An LLC insurance refers to a business insurance product held by a limited liability company for the purpose of protecting the company’s assets. While an LLC protects your personal assets from debts and liabilities incurred by your business, an LLC isn’t inherently protected from any liabilities caused by the business itself.

LLC insurance lets business owners obtain financial protection for their businesses and pay any claims against their businesses. Insurance products under this category can compensate your customers for their lost property, help you rebuild buildings, and pay salaries while you get your business up and running again.

This type of coverage comes in many forms. To get the policy that matches the needs of your business, you must also understand the kind of protection each one provides.

What is an LLC?

LLC stands for limited liability company, which is a business that is completely separate from your personal finances.

This means that the LLC forms a wall between the company and you, the business owner. It protects your personal assets from being negatively affected if someone sues the business or if someone gets hurt as a result of your work. It is more complicated to create an LLC than to simply run your business as a partnership or sole proprietorship, but there are real advantages to setting up an LLC.

An LLC can have one or more owners, also referred to as members. LLC members typically share the responsibility of managing the business in a system called member-managed.

Therefore, LLC insurance refers to a business insurance product held by a limited liability company for the purpose of protecting the company’s assets. While an LLC protects your personal assets from debts and liabilities incurred by your business, an LLC isn’t inherently protected from any liabilities caused by the business itself.

If you have chosen to structure your small business as a limited liability company, you may have already considered risk management—since one of the benefits of an LLC is the financial protection it offers to small business owners. By partitioning your personal assets (like your house, car, or personal savings account) from your business’s assets (like a business savings account, a commercial vehicle, or inventory), an LLC structure can prevent creditors to your business from coming after your personal assets.

What the LLC structure does not protect, however, is any of the assets that your business owns. To get coverage for business assets, many LLC owners work with an insurance company to get LLC insurance coverage.

Types of insurance for LLC

There are many types of LLC business insurance. Some fall under a business owner’s policy (BOP)—an insurance package that bundles multiple types of coverage—while others have to be purchased separately or obtained as policy add-ons.

Common LLC business insurance policy types include:

Business Owners Policy (BOP)

If you want general liability insurance and property coverage, you can package them together in a business owner’s insurance policy, also known as a BOP. A BOP provides liability coverage for customer injury, property damage, and product-related claims, in addition to commercial building and movable property coverage.

Property insurance

Property insurance covers the physical assets of a business, including buildings, equipment, inventory, and other tangible property. It provides compensation for losses due to events like fire, theft, vandalism, or natural disasters.

Property insurance helps businesses recover and repair or replace damaged or stolen property, minimizing the financial impact of such events. The type of coverage you need will depend on the property you own or rent.

Types of insurance under property insurance include:

Commercial property insurance

Commercial property insurance protects your physical assets (building, equipment, inventory, tools, furniture and personal property) and covers financial losses due to property damage from fire, theft or loss.

Homeowners’ insurance

If you have a home-based business or store business property in your house, check the business coverage under your homeowners’ insurance. Homeowners insurance often only provides limited coverage (e.g., $2,500) for business property or equipment stored in your home, and some policies don’t cover business property at all.

Business renters insurance

Business renters insurance is essential for businesses operating in one or more rented spaces. It will cover incidents within the space, including fire, floods, accidents, and building or property damage due to natural disasters. This type of insurance covers many things that the other policies also cover, but for rented spaces specifically.

Liability insurance

Liability insurance protects businesses from legal claims and financial losses resulting from third-party injuries, property damage, or lawsuits. It covers legal defense costs, settlements, or judgments if the business is found legally liable for causing harm or injury to others.

Types of insurance under liability insurance include:

General liability insurance

General liability insurance, also known as business or commercial liability insurance, is essential coverage for various claims, including bodily injury, property damage, personal or advertising injury, medical payments, products-completed operations, and damages to premises rented to you.

Professional liability insurance

Professional liability insurance, also known as errors and omissions (E&O) insurance, protects businesses that offer professional services. B2C businesses often use E&O coverage to protect against claims stating their services caused clients financial distress or bodily injury.

Workers’ compensation insurance

Workers’ compensation insurance provides coverage for LLC employees who suffer work-related injuries or illnesses. It covers medical expenses, disability benefits, and lost wages for employees who are injured or become ill while performing their job duties.

Workers’ compensation insurance is typically required by law and helps protect businesses from potential lawsuits by employees seeking compensation for work-related injuries or illnesses. If an employee accepts the benefits of workers’ comp, they relinquish their ability to sue your company for the illness or injury.

Types of business insurance under this include:

Life insurance

You and any other members of your business can acquire a life insurance policy. This is similar to key person insurance, providing a beneficiary with financial assistance in the event of your death. Having life insurance in place can give you peace of mind that your death will not burden your family or business partners financially.

Disability income insurance

Disability insurance is similar to workers’ comp in that it temporarily covers an employee’s lost wages if they are unable to work because of a disability. However, disability insurance will cover injuries or illnesses that occurred on or off the job, whereas workers’ comp only covers work-related issues.

This type of insurance is also sometimes required by law.

Key person insurance

Businesses often have a challenging time continuing operations when founders die. This is why it is essential for entrepreneurs to create a business continuity plan so the company can still thrive if the worst happens.

