There are lots of retirement plans to choose from as a working-class individual. However, if you are self-employed, you are possibly going to select either the 403(b) vs 401(k) plan as your main retirement plan. However, there are some major similarities between them. But there are also some differences we need to look into. This article will reveal the 403(b) vs 401(k) contribution limits. We will also discuss the advantage and disadvantages of 403(b) vs 401(k). Afterward, we will get to know which is better between both.

As we are about to dive into the topic, let us first discuss what they mean separately. Now sit, relax, learn, and enjoy. Shall we?

What Is A 403(b) Plan?

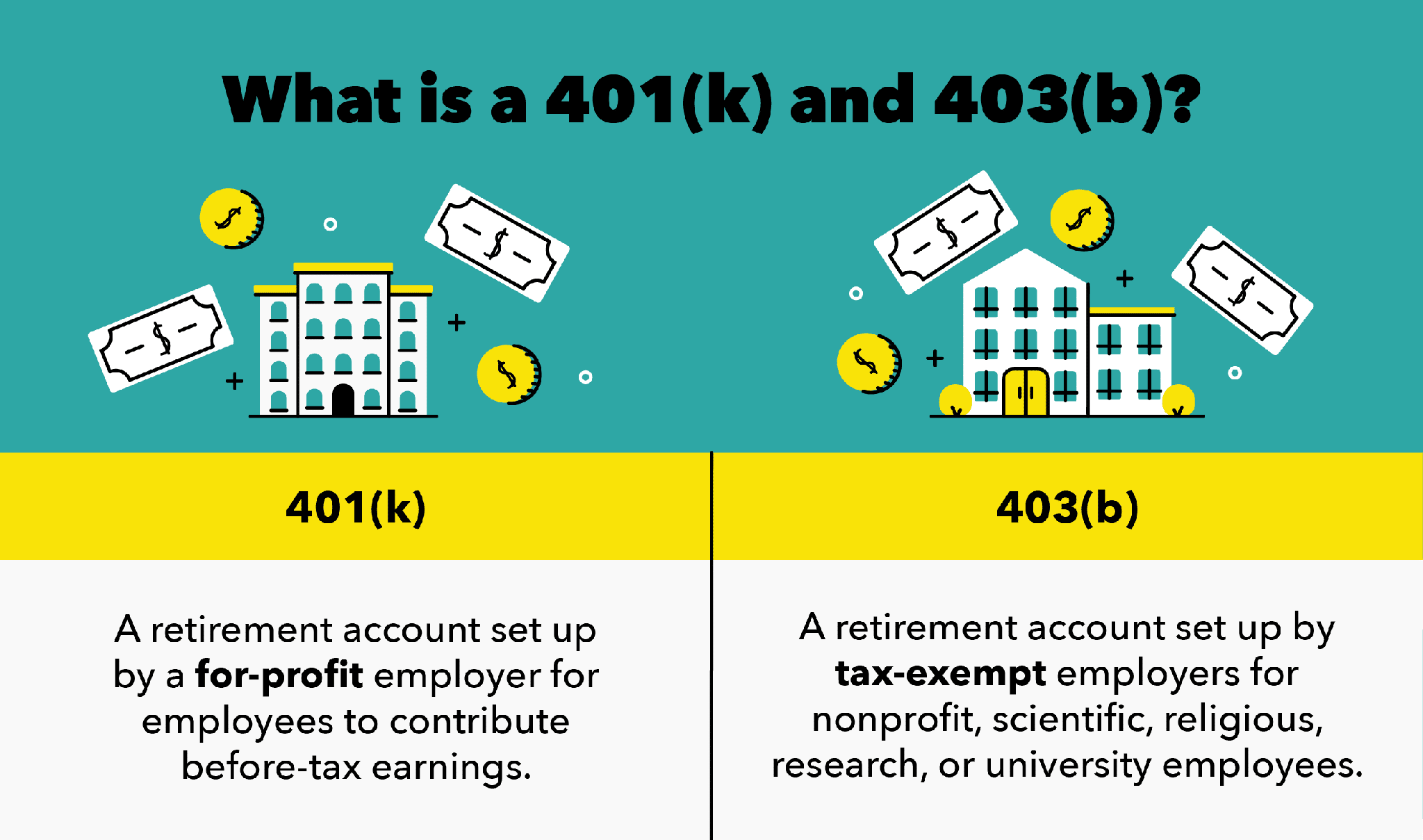

A 403(b) plan is a retirement plan for several employees of public schools and tax-exempt companies. Individuals involved are teachers, school administrators, professors, government employees, among others.

