If you are new to the accounting term, “trial balance” as an accountant or interested individual, then this article will take you through the basics ranging from its meaning, format, and requirements.

Without further ado, Let’s begin…

Trial Balance Meaning

In simple terms, a trial balance refers to a worksheet used for bookkeeping.

Trial balance comprises of the balances of every ledger which is organized and compiled into credit and debit account columns by an accountant. The totals of both often need to be equal.

Basically, a company prepares a trial balance usually at the end of reporting periods with the aim of ensuring that these entries in the bookkeeping of a company are correct mathematically.

However, while anyone can run or create a trial balance, over time this job has been handled by accountants, and graduates of related courses like; Business Administration, Economics, and Mass Communication. This is because companies use trial balances as an indicator to tell if there are losses or gains in the course of a financial year.

How does it Work?

Creating a trial balance for a company helps to limit errors that come with calculations during the process of accounting.

If the risk credits equal the credits then the trial balance is said to be fully balanced.

Meanwhile, it is common to find errors like the improper usage of methods or unavailability of some essential elements from this system. But while these are not entirely inevitable, it is vital that you reduce them to the barest minimum. Trial Balance is a means to ensure these issues do not affect the annual records at the end of the year.

Requirements

Business transactions are initially recorded in bookkeeping accounts in the general ledger. Accounts in the ledgers may have been debited or credited during a specific accounting period before being included in a TB worksheet; depending on the types of business transactions. It’s also possible that some accounts were tools to record several business transactions. As a result, the concluding balance on the TB worksheet for each ledger account is the sum of all debits and credits submitted to that account on the basis of all linked business activities.

The accounts of asset, expense, and loss should all have a negative balance at the conclusion of an accounting period, whereas the accounts of liability, equity, income, and gain should all have a credit balance. During the accounting period, however, certain accounts of the former type may have been credited and certain accounts of the latter type may have been debited when related business transactions reduce their respective accounts’ debit and credit balances, resulting in an opposite effect on those accounts’ ending debit and credit balances. The account titles are always at the far left of the two columns on a TB worksheet. The debit balances go to the left column and all the credit balances, the right column.

Types of Trial Balance

Credit and Debit columns, that’s basically what you would see when you check whichever type of Trial Balance available.

The trial balance is a list of all the accounts a company uses with the balances in debit and credit columns. Basically, there are three types of trial balances. There’s the post-closing trial balance, the adjusted trial balance, and the unadjusted trial balance. All of these have the same format.

#1. The Unadjusted Balance

is made just before adjusting the journal entries. It reflects all of the activities on record from the daily transactions. They come in handy in analyzing accounts when preparing to adjust entries.

#2. The Adjusted Balance

This is fully completed after the entries on the unadjusted reflect in all of the accounts. Basically, they are vital for building and balancing financial statements.

#3. The Post-Closing Balance

This is often available to show balances immediately after the completion of closing entries. It is the starting balance for the next year.

Meanwhile, accounts available in the trial balance are listed below. This aids in the preparation of statements financially.

- Assets

- Liabilities

- Equity

- Revenue

- Expenses

What You Should Know

Liabilities and assets need to get listed on those that are most liquid to those that are least liquid. Liquid implying types of either assets or liabilities that one can easily turn to cash— the most liquid assets being cash because it is already cash. The next most liquid asset is account receivables because several forms get their receivables within thirty days.

Moving on, you could get liabilities and assets in terms of long-term and current. A current asset is one that would most likely get used up in less than a year. A current liability, on the other hand, is one that would get paid in less than a year. Long-term liabilities and assets are those that would be available on the trial balance for more than a year.

N.B: Revenue refers to the entire amount of funds your business is making while expenses refer to the entire amount of funds the business uses for its runnings daily. These are all important for things to flow properly in the company.

Uses

The following are some of the uses of a trial balance for accountants in the course of an accounting period;

#1. Financial Statement Preparation

A trial balance assists in the preparation of financial statements, balance sheet, profit and loss account, and cash flow statement an accountant would need to prepare at the end of each accounting year.

#2. Record Rectification

This is the most prominent of all the uses on this list. Errors are a common phenomenon in the accounting world especially when it is done manually. So, rectification of records would definitely come up occasionally.

Accountants, in the end, feel better off when the trial balance credit and debit match.

#3. Adjustments

These include adjustments in accounts like closing stock, prepaid expenses, and others that need to get prepared during the creation of the trial balance of a company.

This would make the records relevant to the present accounting year. Meanwhile, businesses prepare these adjustment accounts at the end of a financial year.

#4. Business Analysis

It also aids business analysis comparatively. Preparation of trial balance is vital in comparing the balances of the present year with that of the previous year. This will help the business in making the necessary decisions on issues like costs, production, expenses, and income.

It also a factor in recognizing trends in the business and take action wherever it is necessary.

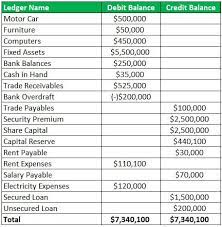

Trial Balance Format

A typical trial balance format lists all the accounts from the general ledger available on each side.

On the right hand, we have two columns. One for credits and one for debits.

The general ledger of a business is often made available for accountants or individuals as it is the most vital element of creating the trial balance.

Because as you generate a TB, you would need to sum up all of the values and then list them out together using the names of these values. These values go into the credit column and the debit column.

In the end, you’ll need to ensure that the total of your credits is fully equal to the total of your debts. All of that is very important.

What Is in the Trial Balance?

Trial balance sheets list all of a business’s accounts that have debits or credits during a certain reporting period, along with the amounts credited or debited to each account, the account numbers, the dates of the reporting period, and the total amounts of debits and credits entered during that time.

What Are the 3 Trial Balances?

There are three kinds of trial balance: the unadjusted trial balance, the adjusted trial balance, and the trial balance that is done after the business has closed. At different points in the accounting cycle, each is used.

What Is Dr and CR in Trial Balance?

A “CR” is written on the account when the amount of liabilities or shareholders’ equity goes up. A debit, which is written as “DR,” is a decrease in liabilities.

What Are the 4 Financial Statements in Order?

A balance sheet.

Income statement.

Statement of cash flow.

Statement of what the owner is worth.