The crucial role that insurance broking play in assisting clients in locating the coverage that best meets their needs makes the industry truly rewarding.

Insurance brokers help customers choose insurance policies, and their work is rewarding. An insurance broker may operate from home or an office. Additionally, you must fulfill some educational and licensing requirements before you can work as an insurance broker.

In this article, we go over what insurance broking is, what an insurance broker does, what it takes to become one, how significant the position is in the insurance industry, how to become an insurance broker and the educational and licensing requirements for insurance brokers.

What is Insurance Broking?

Insurance broking is the art or profession of mediating an insurance sale transaction. Additionally, it is the action of an insurance broker; in the exchange or transaction.

Who Is an Insurance Broker?

An insurance broker’s primary function is that of a middleman. In order to help people and businesses find insurance policies that address their specific needs, they serve as a middleman between buyers and insurance companies. These professionals have the option of working alone or with an insurance brokerage company.

Additionally, compared to agents who work directly for insurance carriers, insurance brokers can provide customers with more coverage options because they are not restricted to a single insurer. As a result, they have the freedom to place policies with various providers based on the state of the market, giving their customers the best protection possible.

Brokers offer that service and are paid in a number of ways, including commissions, fees, or payments from the exchange itself.

What Do Insurance Brokers Do?

Insurance brokers assist people and businesses in locating insurance plans that best suit their client’s needs. They are professionals with training in insurance and risk management strategies. They might specialize in a single kind of insurance or deal with a variety of them, like home, life, and health insurance.

Furthermore, Insurance brokers must be knowledgeable of the insurance broking business and persuasive to explain complicated insurance terms to customers, regardless of the type of insurance they sell. Before they are allowed to sell policies, brokers are required to hold licenses in particular insurance fields.

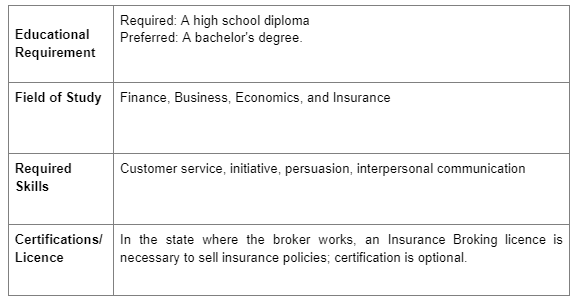

The basic qualifications for insurance brokers are listed in the table below.

How to Become an Insurance Broker

You must be familiar with the entire insurance market to succeed as a broker. Successful brokers frequently have a broader understanding of the industry than captive and independent agents. The steps to becoming an insurance broker are listed below.

Step 1: Comply with the minimal requirements.

Similar to any profession, becoming an insurance broker has certain minimum requirements that one must fulfill. These may differ by region, but in the US, prospective brokers typically need to:

- Age requirement: 18 or older (the minimum age to apply for a license in most states)

- possess the ability to complete a background check

- Do not have any felony or fraud charges

- Make sure to meet up on all your state or federal income taxes.

- Do not owe child support that is overdue

Step 2: A Bachelor’s Degree, though not necessary, could improve your chances of landing a job with an insurance brokerage company.

You can acquire the necessary background in finance, accounting, business law, and marketing through degree programs in business administration or economics.

Furthermore, you might also think about pursuing a bachelor’s degree in risk management and insurance since they devote entire courses to explaining the fundamental ideas and concepts underlying life, health, and property insurance, in addition to developing fundamental business skills.

Step 3: Include an internship in your training as an insurance broker.

There are internship opportunities with insurance companies through some bachelor’s degree programs in risk management and insurance. You will observe and take part in the company’s internal operations while you are an intern.

Consequently, you might be required to submit a written report summarising the experience while the employer gives your instructor a written evaluation.

Step 4: Get an Insurance Broking License

Licenses are available for personal, life, casualty, and property insurance. You will require an insurance broking license from the state you work in.

Step 5: Find a Job

At a brokerage firm, you can anticipate beginning your career either as a broker’s assistant or at the customer service desk. As you become more accustomed to the market and the operations of your employer, you can advance to the position of a customer service representative.

Positions as a department supervisor or branch manager may become available if you exhibit initiative, skill, and leadership.

Step 6: Become a Certified Insurance Broker

Consider getting certified in an area of insurance where you have experience if you want to advance your career and your professional development. For independent brokers, the National Alliance for Insurance Education and Research provides some voluntary certifications, like

- Certified Risk Manager (CRM),

- Certified Insurance Service Representative (CISR), and

- Certified Insurance Counselor (CIC) (CRM)

- A Health Insurance Association (HIA) certificate from America’s Health Insurance Plans is available to those with an interest in the medical field (AHIP).

- The Certified Financial Planner (CFP) designation is available from the Certified Financial Planner Board of Standards if you’re interested in obtaining a financial planning credential.

- Three years of financial planning experience are required, as well as passing an exam covering general planning principles, risk management, benefits planning, and tax.

Step 7: Get a broker’s bond

The majority of US states require insurance brokers to obtain a broker bond before they can sell policies, according to the Independent Insurance Agents and Brokers of America (IIABA). A specific kind of surety bond called a “broker bond” is intended to hold brokers responsible for their deeds. It also aids in defending the populace against potential fraud.

What are the Different Types of Insurance Brokers?

The three main types of insurance brokers are:

#1. Direct Broker

This is an insurance broker who arranges insurance for his clients while holding a license from the appropriate authority to act for compensation.

Functions of a direct broker.