Also known as key man insurance or key woman insurance, key person insurance helps an LLC replace lost revenue due to the death of a key executive of your business. Your business pays the premium while the key person is alive and then collects a death benefit after their passing.

These benefits can be essential to continuing the operation of your business or finding someone to fill their role.

Business interruption insurance

Business interruption insurance, also known as business income insurance, is one of the most common types of coverage most small businesses need. If a disaster strikes (such as a fire, flood, theft, building collapse or civil authority incident) and your business is required to shut down for a period of time, it will help cover lost income or operating expenses like mortgage or rent, loan payments, taxes, and payroll.

Commercial auto insurance

Commercial auto insurance provides coverage for vehicles used for the LLC’s business purposes. It includes liability coverage for third-party injuries or property damage, as well as coverage for damage to the insured vehicle.

This type of insurance is similar to personal automobile insurance; it protects your cars, trucks or vans in the event of damage, injury or liability claims. However, commercial auto insurance provides additional coverage, including property and liability trailer exposure, loading and unloading exposure, hired vehicle coverage, non-owned vehicle coverage, and higher coverage limits.

Cyber liability insurance

If your business handles and stores sensitive customer data, then cyber insurance is a type of liability insurance for LLC that you should have. It protects your company from lawsuits filed by clients, vendors, and even employees for damages caused by a cyber incident. The policy covers court fees, settlement costs, and regulatory fines.

Cyber insurance also pays out for the financial losses your business incurs due to a cyberattack. These include:

- The cost of responding to a data breach

- The cost of restoring and recovering damaged or lost data

- Lost income resulting from business interruption

- Ransomware attack payments

- The cost of risk assessment for future cyberattacks

- The cost of notifying clients about the cyberattack

- Anti-fraud services

A cyber incident can prove costly to your business, especially if you don’t have the proper coverage.

Product liability insurance

Product liability insurance may be worth considering if your LLC manufactures, designs, or sells products. This type of coverage protects your business against lawsuits from clients claiming injuries or losses because of your product. It pays out legal defense costs, as well as third-party compensation if your company is found to be at fault.

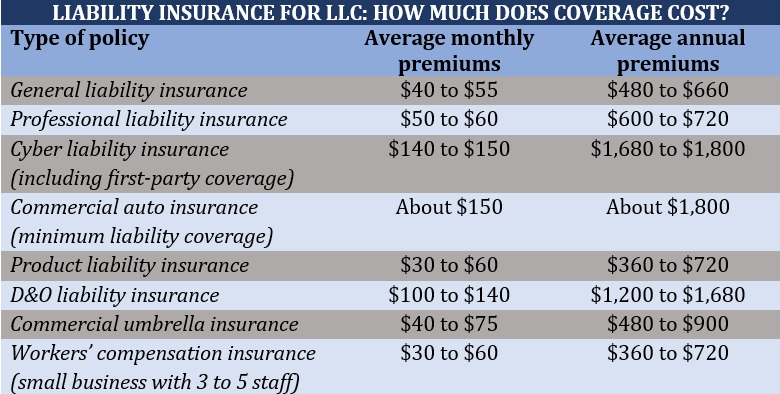

How much does liability insurance for LLC cost?

Liability insurance coverage consists of a range of policies that provide varying levels of protection. That is why it is hard to come up with a general estimate of how much coverage costs.

The table below breaks down how premiums cost for the different types of liability insurance for LLCs based on the various price comparisons and insurer websites, according to Insurance Business:

The cost of liability insurance for LLCs is also influenced by several other factors. These include:

- The number of employees

- The nature of your business

- Where your business operates

- How many properties and equipment your business owns

- The types of policies you purchase

- Your annual revenue

- Coverage limits and deductibles

Do I need business insurance if I have an LLC?

The short answer is yes. One of the main benefits of forming an LLC is that your personal assets are more protected. However, if a client slips and breaks their arm while in your office premises, your business could still be liable for covering the medical fees. If you don’t have liability insurance for your LLC, your business finances could be severely impacted.

A lawsuit could also put your business at risk. If you don’t have the proper insurance, you could be forced to pay out of pocket for legal defense costs even if you aren’t found liable.

The only way to cover your business against these types of scenarios is to get LLC business insurance.

How to get LLC insurance

You can obtain LLC insurance by working with an insurance broker, consulting an online insurance marketplace like Insureon or CoverWallet, or contacting an insurance agent to obtain a quote. Although working with an insurance broker can be costly, it can save business owners time and labor.

Also, a trusted insurance broker can also offer advice about finding a best-fit plan for your business for particularly complex policy needs.

To find a plan that meets your business’s needs, contact multiple providers to obtain quotes and compare coverage options, insurance rates, and policy exclusions across plans. Your rates will vary considering annual revenue, location, number of employees, and industry. Businesses in higher-risk industries such as trucking, construction, and demolition are typically more expensive to insure than lower-risk office-based businesses.

Some insurance providers also offer discounts for purchasing multiple policies (or for purchasing an insurance package, such as a business owner’s policy).

Recommended Articles

- Business Insurance: Definition, Types & What Does It Cover?

- How Much Does Business Insurance Cost?

- Types of Business Insurance: What Coverage Does Your Business Need?