The 403(b) plan is related to the 401(k) plan. Each allows employees a tax-advantaged means to save for retirement. However, investment options are usually more limited in a 403(b), and 401(k)s are only open to private-sector employees.

What Is A 401(k) Plan?

A 401(a) plan is a Retirement plan available for employees working in a government agency, nonprofit organization, and government educational institution. Qualified employees who participate in this plan mostly work as teachers, administrators, and support staff. The 401(a) plan attributes are technically similar to that of 401(k), which are more inherent in profit-based organizations.

The 401(a) usually does not allow an employee to contribute to the 401(k) plans. However, if the employee leaves the organization, he has the right to transfer his funds from the 401(a) to his 401(k) plan.

403(b) vs 401(k) Contribution Limits

Everything in life has its limit. Likewise, the 403(b) vs 401(k) contributions limits. Each plan has its limits. Let us take a brief look at their contribution limits.

Contribution Limits For 403(b)

403(b) plans are like 401(k)s in many ways, and one similarity they have in common is that they enable you to make large contributions toward retirement.

For 2020, $19,500 was the contribution limit for employees in a 403(b) plan, and it was the same in 2021. For both 2020 and 2021, people in their fifties and older can make a catch-up contribution of $6,500. Hence, bringing the total eligible contribution limit to $26,000.

Additionally, some employers add into their plans an additional catch-up contribution option. This allows those who have 15 years and above of service with the organization to make an additional contribution of up to $3,000.

Contribution Limits For 401(k)

The contribution limit to a 401(k) for 2021 is the same as 2020 at $19,500 for those younger than age 50. Those at age 50 and older can add an extra $6,500 per year in “catch-up” contributions. Hence bringing the total 401(k) contributions for 2021 to $26,000. Contributions to a 401(k) are generally due by the end of the calendar year.

A typical 401(k) is an employer-based retirement savings account. It is funded through payroll deductions before taxes have been taken out. Those contributions lower the taxable income and help cut the tax bill. For example, if your monthly payment is $10,000 and you contribute $2,000 of that to your 401(k), only $8,000 of your paycheck will be subject to tax. While the money is in your account, it is protected from taxes as it grows.

What are 403(b) vs 401(k) Advantages And Disadvantages?

Everything that has an advantage has a disadvantage. In the same way, 403(b) vs 401(k) have their advantages and disadvantages. Let us take a look at some of them.

403(b) Plan Advantages

The advantages of contributing to a 403(b) account include:

#1. Tax advantages

Generally, 403(b) accounts carry the same tax advantages as 401(k)s and IRAs. You can enjoy a smaller tax bill in exchange for taxes on distributions in retirement. Or tax-free withdrawals in retirement if you pay taxes on your contributions. That depends on whether you choose a traditional or Roth 403(b).

#2. High contribution limits

Contribution limits for 403(b) accounts, discussed above, are on par with 401(k) contribution limits and much higher than IRA contribution limits.

#3. Employer matching

Employers offering 403(b) plans may offer to match some of their employees’ personal contributions, just as companies offering a 401(k) might do. Each company has its own rules about how, when, and if it will match employee contributions.

#4. Shorter vesting schedules

Vesting schedules determine when your employer-matched funds are yours to keep. This differs from company to company, but 403(b) vesting schedules are shorter than 401(k) vesting schedules. Some 403(b)s may offer immediate vesting, meaning you get to keep all employer-matched funds that have been made, no matter when you leave that job.

