company or to pay future dividends.

Example 2

Let’s assume that Sam Logistics has $10,000 in RE at the start of a new accounting period. During the accounting period, the business reported a $25,000 net loss. By the end of the accounting period, the company cannot pay its stockholders dividends. Retained earnings for the corporation would be calculated as follows: $10,000 – $25,000 = $15,000.

Financial statements display negative sums in parentheses. Due to this negative balance, the company will not have any money to reinvest, which will roll over to the following accounting period. Until the company’s retained profits account is positive again and it has sufficient net income, dividend payments should be delayed. If a company’s RE is negative, it shouldn’t pay dividends.

Why Are Retained Earnings Important?

Retained earnings are a critical component of a company’s financial health. They represent the portion of profits kept within the company for future use. It also plays a vital role in financing a company’s operations, funding growth initiatives, paying dividends to shareholders, and clearing loan outstandings.

#1. It Provides Funds for Functioning Activities

One of the main purposes of retained earnings is financing a business’s continuing operations. By holding onto its earnings, an organization can guarantee that it has enough money to pay for regular charges like rent, salaries, and other running expenditures. This can lessen a company’s dependency on outside funding sources like loans or equity financing and help it become more financially stable.

#2. It Finances Plans for Future Growth

RE can potentially finance future expansion plans. These endeavors include R&D, new product lines (CAPEX), and market expansion. Investing in these growth prospects allows a company to avoid depending on external financing, which can be more costly or challenging to secure.

It can additionally be utilized to repurchase shares from the secondary market or distribute dividends to shareholders. Some businesses do not pay dividends, but those with the option to finance these payments with them do. Offering a consistent revenue stream and the potential to boost a company’s share price, dividends can be a compelling attribute for investors.

#4. Debt Management

Retained earnings can also be used to reduce reliance on external debt. By funding projects internally, companies can lower their debt levels, decreasing financial risk and interest expenses. This improves the company’s overall financial health and creditworthiness.

#5. Flexibility

Retained earnings offer flexibility in financial management. Unlike debt, which comes with repayment obligations, and dividends, which can signal financial commitment to shareholders, retained earnings allow companies to adjust their investment and distribution policies according to current needs and market conditions.

What Is the Difference Between Profit and Retained Earnings?

Profit is not the same as retained earnings. While both are necessary to assess a company’s financial standing, they don’t always show the same thing. Profit is the revenue derived from selling goods and services and represents the company’s bottom line. Typically, it refers to net income, the total revenue minus operating expenses (such as salary and overhead). The revenue from the sale of commodities minus the cost of those things is known as gross income.

On the other hand, RE is the portion of the profit saved to make shareholder dividend payments or for other future uses, such as growing the company and/or product lines or paying off debts. Shareholders might see value in using the money for things other than immediate cash dividends if invested in something likely to become highly profitable and pay even bigger dividends.

Is Retained Earnings Cash on Hand?

No, they are not cash on hand.

How to Prepare a Retained Earnings Statement

Companies usually publish statements quarterly or yearly. However, you can create one at any time. Startups might post them more often because they hold crucial information for lenders and investors. I have provided a comprehensive checklist for preparing a retained earnings statement for your business.