- to learn more about the client’s business and risk management practices.

- to become knowledgeable about the client’s operations so that he can explain them to an insurer and other parties.

- to offer guidance on suitable insurance terms and coverage.

- to keep up-to-date knowledge of the various insurance markets.

- to promptly carry out a client’s instructions and send written acknowledgements and updates.

- to help customers pay premiums as required by Section 64VB of the Insurance Act of 1938.

#2. Reinsurance Broker.

This is an insurance broker who has registered to arrange reinsurance business for his clients with insurers or reinsurers. Additionally, he offers risk management services, claims consulting, and other services permitted by the regulations.

Functions of a reinsurance broker.

- Learn about the client’s business and risk retention practices.

- To aid the insurer or others, keep accurate records of the insurer’s business.

- Provide reinsurance with consulting and risk management services. choosing and advising a particular insurer or group of insurers on behalf of the client.

- Follow a client’s instructions promptly, and send written acknowledgments and progress updates.

- Select insurers and international insurance brokers with caution and diligence, taking into account their respective security ratings, and establish respective responsibilities when engaging their services.

#3. Composite Broker.

A composite broker is an insurance broker who currently holds a license from the relevant authority to act for compensation and arranges the insurance and/or reinsurance on behalf of his clients.

Functions of a composite broker.

- Any one or more of the tasks listed under the responsibilities of the direct broker or the reinsurance broker above must be performed by a composite broker.

- They must adhere to a set of standards and requirements established by the IRDA.

- They must uphold a specific code of conduct and keep earnings and insurance money in separate accounts.

- According to the regulations published by the IRDA, a composite broker is required to maintain a solvency margin.

Is Being an Insurance Broker Profitable?

If you’re wondering whether being an insurance broker is a good career choice, it’s helpful to consider the pros of this professional opportunity as you make your decision. Here are a few you can think about:

#1. There is a potential for growth

The growth potential is one advantage of working in the insurance industry. Research shows that opportunities for insurance brokers will increase by 5% by the next decade, which is good news. This represents a faster growth estimate than the national average for all occupations.

#2. Work remotely

Insurance brokers often work from home, although they may also meet with clients and potential leads in person. Many insurance agents set their own work schedules, which provides a great deal of flexibility for their day-to-day lives.

Consequently, the idea of working from home is appealing to many people.

#3. A large earning potential

Your earning potential is determined by your work ethic and willingness to put yourself out there. Insurance brokers can maintain a passive income stream from policy renewals.

#4. Opportunity to provide benefits

By offering insurance opportunities to people, brokers have the opportunity to provide a great benefit to their clients. Health insurance provides for health expenses and medical treatments, while auto and home insurance protects your valuable possessions.

#5. Minimal requirements:

A state licensing exam is required for insurance brokers, but there aren’t many other entry requirements. Although some employers might prefer it, a college degree is not necessary for this position. It is not necessary to have prior experience because most brokers learn on the job and through training.

What Insurance Brokers Make the Most Money?

You have a variety of job options in the insurance industry, depending on the type of insurance you want to cover. The highest-paid insurance brokers in the industry are those in the following categories:

- An Insurance Consultant

Salary range: $100,000-$180,000 per year

An insurance consultant is a person who offers clients accounting and risk-assessment guidance. Your duties are to collect and analyze data and provide a solution to the company or client with whom you are consulting.

Qualifications for a career as an actuary include several years of experience in the actuarial field.

- A Life Insurance Actuary

Salary range: $70,000-$130,000 per year

A life insurance actuary helps determine pricing for life insurance policies to minimize cost and risk. Their duties include risk assessment, performing financial analysis, and creating reports.

Qualifications for becoming an actuary typically include a bachelor’s degree in mathematics or actuarial science.

Who Is An Insurance Agent?

An insurance agent is one who represents one or several insurance companies and sells their policies for a commission. They can either work full-time in insurance sales for an agency or as independent contractors.

Therefore, their job is to represent the insurance company in the transaction while also helping customers find the right coverage.

What Is The Difference Between An Insurance Agent and an Insurance Broker?

- Agents speak on behalf of insurance providers. Brokers speak for their customers.

- Agents do not have a fiduciary duty to their clients; brokers do. As a result, agents do not offer guidance throughout the process as brokers do.

- Agents can go into great detail about the coverage, but ultimately it is up to the person or company buying the coverage to determine whether the insurance product suits their needs.

- Since they are employed by the insurer, agents can bind coverage, but brokers cannot. The broker must obtain a binder from an insurance agent or the insurance company when a customer is prepared to buy from them.

- Brokers are not subject to the same sales requirements as agents, who may be required to promote certain insurance products.

Who Pays The Broker in Insurance?

There are a few ways that an insurance broker can get paid and they are as follows:

#1. Commission:

An insurance broker is paid a commission by the insurance company where they place your insurance. Each business determines its commission rate, which is then pre-approved by each state.

#2. Consultancy fee:

In many states, a broker may also charge a broker fee in addition to a commission. Usually, the only parameters for this fee are that it’s reasonable, disclosed, and typically has to be accepted with a signature. Some insurance brokers charge a fee for all new business, renewal business, and many service transactions.

- TOP INSURANCE COMPANIES IN TEXAS IN 2023

- The Best Life Insurance Companies in the USA

- Private Placement: Definitions, Life Insurance And Investment Offers (+ How it works)

- WHAT IS A CREDIT BUREAU AND HOW DOES IT WORK?

- FORBEARANCE MORTGAGE: Meaning and How It Works