403(b) Plan Disadvantages

Some of the shortcomings to identify when contributing to a 403(b) account are:

#1. Few Investment Choices

Up until recently, 403(b)s gives only changeable annuities. While this is no longer the case, this type of account allows more limited investment options than a 401(k) or an IRA.

#2. High Fees

Some 403(b)s charge higher fees that can consume your profits. However, this isn’t true of all of them. To avoid this, make some inquiry into the plan’s administrative costs and any fees linked with your investments. Also, try to keep these as low as possible to maximize your profits.

#3. Penalties On Early Withdrawals

If you withdraw funds from your tax-deferred 403(b) before 59 1/2, you’ll pay a 10% early withdrawal penalty in addition to taxes. However, the penalty is ignored if you have a good reason, like a huge medical expense. This is also applicable for IRAs and 401(k)s.

401(k) Plan Advantages

There are advantages of utilizing this type of investment:

- Significant contribution limits (currently $19,500 per year if 49 years old or lesser and up to $25,500 if 50 or older in 2020)

- Income tax benefits cover investing with pretax dollars and tax-deferred growth on the account until the time of distribution

- Potential employer matching

- Loans in the case of an urgency or financial crisis

401(k) Plan Disadvantages

These are the disadvantage of a 401(k) plan.

- Most plans have restricted flexibility as it links to the quality and quantity of investment choices.

- Fees can be high, notably in smaller company plans.

- There can be early withdrawal penalties equal to 10% of the amount withdrawn before age 59 1/2.

- The individual needs to make investment choices by themselves with very little help or direction from the plan provider.

- Members need to observe and control their plans over time. Again with very little help or direction from the plan provider.

403(b) vs. 401(k): Which Is The Better?

The type of plan doesn’t really matter. One isn’t better than the other.

Instead of assessing a 403(b) vs a 401(k), estimate the plan’s investment choices. Basically, the larger the company, the lower the plan fees. Hence, more people are partaking, which brings costs down. If you manage a small company, examine lower-cost index funds as an investment option than placing money in higher priced actively managed funds.

Either way, if your company matches your contributions, consider partaking in the plan up to the highest amount they will match. After that, open an IRA if the plan’s fees are high or if you want to expand your investments to choices not open in your 401(k) or 403(b).

What are 403(b) vs 401(k) Plan?

401(k) and 403(b) plans have a lot in common, but here’s what sets them apart:

Eligibility:

401(k) plans are open for-profit companies, and 403(b) plans are given by tax-exempt organizations, such as schools, universities, hospitals, nonprofit and religious organizations.

Investment Options:

403(b) plans only cover mutual funds and annuities. However, 401(k) plans cover mutual funds, annuities, stocks, and bonds.

Employer Match:

Both plans offer employer matching, but fewer employers offer matches with their 403(b) plans. If an employer who provides a 403(b) does offer a match, they have to follow the regulations created by ERISA—the Employee Retirement Income Security Act—passed in 1974. Complying with these regulations costs time and money; hence most employers want to avoid them.

Cost:

With the 403(b) plan, the government would not want to place extra burdens on a nonprofit organization by giving higher administrative costs. However, 401(k) plans are more expensive for employers. But never mind, this doesn’t affect you as an employee.

Conclusion

In conclusion, 403(b) vs 401(k) plans are all good plans. One is not better than the other. 403(b) vs 401(k) have their contribution limits.

Instead of assessing a 403(b) vs a 401(k), estimate the plan’s investment choices.

403 (b) vs 401 (k) FAQ

Which is better 403b or 401k?

Instead of assessing a 403(b) vs a 401(k), estimate the plan’s investment choices. Basically, the larger the company, the lower the plan fees. Hence, more people are partaking, which brings costs down. If you manage a small company, examine lower-cost index funds as an investment option than placing money in higher-priced actively managed funds.

What are the disadvantages of a 403 B?

Some of the shortcomings to identify when contributing to a 403(b) account are:

- Few Investment Choices

- High Fees

- Penalties On Early Withdrawals:

Related Article