Businessyield-Retained-Earnings-Statement-Checklist

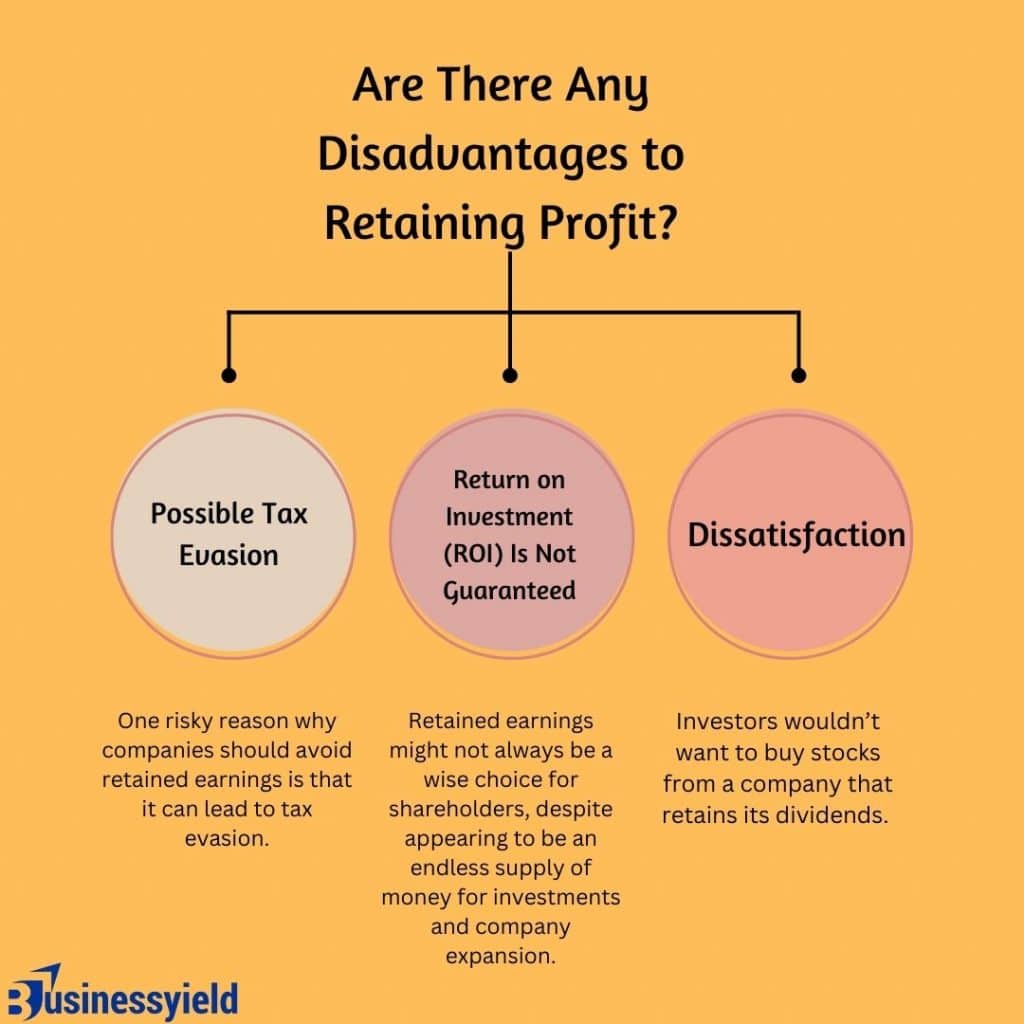

Are There Any Disadvantages to Retaining Profit?

Yes. While, on the surface, retained earnings seem like a good way to increase company value and save money for reinvestment purposes, it’s not always the most efficient option. I have put together some of the limitations of retained earnings:

#1. Possible Tax Evasion

One risky reason why companies should avoid RE is that it can lead to tax evasion. Some might attempt to ease the tax burden by keeping profits. Some shareholders who don’t have an immediate need for dividends might vote against their distribution to avoid paying income tax. Once the company’s stock value increases through profit retention, the shareholders could decide to sell the business at a higher price or withdraw dividend distributions in the future. Moreover, a company that attempts to retain its earnings and gets caught will have to pay penalties later.

#2. Return on Investment (ROI) Is Not Guaranteed

Retained earnings might not always be a wise choice for shareholders despite appearing to be an endless supply of money for investments and company expansion. It isn’t free, but it is an affordable financing option that could provide the business with emergency cash flow.

Shareholders who choose to forego a larger cut in earnings in favor of smaller payouts are missing out on opportunities. Furthermore, a company’s return on investment (ROI) will determine whether or not its shareholders decide to withdraw their funds and invest elsewhere.

#3. Dissatisfaction

Investors wouldn’t want to buy stocks from a company that retains dividends. They will need to see if the company has a steady stream of dividends, primarily if it is known to be profitable. Not all shareholders are willing to withhold a claim over their profits. Suppose the investors do not see any gains in their investments.

In that case, they will likely look for other companies that generously award dividends—ones that don’t keep the profits to themselves and distribute them to all shareholders instead.

Who Makes the Decision About the Use of Retained Earnings?

Company management usually decides whether profits are used to pay shareholder dividends or set aside for RE. However, since the firm owners decided to buy common stock, shareholders may contest this with a majority vote. Regarding retained earnings, shareholders frequently find themselves on the same side as company management.

They both may see them as working capital to pay off high-interest debt or invest in growth that will make the company even more profitable given some more time. If money is paid in dividends, it is out of the company and off the books. If it is kept as retained earnings, it remains on the books and is available for use within the business.

It’s common practice to strike a balance between keeping some profits as RE and paying out some of the profits as dividends.

Bottom Line

Retained earnings are an essential aspect of a company’s financial statements. Understanding them is crucial for business owners, investors, and other stakeholders.

It shows how profitable a business is and how well-positioned it is to finance expansion plans or dividend payments. By examining retained earnings, stakeholders can learn important information about a company’s long-term prospects and financial health.

Investors should be aware of the variables that may affect RE. Considering these factors, they can choose wisely whether to invest in a particular company.

Have a happy investment, and invest wisely!

Similar Posts

- HOW TO RETAIN EMPLOYEES: Top Strategies Explained

- 6 Biggest Challenges To Small Business Growth

- RETENTION STRATEGIES:15+ Proven strategies in 2023